What have Google and Amazon taught all of us? Simple is better. You can get information, answers, and product options by typing one word into your browser. Make one click and have a package of goodies delivered to your doorstep tomorrow.

With financial institutions the product experience is the opposite of this — there are many complex options, difficult-to-understand pricing and rewards hurdles, and multiple-click applications. With the war for deposits and for new customers intensifying, financial institutions everywhere need to re-examine their product lines for both consumers and businesses.

Four principles rise above other considerations to help banks and credit unions successfully transform their product lines to support superior new customer and new member acquisition, deposit and loan growth.

1. Simplify Product Features By Using a Layered Approach

Despite the fact that financial products are far more significant in people’s lives than buying a new fleece jacket, and subject to regulations, consumers now expect a simple experience whether they are buying a car, buying a house or buying a bank account. Yet, most banks and credit unions continue to offer confusing, complicated products with numerous hurdles along the way and confusing pricing structures. This can be simplified.

For example, if you offer more than four checking products to consumers or small businesses, it’s time to start streamlining your deposit product line. It helps to think back to why checking accounts were originally created: a simple way to exchange funds without using cash, and a safe and secure alternative to hiding cash under the mattress. Your basic checking account should do the exact same thing it always did – enable the movement of money and provide security for funds.

Several institutions are now offering only one checking account and are finding success with this strategy.

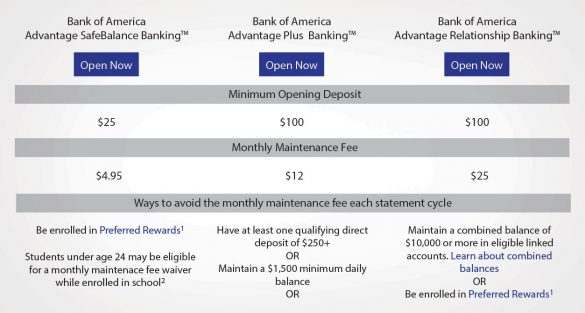

- Bank of America = Advantage Banking

- Capital One = 360 Checking

- Frost = Frost Personal Account

- USAA = USAA Classic Checking

- Discover = Discover Cashback Debit

Some of these institutions also offer student accounts, but for the general population, they have consolidated down to one basic checking product with simple pricing and flexible benefits. This helps accomplish four goals:

- Better compete with online only offerings.

- Make it easier to sell through digital and traditional channels.

- Simplify the fee structure so consumers better understand what they are paying for.

- Manage a product structure with the flexibility to change, add or remove benefits at any time.

“By keeping the deposit product line simple and functional, you create the ability to layer on benefits and rewards.”

Whether you decide to simplify to one account or several, product re-design can help attract a new segment of customers and grow new households faster. It also can provide more benefits to customers who bring more of their wallet to you. However, you do not need to bake every single benefit into your deposit accounts. By keeping the deposit product line simple and functional, you create the ability to layer on benefits and rewards, create bundles and packages, and launch special promotions at any time.

Designing products in this modular way also means you can remove benefits, bundles, packages, programs and promotions at any time. This gives financial marketers the flexibility to push and pull certain levers at certain times to help achieve your goals. This becomes critical as interest rate environments and the need for deposits change over time.

Here are three examples of how to use modular feature flexibility:

- Need more deposits? Offer a short-term rate incentive on a money market account to checking customers with certain balances.

- Need real estate loans? Offer a discount on the interest rate or closing costs when the monthly mortgage is paid electronically.

- Need to acquire new customers? Know your target segments and create short-term promotions that appeal directly to them, provided they open a checking product and meet your promotion requirements.

Bank of America provides a good example of how to build interchangeable benefits on top of a simplified product line. Instead of offering multiple products, they are offering a single product, Advantage Banking, with three “settings” the customer can change anytime. The three settings are actually product bundles and pricing options:

By simplifying the chassis, you can customize other aspects of the product or create programs and packages to appeal to target groups. The underlying product set and operations don’t need to change, which eliminates the need to grandfather tons of products and accounts created for special situations. This approach also makes things much simpler to manage internally.

An additional benefit is that this layered approach engages the customer to select the suite of benefits and associated pricing that best meets their needs.

Read More:

- Have Traditional Checking Accounts Become Obsolete?

- How to Build Banking Products Consumers Will Love

- Seven UX Design Hacks to Make Your Banking Insanely Great

2. Have a Strong Value Proposition that Appeals to Target Segments

While financial institutions may need to service many customer segments, they do not need to tailor their products to each of them. There are successful and profitable institutions that have focused on a wide range of segments from younger mass affluent to older Millennials, and from dentists to property managers.

This laser-like focus allows institutions to create differentiated approaches to meet unique needs of target segments. The most successful institutions have value propositions, products, delivery channels, sales and service aligned to resonate and win with these targeted segments.

Product development becomes a lot easier when you are creating products, bundles, packages and programs for specific groups of people with similar needs. Finding and communicating a great value proposition also gets easier the more focused you become on your target segments.

Here are four keys to having a great product value proposition. A product line:

- Is easy to describe to customers and staff.

- Offers increasing levels of benefits to customers as they bring more of their wallet to the financial institution.

- Has clear, easy-to-understand pay-offs that not only appeal to your target segments, but are attractive to other customers and segments in your customer base.

- Differentiates you from competition in the eyes of your target customer.

Using the value propositions that are important to your target segments, and that capitalize on lack of strong competition, can help fuel growth. Research can uncover such “competitive white space” where your institution can focus to create competitive advantage.

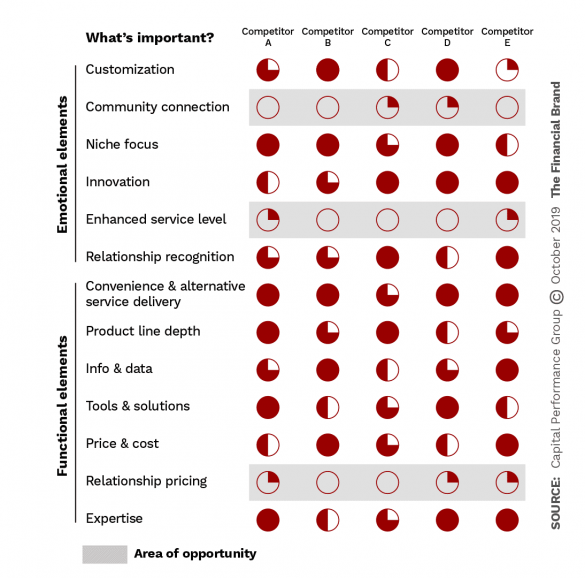

One regional bank, for example, uncovered an opportunity for a differentiated product value proposition by analyzing competitors’ relative strengths and weaknesses in 13 categories. This led to the identification of opportunities in three areas: Community Connection, Enhanced Service Level, and Relationship Pricing, as shown in the chart.

One regional bank’s competitive market scan found three areas of relative weakness that it could build on

3. Price for Your Competitive Environment, Not for Your Vendors … or CFO

Many financial institution teams, sitting in conference rooms, price new products based solely on the underlying costs paid to vendors with little consideration for the competitive pricing environment or customer impact. Obviously, your cost basis is important for determining the profitability of your product line, but pricing should not be done in a vacuum.

The best pricing schemes incorporate a thorough competitive analysis and understanding of your target segment needs, wants and price points. After all, any person shopping for a new account is researching, comparing and contrasting financial institutions and products online.

The financial services business is national and virtual now, so you need to understand how Chase and Bank of America are structuring and pricing products, even if they are not in your market. The big banks and digital banks are influencing your customers’ pricing expectations just as use of Amazon, Apple and Google are influencing your customers’ user experience expectations.

“Finance often wants every customer to be profitable. That’s not how pricing works!”

Finally, the finance department often wants every customer to be profitable. That’s not how pricing works! You want to design a product so the majority of users are profitable. Creating balance levels, item counts and other stipulations to catch every optimizer and make them profitable makes your pricing confusing and difficult for your employees and customers to understand.

At least as important: That complexity will significantly hamper the success of your new product launch.

Read More: Five Reasons Financial Institutions Struggle With Onboarding

4. Redesign Like a Customer, Not Like a Banker

Product redesign teams have a tendency to design products that are attractive to them as bank or credit union employees, not as consumers. As a result, products are often unnecessarily complicated and don’t actually solve the real need or problem the retail or business consumer has.

A classic example was a bank that created three tiers of business banking, based on a combination of balance level and item count. Each tier had different pricing for benefits like remote deposit capture and merchant services. The only problem was that customers could move from one tier to another each month as their balance and items fluctuated. This became so confusing that the bank’s staff began placing every new customer in the most basic package, eliminating any potential benefit that might have been gained by the product redesign.

Another great example of this “inside-out thinking” is the long list of stipulations and qualifications customers often have to meet in order to qualify for a product or offer. Here are three examples; see if they seem familiar:

- Monthly direct deposits — of over $500 — for three consecutive months

- At least five bills paid online per month

- At least ten debit card transactions per month of more than $10 each.

“Our industry can no longer afford to be so inwardly focused. There are too many competitive options for customers now.”

Customers don’t have time to track their debit card usage, and most financial institutions don’t provide the tools for them to do that. Many people end up not reaching their hurdles and get hit with fees. Nothing makes consumers less loyal and more likely to switch than being hit up with unexpected fees.

Our industry can no longer afford to be so inwardly focused. There are too many competitive options for customers to take advantage of and too many new places for them to park their money.

If your bank or credit union does not have a customer or client experience officer or team, be sure to designate one person on every product development team as the customer advocate. Their job is to think through all aspects of product design from a customer’s point of view. We’d even suggest you find a young, technically savvy person from outside the industry for this role and empower them to challenge the status quo. Your product line and decision making will be stronger for having a forward-thinking customer advocate on the team.