There’s no doubt that retail banking leaders understand the potential of artificial intelligence technology to improve customer experience. Nearly every one (94%) of more than 300 banking and insurance executives surveyed by The Capgemini Research Institute agreed that improving CX is the key objective behind launching new AI-enabled initiatives.

In fact, more than half of the international sample say that at least 40% of customer interactions are already enabled by various AI applications, including conversational agents, prescriptive modeling, process automation, and complex analytics.

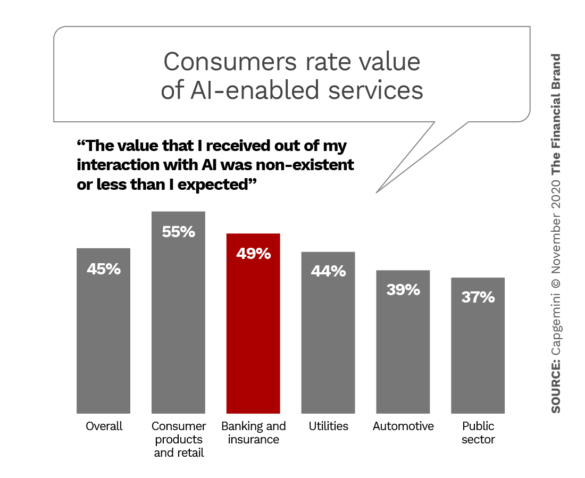

That would be impressive — except for one thing: Half of more than 5,000 consumers polled by Capgemini worldwide feel that the value they receive from AI-powered financial interactions was “non-existent or less than expected.”

What about in the U.S., the land of “Erica” and “Eno” and other digital assistants, and the many advanced mobile banking apps?

Capgemini found fewer consumers in the U.S. who see no, or little, value from AI interactions — 38% versus 49% worldwide. But that’s still a strong indication of a significant lack of satisfaction.

“The U.S. generally is more advanced when it comes to AI-based research and innovation in general,” Elias Ghanem, Global Head of Market Intelligence for Capgemini Financial Services told The Financial Brand. It is also home to most of the big techs, meaning that U.S. financial services firms face both greater opportunities and greater threats, he adds.

Ghanem agrees that some of the largest American banks — Wells Fargo, BofA, Capital One — have implemented AI solutions that allow them to compete with fintechs and big techs. But most traditional financial institutions, he believes, still struggle with prioritizing the right AI initiatives and scaling AI applications across all their divisions. Much of that, he says, is due to siloed data and thinking.

Capgemini’s latest report on AI in financial services, states that “AI should be used for more complex customer interactions, such as creating customer personas to understand needs and create a relationship. These solutions deliver the greatest benefit but are rare in the industry when it comes to scaled adoption.”

Use of AI in Banking Is Surging

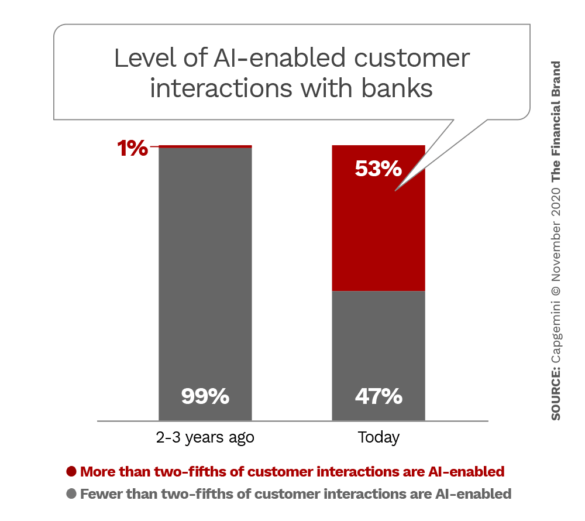

Use of artificial intelligence in banking has been growing rapidly in banking over the past few years. Currently just over half of all financial institutions surveyed by Capgemini report that 40% or more of their customer interactions are AI-enabled. Three years ago just 1% of banks worldwide saw that level of AI use.

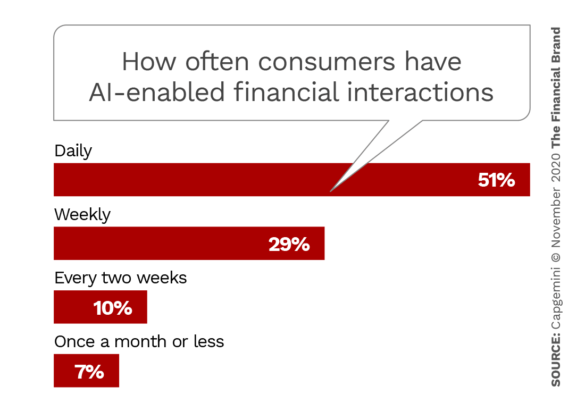

Customers themselves are increasingly aware of the role of AI in banking interactions. About half report that AI-enabled transactions are part of their daily life. The COVID-19 pandemic boosted this trend, according to the report, due to the desire of so many people to use contactless interactions through voice assistants, chatbots or mobile apps.

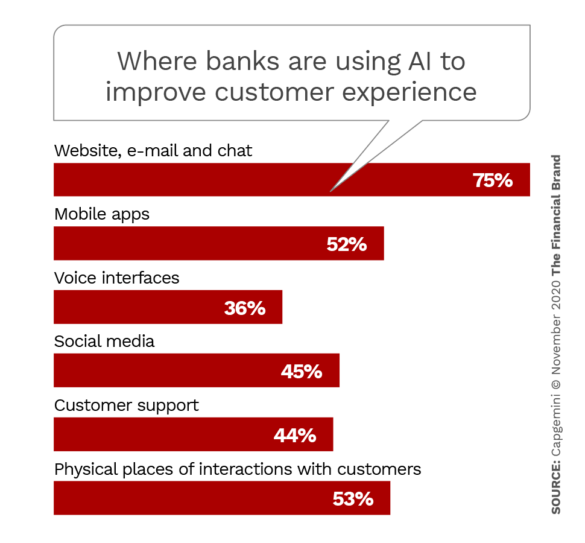

As the chart below demonstrates, financial institutions are using AI to automate answers to commonly asked consumer queries, as well as to conduct sentiment analysis on social media platforms. The bar for “physical places of interactions” includes use of AI with ATMs and kiosks for credit card and other account-opening applications.

Perception of AI Value Lags Usage

The most notable finding of the Capgemini report is that AI use for consumer interactions has not lived up to expectations. As mentioned above, nearly half of all consumers surveyed were underwhelmed by the value they receive from banks’ use of AI.

“Consumers may be satisfied with banking AI from the viewpoint of getting the work done,” Ghanem explains. “The AI interactions may just be substituting for the work done by a human and still be satisfactory, such as basic, text-based chatbots.”

“However, the novelty factor of AI interactions may be wearing off,” Ghanem continues. ”

Three reasons for the lack of customer enthusiasm with banking AI were suggested in the report:

- Lack of value received for data. 57% of customers believe that they do not have any incentives for allowing AI to use personal data.

- Absence of a human touch in AI interactions. 79% of banks and insurers agree consumers want human-like AI interactions. 35% of customers, however, believe they are not receiving them.

- Awareness of AI involvement. 71% of customers say they want to be made aware when they are interacting with AI, but only 29% of bank and insurance company executives believe this is what consumers want.

In addition, Ghanem points out two additional factors that impact the AI-powered services of banks and credit unions:

- Hyper-personalization. Consumers willing to share their data with banks and credit unions expect hyper-personalized services, products, advice and offers (or pricing) in return.

- Empathy. AI experience needs to retain the human and emotional touch, especially during “signature moments.” These interactions that support customers in times of need (such as family loss, job loss, sickness and fraud).

Benefits of AI: Actual and Potential

Despite the fact that many consumers don’t find all that much value in AI-initiated banking transactions, the industry’s efforts to implement the technology have already led to benefits. The Capgemini report points to two broad areas: Reduction in operating costs and increased revenue per customer. In addition, a quarter of banks have seen a 20% to 40% increase in customer engagement.

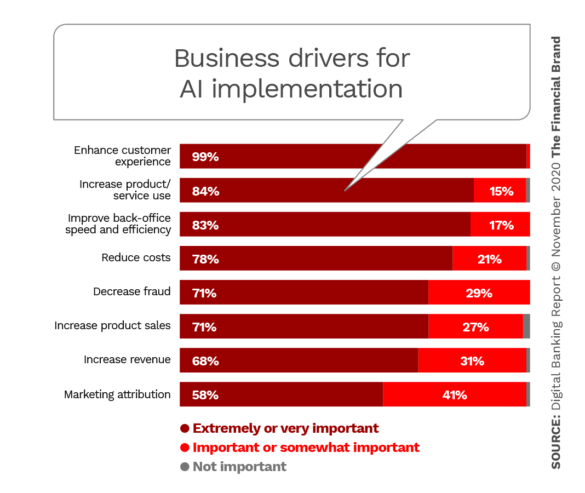

New research from the Digital Banking Report indicates the near universal view of enhanced CX as a primary benefit of AI implementation. The DBR research also identifies reduced costs and improved back-office efficiency, as among the top benefits sought.

Bank of America appears to have benefitted by its investment in its digital assistant “Erica.” J.D. Power singled out BofA (along with Capital One) in a report highlighting the benefits of having a digitized financial guidance and advice strategy, of which Erica is a key element. Ghanem cites two other examples:

- HSBC has been using AI to process customer data to predict how consumers will redeem their credit card points so it can better market offerings. Emails based on this data produced a 40% jump in open rate and a 70% jump in reward redemption.

- Commonwealth Bank of Australia uses AI to link and automate processes, integrating them with customer engagement tools. The resulting model, called “Next Best Conversation,” predicts outcomes and suggests potential actions. The NBC model is then used to train new AI models, exponentially speeding up the process of customer engagement.

Lack of Scale Hinders Financial Institution AI Use

“The future of AI usage for banks lies in enterprise scaling up of the technology, which will help them reap superior benefits,” Ghanem maintains. He positions that stage in the future because the Capgemini report finds that financial institutions overall lag other industries in deploying AI at scale across multiple teams, business lines, and regions.

What gets in the way of this expanded use of AI, according to Ghanem, is the difficulty in getting leadership buy-in because of an inability to demonstrate ROI for customer-facing AI pilots. In addition, he says about three quarters of senior banking executives don’t believe consumers trust AI-enabled channels for high-value interactions such as financial advice.

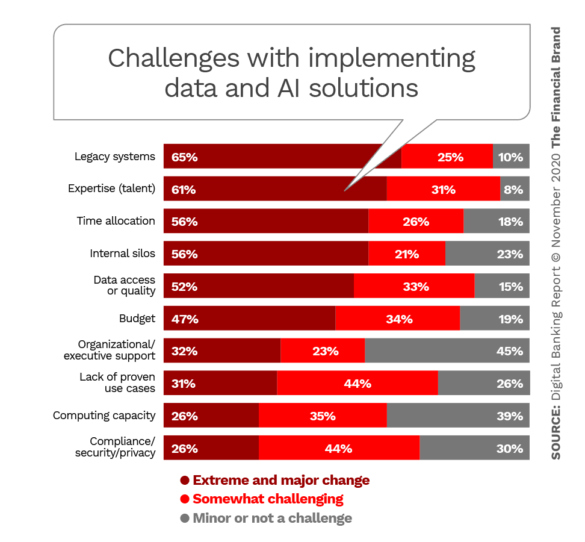

Meanwhile, as shown in the chart below based on the Digital Banking Report research, legacy technology and lack of AI talent top a long list of challenges banks and credit unions face to implement customer-facing AI.

“A fundamental shift in mindset will help banks overcome the challenge of scaling AI as an enterprise-wide innovation,” states Ghanem. Currently, the typical thinking is whether or not AI is right for solving a particular business problem and what the ROI is, he explains. “The way forward is to move from thinking how they can use AI to save money to thinking how they can use it to transform the customer experience.”

Read More:

- AI’s Real Impact on Banking: The Critical Importance of Human Skills

- Data Reveals a Surprise Driver of CX Satisfaction in Banking

The Road to Enterprise AI

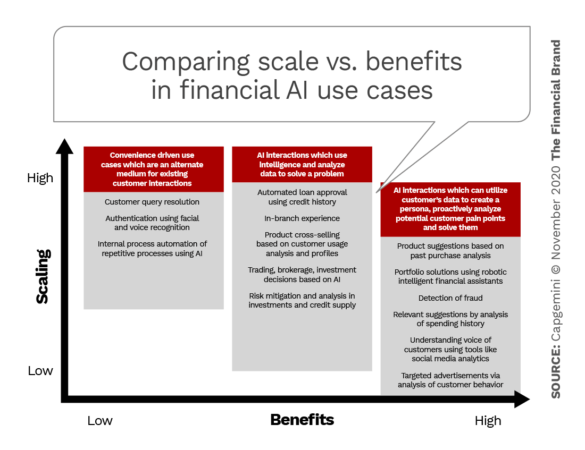

The chart below from Capgemini’s report depicts three areas in which banks and credit unions can concentrate their efforts at AI implementation for customer interaction.

The report lists six steps that will assist in moving this vision forward and improving the lackluster consumer view of AI technology uncovered by the report.

1. Invest in value-driven AI to transform the customer experience. This step emphasizes the need to identify use cases that address more complex consumer needs. Capgemini emphasizes that the best AI use cases for improving customer experience are those that are “context aware” — that is, applications that consumers find easy to use, are highly personalized, and offer control and efficiency. Detection of fraudulent transactions is one example. But hyper-personalization may be even more powerful.

2. Create trust-based and ethical AI approaches to drive adoption. An earlier Capgemini report, “Ethics in AI,” found that 64% of customers are not comfortable with the fact that important decisions are being made only by AI algorithms, and 68% of customers prefer to deal with companies that help them understand their AI output. Institutions should consider establishing a dedicated team to monitor use and implementation of AI from an ethics perspective.

3. Deliver an AI experience that incorporates empathy and emotion. This is more than having a human-like chatbot experience. People long remember how an institution interacted with them during the “signature moments,” mentioned earlier. Financial institutions should be able to identify use cases that need human as well as AI interventions.

4. Set up the technology foundation for an AI-enabled customer engagement. A customer engagement platform that is connected to a customer data hub is a prerequisite for creating a personalized and contextual customer experience. Such a platform offers a “single source of truth” and a unified view of the customer.

5. Add AI leadership roles to accelerate adoption. Currently half of the responding banks say they do not have an AI head/lead. Hiring, training and reskilling of organizational talent through a structured and long-term talent strategy and plan will be critical.

6. Educate consumers about AI and make AI systems explainable and transparent. The industry needs to make sure that they explain to customers how they are using AI at every step and how they are using their data.

“Financial institutions — regardless of size — are facing a ‘“black box’ issue in which they have no visibility on the processing of data used to make decisions,” warns Ghanem. He advises setting up a governance body as the first step and then augmenting this with technologies to audit and remove bias from the AI algorithms, and ensure high quality of data used in AI.