There are about 7.5 billion people on the planet, give or take a few. But that number pales in comparison to the number of connected devices worldwide. According to Autonomous, a financial research firm, people are outnumbered three-to-one by their smart computing devices — an estimated 22 billion in total. And the number of smart devices will continue to explode, with venture capital firms pouring $10 billion annually into AI-powered companies focusing on digitally-connected devices.

For financial institutions, their slice of this massive AI pie represents upwards of $1 trillion in projected cost savings. By 2030, traditional financial institutions can shave 22% in costs, says Autonomous in an 84-page report on AI in the financial industry. Here’s how they break down those cost savings:

- Front Office – $490 billion in savings. Almost half of this ($199 billion) will come from reductions in the scale of retail branch networks, security, tellers, cashiers and other distribution staff.

- Middle Office – $350 billion in savings. Just simply applying AI to compliance, KYC/AML, authentication and other forms of data processing will save banks and credit unions a staggering $217 billion.

- Back Office – $200 billion in savings. $31 billion of this will be attributed to underwriting and collections systems.

These numbers align with what other analysts and research firms have forecast. Bain & Company has pegged the savings at around $1.1 trillion, while Accenture estimates that AI will add $1.2 trillion in value to the financial industry by 2035.

In the U.S. banking sector, 1.2 million employees have already been exposed to AI in the front-, middle- and back office, with almost three-quarters of workers in the front office using AI (even if they don’t know it). If you include the investment and insurance industry, there are 2.5 million U.S. financial services workers whose jobs are already being directly impacted by AI.

Use Cases for AI

Autonomous sees three primary ways in which artificial intelligence will transform the banking industry:

- AI technology companies such as Google and Amazon will add financial services skills to their smart home assistants, then leveraging this data+interface via relationships with traditional banking providers.

- Technology and finance firms merge/collaborate to build full psychographic profiles of consumers across social, commercial, personal and financial data (e.g., like Tencent coupling with Ant Financial in China).

- The crypto community builds decentralized, autonomous organizations using open source components with the goal of shifting power back to consumers.

AI-enabled devices are already using vision and sound to gather information even more accurately than humans, and the software continues to get more human-like.

“Not only can software understand the contents of inputs and categorize it as scale,” Autonomous explains, “it has exhibited the ability to generate new examples of those inputs. Artists are now as endangered as lawyers and bankers.”

Read More:

- Why the ROI of AI Falls Short for Nearly Everyone

- Top Digital Banking Transformation Trends

- Rethinking Financial Services with Artificial Intelligence Tools

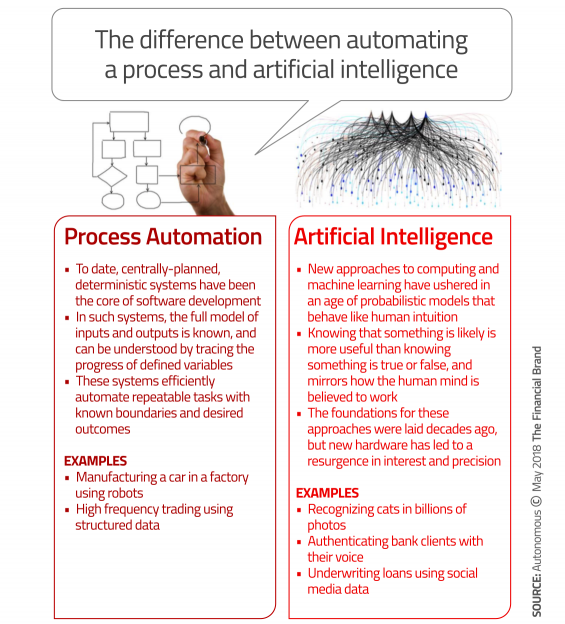

But AI still has a way to go before a computer will become the next van Gogh or Pollock. Today’s AI is “narrow,” meaning that the machines are built to react to specific events and lack general reasoning capability. That said, there are plenty of practical applications for AI that banks and credit unions are taking advantage of today.

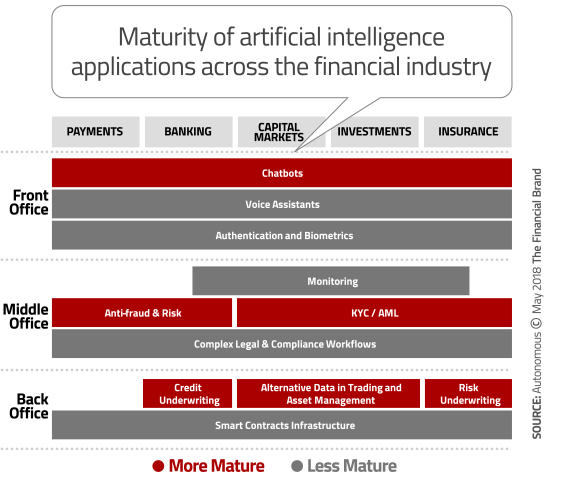

The most mature use cases are in chatbots in the front office, antifraud and risk and KYC/AML in the middle office, and credit underwriting in the back office.

Financial institutions can use AI to power conversational interfaces that integrate financial data and account actions with algorithm-powered automatic “agents” that can hold life-like conversations with consumers.

Bank of America has announced that it is aggressively rolling out Erica, its virtual assistant, to all of its 25 million mobile banking consumers. Using voice commands, texts or touch, BofA customers can instruct Erica to give account balances, transfer money between accounts, send money with Zelle, and schedule meetings with real representatives at financial centers.

Biometrics and workflow and compliance automation are other strong use cases for AI. To improve the consumer experience, AI can allow a bank or credit union to authenticate a mobile payment using a fingerprint or replace a numerical passcode with voice recognition.

In the middle office, AI can perform real-time regulatory checks for KYC/AML on all transactions rather than rely on more traditional methods of using batch processing to analyze only samples of consumers.

Perhaps the most promising application, says Autonomous, is using AI to incorporate social media, free text fields and even machine vision into the development of lending, investment and insurance products.

Surgery? No Problem… But Financial Advice? Hold Up There!

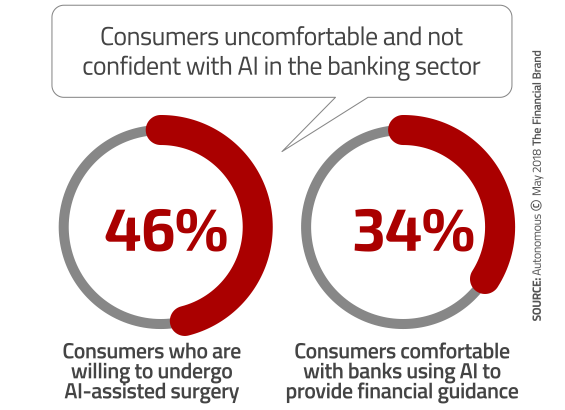

Consumers remain wary of AI applications, particularly in banking. In all honesty, consumers aren’t even sure what AI is, so perhaps they are simply afraid of the unknown. Sadly, only 44% of consumers in a survey from SAS said they could explain AI to someone else. And they aren’t convinced that personal data used in AI situations is being protected, with only 35% saying they were confident.

Consumers are fine with AI in healthcare settings, but are notably less comfortable with banks and credit unions using AI. More consumers say they trust healthcare providers to use AI to perform surgery or suggest medical treatment than they would trust banking providers using AI to provide financial guidance. AI in retail also gets the nod of approval from consumers: almost half say they are comfortable with retailers using computers and drones to fill and deliver orders.

The only area that consumers are comfortable with banks and credit unions using AI is in monitoring threats such as fraud, with 59% of consumers saying that using AI was okay. The least popular use of AI was for analyzing consumer credit history to make a credit card recommendation.

Consumer trepidation with AI in financial services could be attributed to a lack of understanding in how AI could improve consumer experiences or make their financial lives more convenient and even healthier. Just like banks and credit unions face a steep AI learning curve, the same is true for consumers.

It certainly doesn’t help that every major motion picture that incorporates AI into the plot casts the computer/robot as a heartless, diabolical villain out to destroy mankind. One of the earliest films, 2001: A Space Odyssey, sparked the public’s fear of AI when the computer “HAL” turned on the crew, killing them off one by one. Hollywood blockbusters like the Terminator series and The Matrix trilogy have trained movie-goers worldwide to distrust any machine capable of learning. Other films like Ex Machina and Her where female bots aspire to world domination compound the cinematically-induced AI hysteria.

Read More: AI’s Real Impact on Banking: The Critical Importance of Human Skills

The Rise of the Chatbots

Despite the public’s paranoia towards AI-powered conversational interfaces, developers in all sectors continue to plow forward. Major advances are being made using multiple machine learning techniques including speech recognition and natural language processing systems that turn spoken words into data. From this “raw material”, AI-powered platforms can extract meaning, detect emotion, interpret context, and ultimately frame an appropriate response.

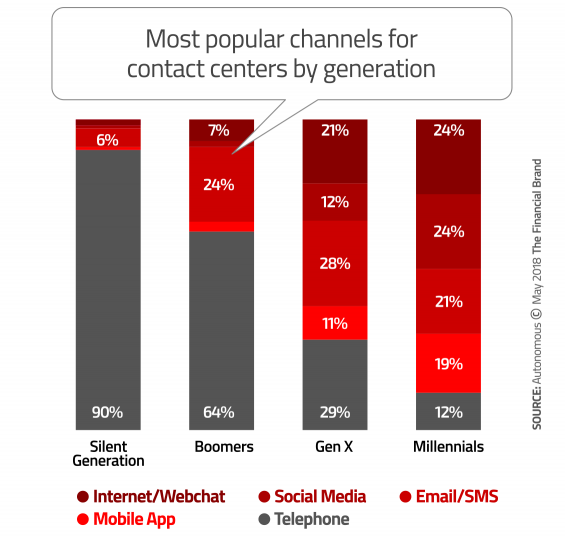

Such conversational interfaces are natural extensions of today’s mobile web and, not surprisingly, Millennial consumers are more comfortable than older generations in contacting their bank or credit union without having a conversation with an actual human. 90% of the Silent Generation (born 1925-1945) have a preference towards human service over the phone, while only 12% of Millennials prefer phone, with nearly all others looking for chat, social or text channels.

Finn AI is a Canadian company that provides financial institutions with a chatbot that integrates into legacy core systems and conversational apps such as Facebook Messenger. They are currently working with tier 1 and tier 2 banks across four continents, to automate hyper-frequent front office tasks and chop the time support staff spend on such activities in half.

Finn AI is a virtual banking assistant that uses natural language to understand what users are asking. The technology leverages multiple data sources to extract information including data aggregators (such as MX), core banking systems (like Temenos), credit bureaus, card networks and others. Finn AI uses machine learning and natural language processing to create user insights so bank customers can receive personalized advice based on their characteristics, sentiments, and financial profiles.

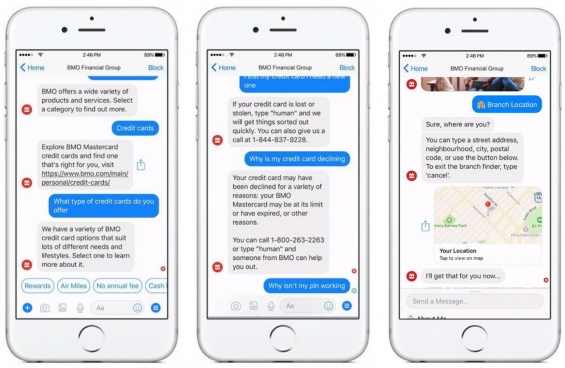

Bank of Montreal has already announced that its partnering with Finn AI to create a personal banking chatbot for consumers dubbed BMO Bolt. Bolt can answer 250 common questions and will learn to answer additional questions as the number of interactions it has with people increases.

BMO’S ‘BOLT’ CHATBOT AUTOMATES MANY ROUTINE CONVERSATIONS IN BANKING

BMO’S ‘BOLT’ CHATBOT AUTOMATES MANY ROUTINE CONVERSATIONS IN BANKING

And with open banking gaining traction, you can expect to see more financial institutions roll out conversational interfaces that improve the consumer experience in ways similar to Finn AI. Banks like Barclays with its API Store and HSBC who has a developer portal are encouraging third-parties to build new apps and create more innovative platforms.

Read More: Banking Execs Say AI Will Separate Winners From Losers

The Power to Disrupt Product Innovation

The focus of most fintech companies using AI is to improve the consumer experience, but Autonomous predicts the real transformative power of AI will be in areas tied to product development. Banks and credit unions will be able to apply qualitative as well as quantitative data to manufacture financial products. For example, Upstart, a fintech lending platform, employs AI and machine learning to underwrite loans using alternative data such as schools attended, work experience and the consumer’s web behavior while applying for the loan online. Upstarts claims $1.9 billion in loans originated.

Upstart offers its platform for online applications, underwriting, verification and servicing to banks and credit unions. Digital-only BankMobile is using Upstart’s software to determine the creditworthiness of consumers with thin or no credit files