While many financial institution branches may not be profitable on paper, bank and credit union leaders should think carefully before closing the doors. Even in the digital age, branches remain a critical channel for many consumers. Closing too many branches too quickly in some areas could lead to bad public relations, brand damage, angry consumers and business customers, and other nasty surprises.

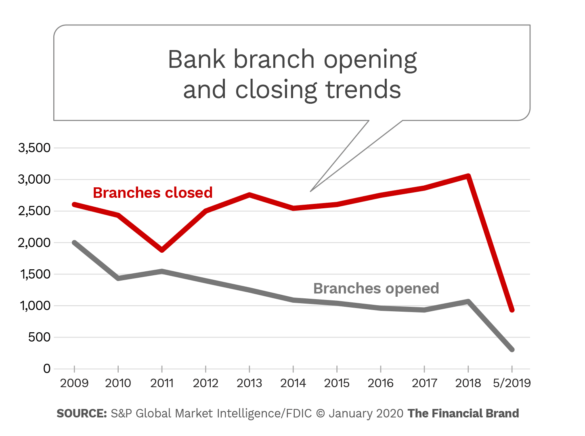

The pace of bank branch closures continues to increase. Banks closed nearly 2,000 brick and mortar locations in 2018, and more than 11,000 since 2012, according to S&P Global Market Intelligence.

Many financial institutions are cutting locations to reduce costs as consumers shift towards digital channels. Meanwhile, consolidations and acquisitions are also persuading managers to close redundant locations in some markets.

Here are five reasons banks should think twice before closing branches:

1. Many Consumers Still Like Bank Branches

Consumers are doing more of their banking online and with mobile devices. A survey by the American Bankers Association found that while nearly three-quarters of consumers most often access their bank accounts online and on mobile devices, less than a fifth conduct transactions in person.

Yet that one-fifth is still an important part of the consumer population, and an even greater number of people rely on branches at least part of the time.

“Banking in person at branches has consistently maintained its appeal to a large number of people. While many consumers have a favorite banking channel, we’re continuing to see most bank customers use a mix of the account management methods available to them,” said Nessa Feddis, ABA’s Senior Vice President And Deputy Chief Counsel For Consumer Protection And Payments.

While it may seem contrary for a generation that grew up in the digital age, even younger consumers like branches. A survey by CivicScience found more than half of those under age 25 visit a bank branch several times per month while a fifth visit branches a few times per week.

Local branches also sponsor events, handle volunteer outreach, and take part in the community. Some people actually maintain relationships with their local bankers, even if it’s just to cash a paycheck every Friday. And whether they’re wrong or right, there’s a segment of consumers out there who believe in-person banking is safer than online.

It’s not necessarily branches that are becoming irrelevant — the branch format is.

Accenture said in its Global Financial Services Consumer Study that consumers of all types still value face-to-face support when undertaking certain banking activities. In areas where physical channels are important, providers should develop their branches into “experience hubs” that offer digital services.

“They should leverage their physical footprint and integrated physical and digital services to meet customer needs more effectively,” Accenture said.

That means banks may implement more technology, reduce staff, and maybe even downsize to a smaller footprint. But it doesn’t mean the first step is to close the doors.

2. Institutions Risk a Loss of Trust When They Shutter Branches

E-commerce companies like Amazon and Alibaba have built multi-billion businesses without any physical presence. Yet with something as personal as money, consumers see branches as a “symbol of trust,” for safekeeping funds and depository functions, according to Deloitte.

Many find a level of assurance just knowing a branch is nearby. They know they have a place where they can interact with people and even close their accounts if they want to.

And at a time when digital interactions are the norm, in-person handshakes and eye contact instill a level of trust that apps can’t. While they may want digital options to start or conduct part of the process, 57% of consumers said they would still prefer to communicate with a lender by phone or in person during the process, according to an Ellie Mae survey.

Closing branches may not create an immediate exodus of consumers and businesses, but it can erode goodwill. Some people may be left questioning your institution’s commitment to the community — or even your viability.

Read More: Do the Majority of Americans Really ‘Want’ to Use a Branch?

3. Closing Branches Can Tangle Your Brand in Bad PR

Nowadays, any bank closing more than a branch or two at a time risks a potential PR backlash and had better have a story to spin for the media. It likely won’t look good if those closures happen to be in rural or urban poor areas. The Federal Reserve noted in a November 2019 report that nearly 800 rural communities lost more than 1,500 bank branches between 2012 and 2017. :

“Rural counties deeply affected by branch closures had higher poverty rates, lower median incomes, a higher share of their population with less than a high school degree, and a higher share of their population who were African American,” said the report.

JPMorgan Chase found itself the subject of a Bloomberg report when it closed its last branch in Aberdeen, Wash., in 2019 while opening numerous branches in wealthy parts of Washington, D.C. Bloomberg also noted that Chase closed branches in poor areas of the Bronx and Washington Heights while opening new ones in upscale areas of Manhattan.

A JPMorgan spokeswoman told Bloomberg the data was “skewed” and that Chase has significantly more branches in low-to-moderate income neighborhoods than any other competitor.

Still, it’s an example of the kind of PR closings can attract.

In small, struggling communities, even one branch closure can result in blowback when it’s one of the only financial institutions in town. NBC News noted the small community of Itta Bena, Miss., has become a “banking desert” after the last banking office closed in 2015.

“The bank branch is to local economies what the debit card is to your wallet — a key point of contact to the financial system and the way a large part of the population accesses non-predatory financial services,” said Jesse Van Tol, CEO of the National Community Reinvestment Coalition, an association of community development organizations.

Read More: Top Branch Trends for Banks and Credit Unions

4. Some Things an Income Statement Doesn’t Tell You

One out of four branches don’t break even, and only half of branches achieve what is considered an acceptable level of profitability, according to data from Peak Performance. That can make closures seem like a no-brainer.

Guenther Hartfeil, senior consultant at Peak Performance Consulting Group, told The Financial Brand that with annual operating costs of $600,000 to $800,000, the typical branch needs roughly $25 million in deposits to achieve a breakeven.

“The problem is clear: Too many branches that have too few customers, and are not growing at a sufficient rate, to ever achieve breakeven, let alone desired ROI,” Hartfeil said.

Yet while deposits, balance sheets, and income statements may gauge financial viability, they can’t measure things like brand reputation or customer perception.

Sometimes a financial institution may not realize how important their branch is to the community until they close the doors. Branches are especially important for small businesses where the relationship between bank staff and business owners allows more confidence between lender and borrower.

“When local branches close, those relationships are lost, resulting in the loss of credit that local businesses need to thrive,” said Jason Richardson, Director of Research and Evaluation at the National Community Reinvestment Coalition.

Branch closures can also lead to diminished brand reputation and disgruntled locals when it leads to layoffs. Many will take to social media, forums and discussion boards.

Financial institution leaders should also take note how closures may impact certain demographics. For instance, while Millennials may more willingly accept branch closures, it could put off older — and often more profitable — consumers, James Barth, finance professor at Auburn University told S&P Global Market Intelligence.

“That’s the trend that not everyone is capturing,” said Barth. “Older people generate most of the profits, and they go to branches more, so the banks need to keep them open.”

Read More: Don’t Abandon Branches to Favor Digital Banking Channels

5. Closures Could Impact Certain Lines of Business More Significantly than Others

Closing a branch could have a negative impact on account openings and loans in that community.

Deloitte noted in its Global Banking Survey that branches remain the dominant channel for opening new accounts, and for complex products such as loans. And for the most part, that preference is uniform across all age groups, from 64% of Baby Boomers to 56% of Gen Z consumers.

Banks and credit unions shouldn’t look at branches as standalone channel. Instead they should determine how they fit into the overall digital transformation strategy.

“Our survey findings tell a compelling story about the unique value branches can provide to customers and the key role branches often play in building and sustaining strong retail banking franchises,” Deloitte said.

If your institution serves a small market and will have little or no physical presence in some markets, you’d better ensure your digital strategy is ready to step up to the plate. At a time when many banks and credit unions are turning their branches into advisory centers, closure could also result in lost opportunity.