The accepted wisdom among many in financial services is that younger consumers — more focused on ethics and integrity generally — are more skeptical of financial institutions, and prefer to deal with (or to work for) the most innovative companies.

New research based on input from thousands of consumers around the world basically throws cold water on those two notions.

In a nutshell: Younger people worldwide tend to trust and like banking providers more than older people do. “Purpose”-related factors are more important to most consumers than product offerings and innovation. In fact, innovation ranked lowest pretty much across the board as a consumer preference. Integrity and authenticity are consistently the top drivers of consumer preference in financial providers, including among Millennials and Gen Z.

While in many ways the findings seem counterintuitive, the research, conducted in the first quarter of 2019 by Calib on behalf of the European Association of Communication Directors, explores how the findings fit a logical pattern.

One of the strongest positive takeaways from the findings is this: “While the trust crisis was and still is deep and serious, banks still stand a chance to repair it going forward since the younger population is more positive and possibly less judgmental than they think.”

Reputation Recovery Well Under Way

The ongoing string of scandals that perpetually bedevils the banking industry would lead many to believe that the industry ranks low on trust and likeability. The Caliber/EACD study sought to establish whether trust has been restored. Using an index they call the “Trust & Like” score, the research found that the reputation of the financial industry turns out to be quite robust — close to the average of thousands of companies across different sectors and countries. (The results were somewhat influenced by the fact that the study covered both banks and insurance companies. The latter, it turns out, are more trusted and liked than banks, but banks have made progress.)

The Trust & Like score includes a range of attitudinal perceptions relating to whether consumers consider a given company to be innovative, differentiated, authentic or inspiring, has compelling products and demonstrates leadership. The study found that while differences exist geographically in the overall scores (institutions in China and Brazil, for example, generally score higher than those in Europe and the U.S.), the public expectation of responsible behavior is universal. “If a bank fails this expectation, its reputation will suffer greatly, irrespective of where in the world it is based,” the report states.

In the table below — showing a portion of the 68 banking providers covered by the survey — many of the institutions in the low/very low range are recognizable names from news headlines: Denmark’s Danske Bank for money laundering issues, Germany’s Deutsche Bank for management issues, Wells Fargo Bank for its account-opening fraud issues, etc.

How consumers rate selected banks by degree of ‘trust and like’

| Bank | Like/Trust Level |

|---|---|

| Bank of China (CN) | Very high |

| Caixa Economica Federal (BR) | High |

| UniCredit (IT) | High |

| JPMorgan Chase (US) | Average |

| Citibank (US) | Average |

| BBVA (ES) | Average |

| Barclays (GB) | Average |

| Swedbank (SE) | Average |

| Bank of America (US) | Average |

| HSBC (GB) | Average |

| Caixa Bank (ES) | Low |

| BNP Paribas (FR) | Low |

| Wells Fargo Bank (US) | Low |

| Deutsche Bank (DE) | Low |

| Danske Bank (DK) | Very low |

Source: EACD/Caliber

Hope From the Two Youngest Consumer Segments

Members of Gen Z and the slightly older Millennial generation together represent a huge portion of the current and future customer base for banks and credit unions. The two groups are different in many respects, but the general consensus is that they tend to be more skeptical of financial institutions than older generations.

The Caliber/EACD data found the opposite to be the case, however. The youngest respondents (those 18-24 at the time of the survey, and thus part of Gen Z) express the highest level of trust and like towards banking providers worldwide, followed by those age 25-42 (Millennials). The most critical responses came from the next two oldest cohorts — members of Gen X and the younger half of the Baby Boomers.

While the trust crisis was and still is deep and serious, the report states, banks and credit unions still stand a chance to repair the reputational fallout going forward since the younger population — who will increasingly form the consumers, employees and influencers that matter to financial institutions — is more positive and possibly less judgmental than they think.

Read More: 15 Things Banks & Credit Unions Must Know Before Targeting Gen Z

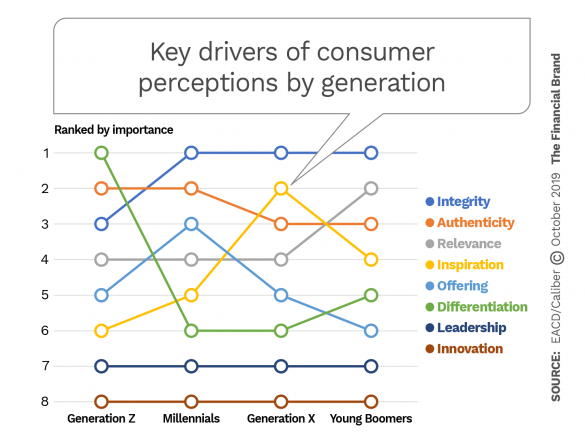

Factors Most Important to Younger Consumers

The Caliber/EACD report analyzed what it calls the generational reputation drivers, with a particular focus on Millennials and Gen Z.

“One thing that became clear was that of all the dimensions we measured, the one that drives the Trust & Like Score the most is integrity,” the report states.

Out of eight attitudinal perception factors the survey probed, integrity was considered most important by consumers in every generation except Gen Z, where it was still ranked third. As the chart below shows, integrity beats out innovation, leadership, differentiation (other than with Gen Z) and, to a lesser extent, “offering,” which refers to the attractiveness and effectiveness of products offered.

The report suggests that what matters most to people worldwide, irrespective of age, is not financial institutions’ products and services and not their innovation or differentiation — even though those are the elements that preoccupy many marketers as a means to drive preference and loyalty.

“What actually matters most to people when it comes to building trust in financial institutions,” the report states, “is that these institutions demonstrate a responsible behavior.”

In addition, it means that some of the widely discussed topics in the financial community — CEO activism and data privacy ethics — are in fact relevant and very important to consumers.

Although they differ on some points, both Millennial and Gen Z consumers agree that authenticity is important in a financial institution, which relates to integrity.

The report states that the low position of innovation in the rankings of factors considered important by consumers should be cause for reflection among financial institution marketers. The industry “seems nearly obsessed with communicating its innovation and thus competing with fintechs,” they state. That’s not surprising given the amount of attention the “fintech invasion” gets, and which the report authors agree is a major threat. But innovation per se isn’t what consumers look for.

This survey suggests consumers of all ages, but especially Millennials and Gen Z, “prefer to understand better how companies behave, what they stand for and what makes them interesting and different. Focus on innovation seems like the wrong strategy for improving reputation and becoming more attractive.”

Read More: Why Some Financial Brands Win With Millennials (and Some Don’t)

Purpose and Product Both Important

As the researchers studied the responses to determine whether any of the eight factors would be likely to move in tandem, three clusters emerged from this analysis: “product,” “purpose” and “progress.”

Of these, purpose is the most significant for financial institution marketers. It includes integrity, authenticity and relevance from among the eight factors. “Purpose is the set of attributes that has the highest influence on people’s tendency to support financial companies by recommending them … buying their products and considering to work for them,” the report states.

As shown in the table below, banks and credit unions that can be considered purpose-driven enjoy higher support compared to product-driven companies — those receiving higher scores on product offerings, differentiation and inspiration.

Consumer support for two types of financial institutions

| Purpose driven | Product driven | |

|---|---|---|

| Recommendation | 29% | 24% |

| Advocacy | 30% | 25% |

| Consideration | 30% | 26% |

| Employment | 26% | 26% |

Source: EACD/Caliber

The report acknowledges that this may sound counterintuitive considering that, as noted, one of the biggest threats to institutions today comes from nimble fintech competitors offering what many perceive to be better and more innovative products and services. It’s clear from marketplace results that compelling and innovative products and services do matter, especially to younger audiences.

The report’s authors don’t advise financial institutions to stop trying to offer more innovative and user-friendly products as a way to meet fintech competition. However, for many institutions the best way to do that may be to partner with fintech providers, many of whom are eager to join forces with banks and credit unions.

Also, as noted above, differentiation is very important to Gen Z. Banking is gradually becoming less commoditized, but bank and credit union marketers may need to work harder to sharpen their perceived differentiation, the report notes.

To win the hearts and minds and wallets of Millennial and Gen Z consumers, traditional financial institutions “must ensure and continuously prove that they are driven by a unique purpose,” say the authors. That should be driven by being authentic, demonstrating integrity and offering compelling services.