The rollout of the much-discussed Apple Card unleashed an avalanche of media coverage only a few months after a pre-launch announcement stirred up a similar media frenzy. It’s the Apple mystique. Everything they do is seen as larger than life.

But, really, this is about a credit card. How could that be a threat to traditional banks and credit unions? It’s not like this is about Amazon moving full-bore into banking.

While Apple is very different from the ecommerce giant, the two do share one thing in common: They’re both customer experience companies. Apple has built a consumer product empire on seeking out ways to improve the consumer experience in computing, music, phones and more. Most people think of Apple as a product company, and they sell billions of products to be sure. But always the focus is on the design, the function, the experience.

The company has explored co-branded cards before, and has an existing arrangement with Barclaycard. But the Apple Card is at another level altogether, being mainly a virtual card integrated into Apple Pay, the company’s mobile wallet launched in 2014. As Ben Bajarin, Principle Analyst with Creative Strategies, observes, “The opportunity for Apple to insert themselves into payments was clear with Apple Pay, and extending into the banking arena is a natural progression.”

And they’re extending in partnership with Goldman Sachs, the Wall Street giant, itself already deeply embedded in retail banking with its Marcus brand.

It’s likely that if the relationship is successful, it won’t stop there. As it is, in the view of several industry observers, the Apple Card is already much more than “just a credit card.”

A Virtual/Physical Combo With User-Friendly Features

Briefly, the card is primarily virtual, residing in the Apple Pay wallet. The card also exists as a physical card, a stunning white-titanium card containing a chip, issued for free, on request, to be used in places that don’t accept Apple Pay — or don’t have NFC (near field communication) capability. Apple says about 70% of U.S. merchants accept Apple Pay.

Read More: Is Apple’s New Credit Card The Next Big Thing in Banking?

The card has no fees, and offers cashback rewards of 3% on purchases made directly with Apple using the card in Apple Pay, 2% on all other purchases made using Apple Card on Apple Pay, and 1% for all purchases made with the physical cards. These rewards, about average in the highly competitive card rewards market, feature an unusual twist: they are paid daily and available to use for (almost) any purpose in the Daily Cash feature of the Apple Card app. Apple says it will extend the 3% cashback reward to additional merchants and has already added Uber and Uber Eats since the initial release.

A large selection of money management features is also part of the Apple Card experience: weekly and monthly spending summaries grouped in color-coded categories; an interactive tool to see how much interest will be charged at any amount a consumer decides to pay.

Surveys Predict Strong Uptake for the Card

The Apple Card was released on a limited basis to people who had requested to be notified when it was available. That was followed quickly by a full rollout. The expectations were for strong demand.

In a survey done about three months after the initial announcement, J.D. Power found that 38% of U.S. adults were already aware of the Apple Card. Among Millennials, the percentage was much higher — 52%. Further, of those who were aware of the new virtual card, 35% said they were either very likely or somewhat likely to apply for it. The research firm concluded from this and other factors that the Apple Card would be a hit, according to Jim Miller, Vice President Banking and Credit Card Intelligence.

In a survey conducted earlier, Cornerstone Advisors found that more than one in five Millennials intended to apply for an Apple Card. As Cornerstone’s Managing Director of Research, Ron Shevlin, notes, “If the Millennials who said they’ll apply for the Apple Card actually do (and are approved), Apple will have the second-highest market share among young Millennials behind Capital One, and third-highest market share among older Millennials, tied with American Express behind Capital One and Bank of America.”

Shevlin points out, however, that consumers rarely do what they say they’ll do in a survey. Also, 42% of the respondents didn’t have an iPhone, and while they could still apply for an Apple Card and use the physical card, that would seem unlikely.

Even if demand isn’t as strong as expected, various people have noted that other Apple products have seen slow adoption at first, notably the Apple Watch … and Apple Pay.

“Apple has always been great at the long game — getting the critical pieces in place over time to deliver a game-changing experience. This is the early beginnings of “The Bank of Apple’,” notes Dominic Sancto, an independent artificial intelligence software developer, in a LinkedIn post.

Read More: Great Mobile Banking UX Demands More Than a Flood of Features

Strong Impact Likely on Traditional Credit Card Issuers

The Apple Card’s marketing message is very powerful:

- No fees

- Help consumers pay less in interest

- Instant issuance and immediately available to use (the virtual card)

- Privacy protected and data won’t be shared

- Easy to get help via 24/7 text.

“This is where it’s an advantage for Apple and Goldman to be new entrants,” Jim Miller tells The Financial Brand. “They don’t have to worry about cannibalizing existing business by eliminating those fees.”

If the card becomes popular, that could put pressure on traditional card issuers to follow suit, hurting profits.

“While [Apple Card] competes with other credit cards, which offer similar things,” says Ben Bajarin, “it is the total experience and the sum of its parts that separate it from the pack. It is a fully integrated experience, something Apple does very well, and its deep integration with iPhone is a differentiator.”

“Ultimately,” says Bajarin, “I think Apple will raise the bar, and other credit card companies will likely feel pressured to step up their game.”

Maybe more than “credit card companies.” The Apple Card experience will likely raise consumers’ expectations for frictionless banking, once they’ve had a taste of it.

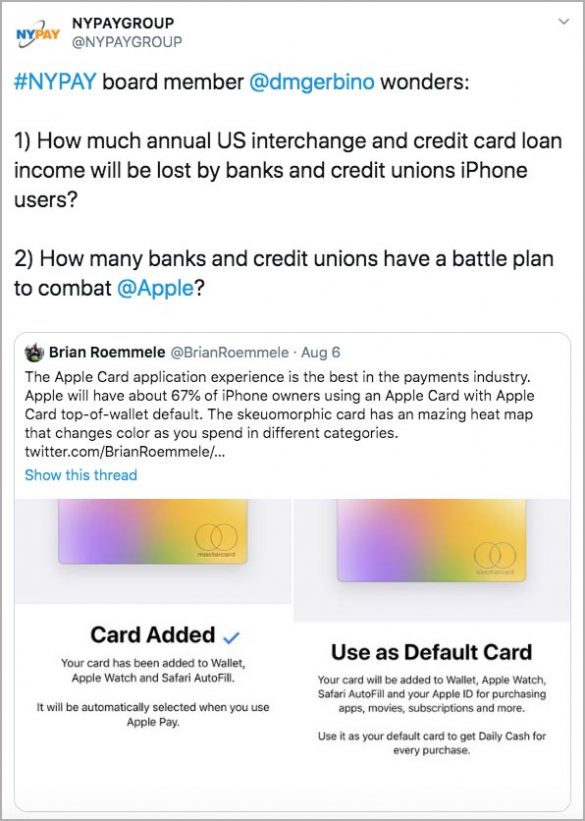

As analyst and author Brian Roemmele observed after the initial announcement: “Apple has reengineered everything” about the credit card user experience. The Founder and President of Read Multiplex only increased his enthusiasm once the cards began to be issued. “The Apple Card application experience is the best in the payments industry,” he says in a tweet. “Apple will have about 67% of iPhone owners using an Apple Card with Apple Card top-of-wallet default,” he predicts.

There were 102 million iPhone users in the U.S. in 2018, according to Statista. Apple Pay requires Touch ID, which arrived with the iPhone 5S, but most of the 102 million Apple phones are that model or newer.

From Zero to Spending in Three Minutes or Less

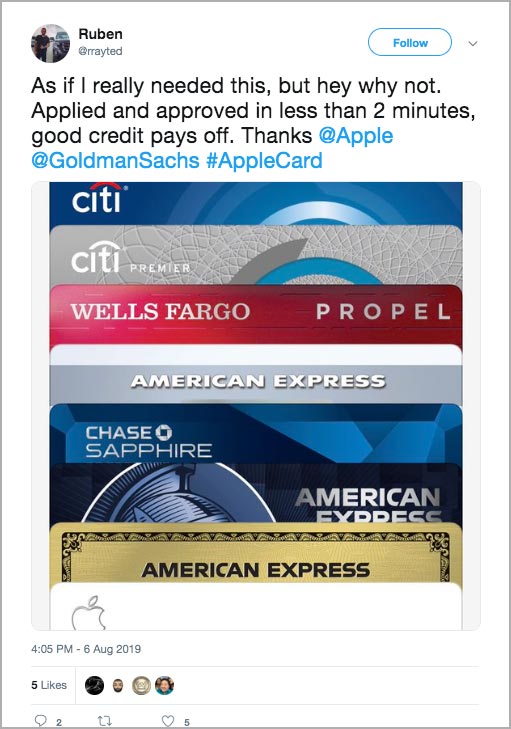

Richard Crone, an influential voice in the payments world, wrote on LinkedIn that he was able to use his new virtual Apple Card within three minutes of receiving the invitation by email.

“The Apple Card raises the bar for true, mobile account opening and instant issuance, a standard that no other bank can match,” Crone wrote. “Last week, Goldman didn’t know me; yesterday within three minutes they extended me a generous credit limit that I could start spending immediately.”

“Onboarding is one of the biggest drop-off points for users,” states 9to5Mac in a tweet. “[Consumers] need to give companies a significant amount of personal information before they can access the actual product, which requires a lot of trust in a brand.”

Legacy financial institutions still have an edge in consumer trust. J.D. Power found that 59% of iPhone users surveyed trust their current bank or credit union to protect their personal data and privacy compared with 49% who say they trust Apple. Only 12% trust Facebook. But data from The Digital Banking Report show that the majority of traditional banking providers don’t yet have the kind of frictionless mobile account opening and activation processes that Apple has now made a reality, although the number is rising.

Apple Card the Next Step to… Apple Banking

Will the Apple-plus-Goldman card venture be the launching point for banking by Apple?

“An [Apple] checking product would make a ton of sense as the next step, particularly for younger consumers who really like debit cards.”

— Jim Miller, J.D. Power

“A checking product would make a ton of sense as the next step, particularly for younger consumers who really like debit cards,” J.D. Power’s Miller maintains. He predicts that Goldman Sachs will launch a checking account one way or another — under its Marcus brand or with Apple. Miller believes they would have more success combining it with the Apple Card.

Banks will be angry in the future, “when they realize Apple has just stolen their customers [with Apple Card] when it decides to become a digital bank,” says Bill Field, Founder of Payments Global and Digital Money Group, on LinkedIn.

A Boost for Digital Wallets Should Help All

Several experts have noted that the Apple Card is Apple’s way of boosting the low usage rates of Apple Pay, its digital wallet.

Launched in 2014, it was the first mobile wallet in the U.S. market but is only actively used on about a quarter of U.S. iPhones, according to Loup Ventures. But no mobile wallet has been a big winner in the U.S. compared with China and several other countries where they dominate payments. The question is whether the Apple Card will be enough of an incentive to convince U.S. consumers to break the plastic habit.

The ability of rapid transit commuters in New York, Portland, Ore., and other cities to use Apple Pay (and other NFC wallets or contactless cards) to pay their fares, could begin to hasten adoption.

Jim Miller sees Apple Pay as the real winner from the Apple-Goldman card venture. Launching Apple Card as primarily a virtual card, encourages consumers to use Apple Pay. “If people see the person in front of them waving their phone to make a payment,” says Miller, “even if they don’t sign up for the Apple Card, if they have a Chase or Citi card in their Apple wallet, Apple gets a cut of that, so that’s another area where Apple’s going to win on this.”

The analyst believes that Apple Card may in fact benefit the banking industry in the sense that it drives up usage of mobile wallets and drives down consumer use of cash.

Daily Cash: Possibly Apple Card’s Secret Sauce

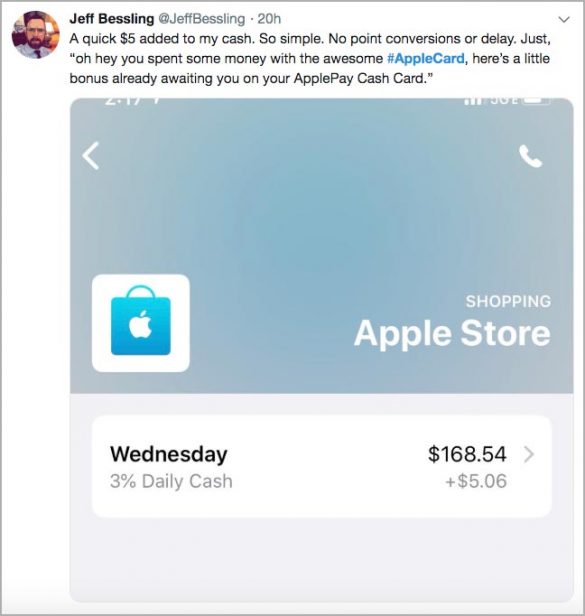

Critics have said that most people aren’t spending that much in a given day or week to see any significant amounts add up in a daily cash feature. 30 cents here or $1 there doesn’t compare favorably to redeeming points for something sizeable like an airline ticket or a significant amount from one of the higher-paying cash reward cards.

That said, Apple Card’s Daily Cash feature is embedded in the Apple Wallet where a consumer can not only see, but use, any available cash at any time right from the wallet. That’s potentially powerful versus having to stop to look something up and make a transfer or take additional steps to use the cash or points, observes Miller.

Some consumer social media comments suggest that Apple may be on to something with Daily Cash.

Not only everyday consumers. Ben Bajarin, who is an Apple Card user as well as an analyst, observes how the cash rewards feature is habit-altering. Even though he often used Apple Pay, he says that at certain stores he still pulled out his credit card, even though they accepted Apple Pay. “All of that changed once I got Apple Card,” he says. “The 2% cashback was the start, but seeing that daily cash show up on a daily basis was even more psychologically rewarding.”

Anecdotal evidence, to be sure, but clearly the feature deserves close attention by all financial services marketers.