Ever since JP Morgan declared itself a technology company that provides financial services — not the other way around — analysts and investors have been scrambling to discern which banking companies are doing tech well, and which are not. They know the institutions that harness the power of artificial intelligence, machine learning and big data, and more importantly, the applied business insights these technologies can generate, will be the banks that will be the winners in the long run.

“Long term I think this will determine the split between winners and losers,” one investor told the Financial Times in a story on AI and banking earlier this year.

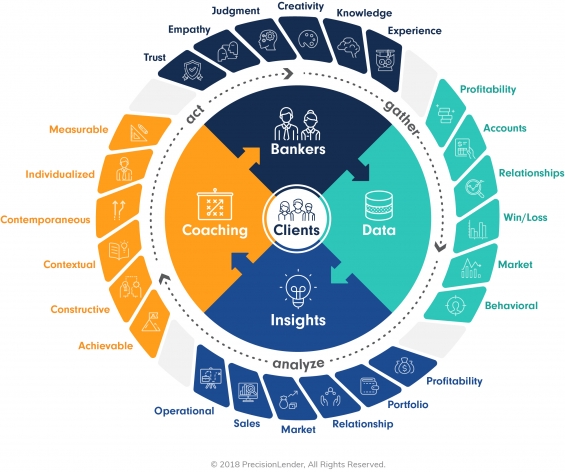

Virtues of a Circular Process

But what does it mean to “harness” the data? It means moving along a circular rather than linear process that starts with your bankers. First, you gather data on what customer actions your bankers took and what outcomes resulted. Then you analyze that data to get valuable insights. Next, you translate those insights into specific coaching that you deliver back to bankers so that they can act on it. Finally, you gather data around which actions led to improved outcomes and the insights “flywheel” spins faster.

Banks have spent billions of dollars on “big data” projects to gather data, and billions more on data science teams to analyze that data to transform it into insights. Despite this level of investment, McKinsey reports that “many boards are pressing for answers about the scant returns on many early and expensive analytics programs.”

The main reason: most advanced analytics and AI projects are dying at the “last mile” of the Applied Banking Insights Flywheel. They fail to translate insights into coaching that drives different and meaningful action. And even when they do, it has been nearly impossible to measure the impact and attribute it back to its source.

To truly deliver value, a bank must build and invest in all the parts of its flywheel. Gordon Ritter, founding partner at Emergence Capital Partners, calls these learning loops Coaching Networks and believes that they are the future of software. Ajay Agrawal, an Economics Professor at the University of Toronto and co-author of the book Prediction Machines: The Simple Economics of Artificial Intelligence, describes this learning loop as The Anatomy of a Task. And you can trace its origins back even further to W. Edward Deming, the father of modern quality and his Plan-Do-Check-Act Cycle of continuous learning.

Five Traits Separating Posers From Performers

Keeping this in mind, how do you separate the posers from the performers? How do you determine which AI and advanced analytics projects will most likely deliver real, tangible value?

Here are five assessments that provide a helpful lens:

1. Beware of Innovation Theater

Be skeptical when a bank or credit union answers questions about its AI program by touting its Innovation Lab. Be doubly wary if their PR kit includes an image of a stock photography model sitting in the “branch of the future” wearing a virtual reality headset while flying a drone.

Putting an Innovation Lab in a showroom is lots easier than deploying AI effectively in the back of the bank. But the back of the bank is where business results live. Be less interested in the window dressing, the hoodies and the foosball tables, and more interested in the women and men doing the hard slog in cubicles.

Innovation Labs have their place. But they should be focused like a laser on innovations that advance the bank’s business strategy in a measurable way. Again, the last mile of the flywheel is the most important — and that’s where too many of these innovations die.

Always understand the pathway to action. Very simple questions that will expose this fatal flaw include: “Who is the audience for this insight?” “What do you expect them to do differently based on it?” and “How will you know the impact?”

2. Beware of Strategic Misalignment

Make sure the bank’s AI & analytics strategy exactly reflects its overall business strategy. Some banks might have a need to attract deposits, and so a retail innovation strategy makes sense. Other banks need to deploy those funds, so a commercial lending innovation strategy makes more sense — even if commercial innovation work is less visible to the “Street.”

There are many banks doing incredibly innovative things using AI and machine learning deep within the bank. They’re having a meaningful impact on the bank’s business. There’s no PR budget behind it. They just put numbers on the board and point to the scoreboard.

3. Is AI being used to help or to harvest?

We’ve all seen the backlash against Facebook and other social-media platforms for using AI to harvest data for commercial purposes. Banks, as fiduciaries, are never going to sell their customers’ data to advertisers. Banks have the opportunity not just to be fiduciaries of money. They are ideally positioned to be fiduciaries of trust.

“If a bank starts saying, ‘How can we extract more value from our customers?’ then AI becomes a strip-mining tool”

That means using big data to benefit their customers, not to exploit them — to help, not to harvest. The question should be, “Are we using big data to make the bank more valuable to the customers, so the customers will be more valuable to the bank?” That’s sustainable, and you can do that with gusto.

But, if a bank starts going down the road of, “How can we optimize this and extract more value from our clients?” then AI becomes an extraction tool. A strip-mining tool. Ultimately, customers will discover this. And that’s how brands get destroyed.

4. Build ‘Ironman Suits’ — Not Terminators

Most stories on AI in banking focus on its potential to generate short-term margin by eliminating jobs. More often than not, this is short-sighted. Technology inevitably will realign work, but reductions don’t always follow. Nor should they.

As Daniela Fernandez of the Wall Street Journal wrote compellingly in a recent story, “AI’s ability to drive significant performance enhancements rests in conjunction with people, not in place of them. Much of AI’s highest return will require adding jobs.”

At the top and center of the Applied Banking Insights Flywheel are bankers. Better data is used to produce better insights which are used to produce better coaching which produces better bankers and the continuous improvement cycle repeats. The goal should be to do everything that machines can do well so that bankers can do what humans uniquely do well (empathy, trust, experience, etc.).

The technology should surround and enhance the banker just like Tony Stark’s Ironman suit. All too often, AI projects accidentally destroy the humanity that is essential for superior client experiences.

5. Beware banks that ’embrace failure’

Every time you hear an innovation consultant proclaim that a bank needs to “embrace failure,” you should cringe. Failure sucks.

It’s not about failure. It’s about learning. You don’t embrace failure — you tolerate it because you love learning. The goal is to create an organization and culture that is so obsessed with continuous learning that it can manage, mitigate, and, if necessary, tolerate failure.

When you succeed, you capture and embed what you learned. And when you fail, you learn twice as much or twice as fast. This is what author Angela Duckworth calls “Grit,” or as my friend who was a Navy Seal says “Innovation is hard. Embrace the Suck.”