When it comes to video in the banking industry, there are two basic approaches: one where people using their own device (either a desktop computer, laptop, mobile phone or tablet), and in-branch video banking that requires consumers to set foot inside one of the banking provider’s brick-and-mortar locations.

Which direction should banks and credit unions choose? Or both?

To answer that question, Vidyo, a provider of two-way video solutions in the banking industry, has been studying trends from both perspectives — which approach financial institutions currently offer, and how consumers interact with them. For three straight years, Vidyo has fielded an annual survey looking at how retail delivery strategies are evolving at banks and credit unions and where video fits in.

In years past, banks and credit unions were much more likely to deploy in-branch solutions, largely because they have more control over security. In this year’s study encompassing of more than 4,100 consumers and over 280 financial industry professionals, Vidyo found that the two approaches — online video and in-branch video banking — are now just about on equal footing.

Today, four out of five bank and credit unions either already offer- or plan to offer video banking. A fifth of these are running a fully-operational service, while one-third say they are currently in the pilot stage. And two-thirds of respondents in Vidyo’s study said they expect to see both approaches used in their financial institution in the near future.

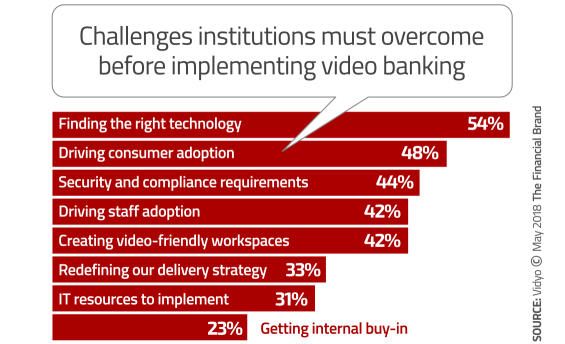

For those few banks and credit unions that are not planning on offering video banking, 62% say it just isn’t a priority, while 40% cite a lack resources to implement such a service.

Seeing the Benefits of Video

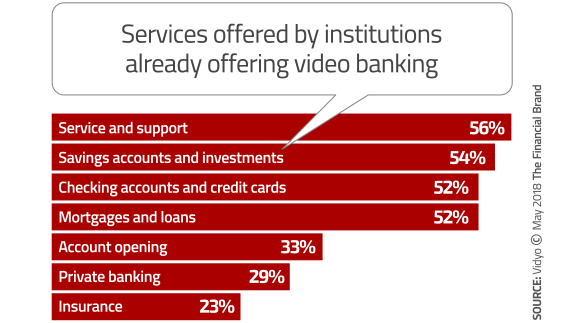

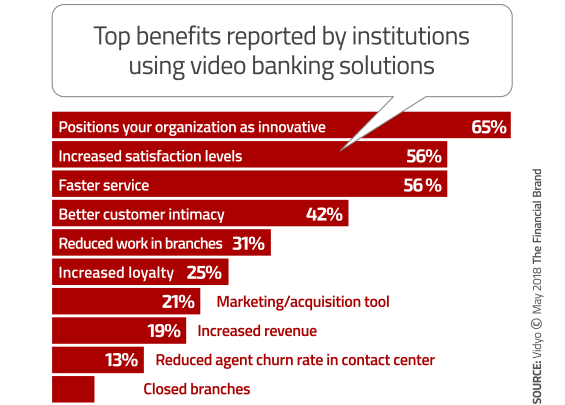

The most common video banking services banks and credit unions offer are support, followed closely by savings accounts/investments. The top benefits of video banking they cite include positioning their institution as innovative, and that consumers get faster service and are more satisfied.

Banks and credit unions that already offer video banking say that it impacts their business. Three-quarters report better outcomes, 97% report that NPS scores for video banking are at least as good, if not better, than other channels. And 77% say sale close rates are better or at least equal to other channels.

Getting Consumers Onboard

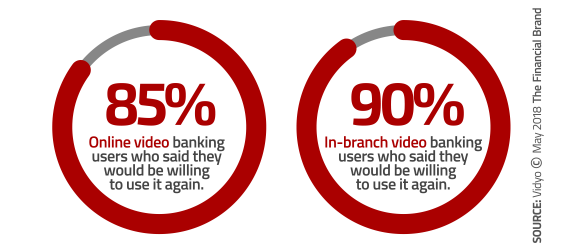

The good news is that the vast majority of consumers who try video banking give it a thumbs up. Somewhat surprisingly, those consumers who have used in-branch video banking are slightly more satisfied with the service than those who used online video via a desktop computer, laptop, mobile device or tablet. One reason explaining this could be that consumers accessing video banking from their own devices are more likely to run into technical or user issues.

Regardless of age, gender or socioeconomic status, consumers are generally open to trying video banking if/when their bank or credit union asks them. According to Vidyo’s research, it’s inaccurate to assume that younger, more upscale consumers are those most likely to accept video banking.

However, about a quarter of consumers are unwilling to give video banking a try. Of those consumers rejecting video banking, 27% say it’s because they didn’t think that video banking would help them perform banking transactions and 36% say that if they are going to make the effort to get to a branch, they want to speak face-to-face with a person.

Before implementing video banking — or working to improve the service if you already offer it — Vidyo says you need to figure out how you can leverage it across the entire organization. Don’t think in silos but consider how video can be relevant to multiple business units and address a range of needs/services, including lending, service contact center, retail delivery and even wealth management.