Although Millennials may not be settling down in the suburbs in their 20s like the last two generations before them, they still want to pursue the American dream of homeownership. According to research from TransUnion, almost three-quarters of Millennials who don’t already have a home plan to purchase one in the future — a move that will require a mortgage loan.

And sure, Millennials may be heavy users of ride-sharing services like Über and Lyft, but four in five either own or lease a car. As it turns out, TransUnion found Millennials have actually opened auto loans and leases at a rate about 2-3% higher than Gen X.

But let’s assume for a second that even if Millennials had a lower appetite for debt than their predecessors (which they don’t), their sheer numbers would make up for it. Today, there are more Millennials than Baby Boomers, and Gen Z — the next generational segment — is about the same size as Millennials. This means there’s a big demand for lending products, and retail financial institutions can count on an expanding need for lending products, possibly at the highest levels ever seen.

Bottom line? Millennials are an attractive lending market. Even though many struggle with student loan debt and try to resist burdensome credit card balances, most are able to successfully manage debt, sometimes even better than previous generations.

Read More:

- How to Design a Millennial Bank

- Reality Check: Why Your ‘Millennial Strategy’ Might Be Completely Irrelevant

- Digital Lending Must Go Beyond Eliminating Paper

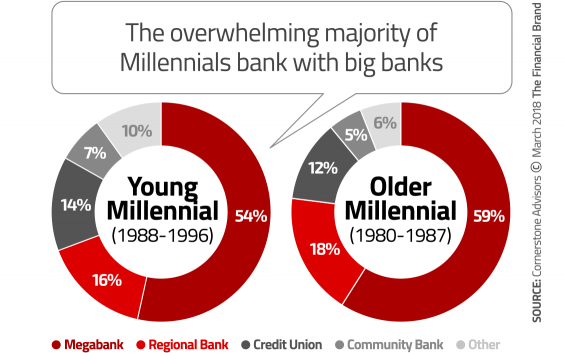

Megabanks Are Winning The Millennial Lending War

Millennials are not looking to community banks and credit unions for their lending needs, passing up smaller institutions in favor of the largest institutions.

“While many mid-sized financial institutions may have superior rates or services, Millennials are often selecting megabanks and large regional banks — those they already bank with — for their borrowing needs,” explains Ron Shevlin, Director of Research at Cornerstone Advisors.

It’s not that Millennials find larger institutions more attractive or that they simply want the convenience of bundling their lending needs with the same institution where they have their checking account. The reality is that these larger players are adapting more quickly to Millennials’ needs and expectations, rolling out innovative solutions that are more appealing.

For instance, Wells Fargo recently announced that instead of making consumers apply for individual loans or credit cards separately, the bank would allow consumers to apply for- and establish their overall credit limit — a singular total for all borrowing — and then allocate that credit across a range of different products. For example, someone eligible for $50,000 in unsecured credit who is planning on renovating their house might choose to allocate $25,000 to a credit card and $25,000 to a personal loan.

This offering is “shifting offers from product-centric to customer-centric,” explains Avid Modjtabai, the head of Payments, Virtual Solutions and Innovation at Wells Fargo.

To Shevlin, what’s particularly impressive about Wells Fargo’s move is that it represents a massive shift — perspective, processes and policies — requiring strategic alignment and coordination across multiple lines of business, something that usually stifles innovation at banking providers of all sizes but specifically megabanks.

Where Can Community-Based Institutions Find Their Lending Mojo

Smaller banks and credit unions will need to overcome a few headwinds to attract Millennial borrowers. First, Millennials tend to bank with megabanks, giving the largest institutions the incumbent’s advantage.

Second, smaller financial institutions have not been as successful as the largest institutions in cross-selling lending products. While 42% of Millennials have opened a credit card with their megabank, only 4% of Millennials have opened a credit card with their community bank. Credit unions fare better, with 31% of Millennials also having a credit card with their credit union.

Megabanks also outperform community banks and credit unions in cross selling mortgages and home equity loans.

| Millennials Who Got a Loan From Their Primary Institution |

Type of Financial Institution |

. Credit Card |

. Home Loan |

Home Equity Loan |

Other Personal Loan |

|---|---|---|---|---|---|

| Young Millennial (1988-1996) |

Megabank | 42% | 9% | 6% | 6% |

| Regional Bank | 20% | 2% | 2% | 6% | |

| Credit Union | 31% | 4% | 2% | 13% | |

| Community Bank | 4% | 0% | 0% | 9% | |

| Older Millennial (1980-1987) |

Megabank | 50% | 16% | 9% | 4% |

| Regional Bank | 24% | 10% | 7% | 11% | |

| Credit Union | 19% | 7% | 4% | 9% | |

| Community Bank | 18% | 0% | 0% | 5% |

Source: Cornerstone Advisors

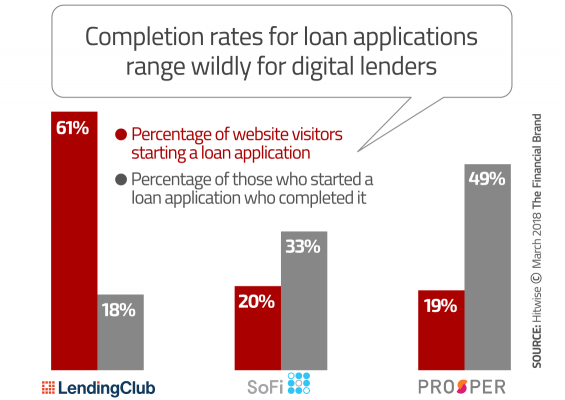

Outside Players Going After Millennials

In addition to megabanks, there is an onslaught of alternative, online and marketplace lenders gunning for Millennial borrowers. Their numbers are impressive, according to their websites:

- LendingClub – $33 billion borrowed, more than 2 million borrowers

- Social Finance (SoFi) – $30 billion borrowed

- Avant – $4 billion borrowed, 600,000 borrowers

- Prosper – $9 billion borrowed, 600,000 borrowers

What’s interesting is that each of the lenders or lending marketplaces above use only Millennial imagery on their websites. There are photos of Millennials buying their first home, Millennials graduating, Millennials hiking with other Millennials. Millennials at happy hour. You (quite literally) get the picture.

And it’s not just lip service; they focus on Millennial loan needs. Prosper offers adoption loans for young parents. SoFi says that it doesn’t just look at your credit score but considers your career experience, income vs. expenses, and your financial history.

But fintech startups like LendingClub and Prosper are suffering as Millennials have aged. Ten years ago, the market was hot since lending by traditional institutions had dried up; Millennials (and a lot of other consumers) had nowhere else to turn. But as the economy has improved — as presumably Millennials’ credit scores along with them —consumers have more options for loans, which puts pressure on alternative lenders’ margins.

Reinventing Consumer Lending

“To better compete with the large banks, community-based financial institutions will need to find new strategies,” stresses Shevlin. “While many smaller institutions believe they have superior rates and service, the cross-sell numbers don’t lie — Millennials are picking megabanks and super-regionals.”

If community-based banks and credit unions can’t differentiate on price or service, what’s the alternative? In a report Shevlin authored for Kasasa, he says they need to compete on product quality, and he proposes three tactics to do that:

- Providing flexible credit terms and repayment options

- Offer on-going access to future funds – durable credit

- Bundling accounts – e.g., checking accounts as part of a loan offer

More than half of Millennials would open a checking account if that’s what it took to get a loan with flexible term and faster payback capabilities.

In fact, more than half of all Millennials say they would choose a bank or credit union that gives them flexibility on monthly loan payments, assistance paying back the loan faster, and insight into how payments affect balances and interest payments, even if the offer was conditional on getting a checking account. An additional three in ten Millennials would take the same deal as long as the checking account wasn’t required.

| Top Factors Influencing People’s Choice of Auto Loan Provider |

Young Millennial (1988-1996) |

Older Millennial (1980-1987) |

Generation X (1964-1979) |

|---|---|---|---|

| Low interest rate | 66% | 64% | 70% |

| Online/mobile tools that help track/pay the loan |

29% | 26% | 21% |

| Features that provide transparency, flexibility and assistance paying off the loan faster |

37% | 34% | 31% |

Source: Cornerstone Advisors

“Offering borrowers choice and flexibility can increase the likelihood that they have a positive borrowing experience,” explains the Center for Financial Services Innovation (CFSI). “Allowing applicants to choose the size, length, and terms of their loan can boost take-up rates and contribute to the successful repayment of a loan.”

CFSI identified “structuring loans to support repayment” as an important guideline for lenders to follow. One practice within this guideline — allowing flexibility in setting repayment schedules that match borrowers’ income schedules — was found in only a few of the lenders that CFSI reviewed. Shevlin says this gap represents an opportunity community-based institutions can fill.

Shevlin also points out that Millennials’ borrowing needs aren’t one-shot deals.

“They are entering — or are in the middle of — life stages that require multiple and ongoing borrowing needs,” Shevlin explains. “Innovative loan products that recognize future borrowing needs can help community-based institutions gain more share.”