Digital lending is far from a new idea. Online lenders emerged in the 1990s, virtually as soon as the consumer Internet. The first eMortgage was registered in 2004. There have been numerous waves of digital innovation within the industry, both customer-facing and internal: PDF documentation, paperless underwriting workflows, and borrower portals. In fact, search engine data shows that only recently has interest in “online lending” returned to pre-financial crisis levels.

Historically, much of the focus on digital lending has revolved around automating manual processes and moving paper-based processes online. In many cases, lenders’ online experiences followed the same flow as their offline experiences, often recreating inefficient processes instead of optimizing them.

The online application replicated the same form with the same structure, and the same documents were required, just in PDF format instead of paper. In addition, several lenders made the mistake of only focusing their efforts on the front-end customer experience without linking their digitization efforts to the middle and back office.

Recently, user-centric design and design thinking have led certain lenders to begin using digital tools to change that experience – streamlining processes, providing personalized pricing up-front and integrating with data sources to reduce documentation requirements. Additionally, leading lenders are using digital tools to enable new forms of customer interactions and provide value-add services which they hadn’t previously offered to borrowers.

A New Era of Digital Lending

Digital lending is entering a new era in which its value proposition is moving beyond historical boundaries.

We see four key trends which will drive the next era of innovation in digital lending:

1. Re-imagining end-to-end workflows and processes

This trend was the leading driver of the transition to this new age of digital lending and is the furthest along in its evolution. However, significant opportunity remains for lenders to streamline and enhance their overall experience. Lenders are integrating new data sources, re-thinking the requirements to originate a loan, and reworking both their customer experience and internal workflow to deliver an efficient, frictionless lending experience.

2. Delivering a “Human Touch” Digitally

Many borrowers continue to value personal advice and having someone readily available to answer their questions. However, that does not always require a face-to-face interaction, or even a phone call.

Historically, lenders viewed the digital channel as an alternative to traditional offline channels. However, the lines between digital and traditional channels are blurring. Digital tools are increasingly adding flexibility to support both self-service and collaborative models.

Interactive co-browsing tools and video chat are clearly digital solutions, but provide many of the same benefits of human interaction. We see a rise in digital-only customers, since personal attention, guidance, and support can effectively be delivered through digital channels. While early generations of digital tools often felt sterile and robotic, more recent versions can retain the feel of a ‘trusted advisor’.

3. Cost-effectively providing personalized advice at scale

Consumers have clearly indicated their desire for relevant advice which helps them improve their financial health and make smarter financial decisions. Personal financial management tools and financial wellness programs are increasing in popularity.

A recent PwC survey of over 1,600 fully employed adults found that 46% of this population – which typically has more stable finances than other groups – still find that financial challenges are the number one source of stress in their lives. Lenders have a major opportunity to help consumers understand their financial options and choose the best solution based on their personal situation. Similar to how robo-advisors have brought the benefits of financial advisors to the mass market, digital tools such as artificial intelligence enable lenders to provide this personalized advice at scale in a cost-effective manner.

4. Providing additional value-add services

Lenders are increasingly positioning themselves as trusted advisors, providing a full suite of support to consumers aligned to their individual needs and preferences. Lenders are offering specific services tailored to the purpose of the loan.

By positioning themselves to support the underlying transactions end-to-end, not just the financing component, leading lenders can expand the scope of and strengthen their relationships with customers. While the specific types of value-add services vary by loan product and purpose, lenders can develop digital tools to provide many different forms of additional assistance to customers.

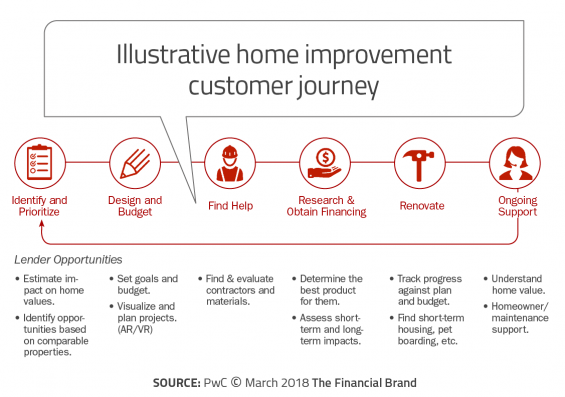

From helping auto finance customers find a car to helping homebuyers find a moving company, lenders are playing a more active role in supporting the overall purchase and ownership experience for the underlying product or service that is being financed. Even within unsecured consumer loans there are significant opportunities for lenders to provide more value to their consumers tied to the specific use of funds, such as in the home improvement example below:

Customer Acquisition in a New Era of Digital Lending

The transition from paper-based to digital is not only a matter of process – it is also a matter of channel. Lenders are increasingly turning to digital tools to find, acquire, and retain customers, not just to process applications. And as a result, many are finding it necessary to invest for the first time in digital marketing, web analytics, and other new capabilities.

As lenders begin to reach customers earlier in their financial journey, digital is having a transformative effect on the early stages of the customer acquisition funnel. A frictionless, easy to use digital lending solution can also enable Point of Sale financing, making it practical to present alternatives to credit cards for many retail transactions.

Getting a Digital Bang for Your Buck

The next generation of innovations within digital lending will not only reduce the friction associated with the online application and bring more paper-based processes online. Instead, it will be focused on how lenders can better understand and respond to customers’ personal needs, support them at every step in the lending process, and provide added value to help their customers better manage their finance and improve their lives.

The next generation of digital lending will engage consumers in new ways: (1) Digitally-augmented human support, (2) Voice interaction, (3) AI-powered virtual assistants and chatbots, (4) Wearables, and (5) Augmented and Virtual Reality.

So if simply ‘going digital’ is no longer enough, how can lenders differentiate themselves? Strategic digital lending leaders don’t just focus on ‘what’ they’ll offer – they focus on ‘why’ and ‘how’ they’ll offer it … and align innovation to users’ needs.

Your customers are ready … are you?

The above article developed with contribution from Carter Kirks, Senior Manager, PwC Consumer Finance Practice

The Guide to Digital Lending

The 63-page Guide to Digital Lending Digital Banking Report sponsored by CRIF Lending Solutions, provides insight into the progress being made by financial institutions globally in the area of digital consumer lending. Beyond a review of goals and investments, this report delves deeply into the strategies, effectiveness, challenges and gaps in delivering an exception consumer lending experience.

The 63-page Guide to Digital Lending Digital Banking Report sponsored by CRIF Lending Solutions, provides insight into the progress being made by financial institutions globally in the area of digital consumer lending. Beyond a review of goals and investments, this report delves deeply into the strategies, effectiveness, challenges and gaps in delivering an exception consumer lending experience.

The report includes the results of a survey of more than 200 financial services organizations worldwide. The report has 63 pages of analysis and 33 charts/graphs. There are also guest articles from market leaders on digital consumer lending.