Wells Fargo has announced they will be closing nearly 1,000 branches by 2020. Other banks have joined Wells Fargo in bidding goodbye to branches. Since 2012, Capital One Financial Corp. decreased its branch network by 32%. SunTrust Banks slashed its branch numbers by 22%. According to the Wall Street Journal, more than 1,700 branches turned out the lights from June 2016 through June 2017.

But it’s easy to misinterpret headlines like these. Wells Fargo is still reeling from a series of crises that have hurt the bank’s brand and its balance sheet. Nevertheless, Wells Fargo Remains committed to branches.

“Branches play an important part in serving our customers,” said Wells Fargo’s Chief Financial Officer John Shrewsberry. “We will have as many branches as our customers want, for as long as they want them.”

Closing branches is certainly one way financial institutions can cut costs and improve the bottom line. Others are consolidating redundant locations after gobbling up smaller institutions acquired through mergers.

While some pundits point to such closures as evidence that branches are dead (or dying), other banks like Chase and Bank of America opening branches. Hundreds of them. Chase has announced they will be opening as many as 400 new branches in 15 to 20 new markets in the next five years, and BofA said it would open more than 500 new branches over the next four years, including an expansion into major markets in Ohio.

Read More: The ‘Bionic Future’ of Retail Banking

Reality Check: It’s almost impossible to enter a new market without establishing a brick-and-mortar branch presence. Even in the Digital Age, opening branches remains the most effective way to grow and acquire new relationships when expanding geographic reach.

This has been Bank of America’s strategy since 2015 — entering new U.S. markets with branches. Under CEO Brian Moynihan, BofA will put branches in new markets where the bank already has a toehold serving other types of clients. For instance, in Pittsburgh, one of the markets BofA is pursuing, the bank has commercial/business and wealth-management clients from its Merrill Lynch unit, but no retail consumer presence.

At the end of 2017, Bank of America had 4,470 U.S. branches, down 109 from a year prior, leaving them with roughly 5,000 total. But during that same period, the bank opened 30 new branches across the U.S., of which 25 were in areas not previously served by retail branches. Moynihan said BofA also renovated nearly additional 300 branches in 2017.

Bank of America has closed or sold more than 1,500 branches since 2009, the vast majority of those located in less profitable rural markets. And In 2017, BofA’s adjusted earnings matched its highest annual profit ever. Branch closures have helped them save on infrastructure and employee costs, bringing down their overall expenses, which have, in turn, bolstered profits.

So are branches here to stay? Or are they on their way out?

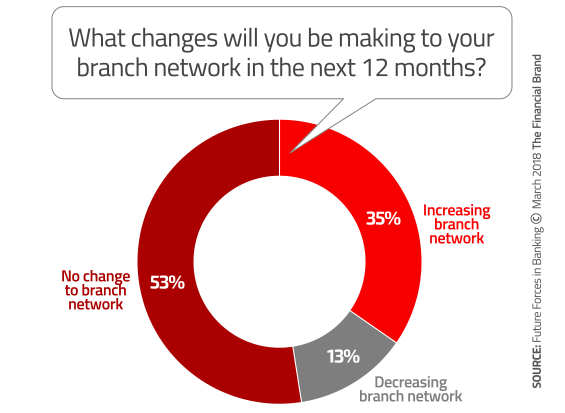

Yes. It appears the answer is both. Some branches need to be closed, others opened. Some financial institutions’ networks need to shrink, others will expand.

Bankers Unsure What ‘Digital’ Means for Branches

It’s hardly a surprise that branch networks would be on the chopping block — branches are expensive. Depending on which study you read, around one-third to one-half of a banking provider’s operating costs go to maintaining their branch network.

Robert Barba, Senior Banking & Fintech Analyst at Bankrate, says both branch openings and closures are connected back to digital banking.

“On the closure side, digital tools that give customers the ability to deposit checks directly into their checking accounts have reduced branch traffic and accelerated the need to close underperforming locations,” Barba explains. “On the expansion side, digital banking allows banks to enter new markets with a smaller number of branches.”

In a PwC survey, 59% of bankers said that they expect the importance of branch banking to diminish significantly as customers migrate to digital channels and 48% expect branch banking to change significantly by 2020. Those changes, say respondents, will have the most negative impact on regional and community banks and the least impact on global banks.

Even though bankers believe that branches need to undergo a massive transformation, only 16% of bankers say they feel “very prepared” for this shift. Banks and credit unions know that branch transformation is occurring, but they seem unsure what to do about it.

“Retail distribution is like a muscle. You have to exercise it or it will waste.”

— Marianne Lake, CFO of JPMorgan Chase

But bankers are starting to take notice and put some muscle into branch transformation. A study by CSI found that the highest priority for bankers in 2018 is customer profitability with branch transformation second on the list.

But, as CSI points out, branch transformation and customer profitability are intertwined. “If you transform your branch network to be a lower cost service delivery — with a smaller footprint, more automation, and less labor overhead, then you can increase profitability. It’s about increasing revenues as well as efficiencies,” notes the report.

Some banks are using branches as “training facilities” to teach consumers about digital, mobile and other self-service channels. For instance, FNB in South Africa, says that branches play a pivotal role in introducing customers to digital banking channels. Over the past year, the bank succeeded in getting more of its customers to adopt online and mobile banking solutions than ever before.

“The major driver has been our effort to show customers how easy, affordable and safe it is to use digital platforms, including self-service channels such as automated deposit tellers,” explained Lee-Anne van Zyl, CEO of FNB Points of Presence. “This digital journey is enabled through sustained investment in digital infrastructure which continues to be intensified through continuous innovation in branch design.”

“We have seen an important shift in the way our branch personnel interact with customers, which includes helping individual and business customers adapt to using the digital channels, thus creating more time to help customers with more complex transactions,” she added.

Read More: 10 Branches Designed To Wow The Digital Banking Consumer

39% of bankers say they plan to improve their customer experience via branch transformation in the next 12 months.

— CSI

Global consulting firm McKinsey says that even as more consumers embrace digital, branches will still play a critical role in building trust and credibility, providing financial advice, offering convenience, and easing the transition to digital channels. It estimates that having branches in just one market equates to millions of dollars in annual marketing spend.

NCR also sees branches maintaining a strategic role in financial institutions’ retail distribution models, although they say networks will evolve. NCR predicts that:

- Flagship and hub branches will decline significantly by 2019.

- Express-style branches will increase from 5% of the branch network to 50%.

- Branches will incorporate digital zones that offer increased self-service via multifunction ATMs that enable 90% of teller-based services and embedded interactive services that allow the consumer to move seamlessly from self- to assisted-service.

- Branches will offer extended opening hours, lower staff headcount and operating costs, and provide.

Utilize Multiple Branch Models and Formats

PwC agrees with NCR that the number of traditional branches will decrease by 20% by 2020. But that doesn’t mean that all your branches need to look the same. PwC says that branch formats will fall into one of three main buckets:

- Flagship branches

- Community centers

- Expanded ATMs

The role of flagship branches will be to offer information, education and advice that will drive consumer engagement, loyalty and sales. A flagship branch located in a high-trafficked area would be the perfect location to hold events and seminars (e.g., workshops for small business owners and entrepreneurs hosted by financial advisors, accompanied with food and refreshments).

Community branches will be smaller than flagship branches and their role will be community outreach and engagement through activities such as financial education.

Expanded ATM branches will be located in stores or other well-trafficked sites through partnerships with third-parties such as malls and grocery stores. The ATM branch may or may not have staff and will serve as marketing, sales, transaction and cash-handling points with smart ATMs, teller-less kiosks and touchscreens. If the ATM branch doesn’t have dedicated staff, they will likely be available via video conferencing.

Citizen’s Bank is embracing the community center model. Says Beth Johnson, Chief Marketing Officer and Head of Virtual Channels at Citizens Bank, “If customers are coming into branches less, we don’t need eight teller lines. We’ve started to think about how to evolve the network to enable colleagues to have more advice-based conversations with customers.”

Citizens is reconfiguring branches to be more inviting spaces where customers can spend longer periods of time to discuss their financial lives with their bankers.

Increase Compensation Packages for Branch Staff

As part of its announcement of 400 new branch openings, JPMorgan Chase also announced that their branch employees will be getting raises. That’s a good thing, because these employees will need more consultative than transactional skills. Moving consumers to self-service frees branch staff up for more valuable, personalized interactions with consumers.

Chase may be on to something. Financial institutions pay notoriously low salaries, with tellers earning a median of $13.11 per hour or just under $27,000 per year, according to the Bureau of Labor Statistics. Yet branch employees are the face of the bank or credit union. Sixty percent of great experiences are due to great staff, notes PwC, with 25% of consumers relying on branch employees to do research, 46% to select products and 63% to resolve their problems.

PwC says that branch staff — particularly traditional tellers — will need to undergo a massive skill transformation beyond the popular universal banker job description to become financial advisors that are truly fluent in all bank products.