Throughout the banking industry, there are remnants of the legacy paper banking world that remain embedded in online banking, creating friction and hindering the movement to a more consumer-centric digital experience. These remnants are poorly designed, reducing people’s ability to interpret financial information and make good decisions about their finances.

The first generation of online banking sites and apps basically took banks’ internal core systems and presented them on the web. So, an online banking home screen was not dissimilar to what a bank employee would have seen on their own green screen monitor – except less green. And, of course, those IT systems were in turn built off even older paper systems that dated back to the early days of banking.

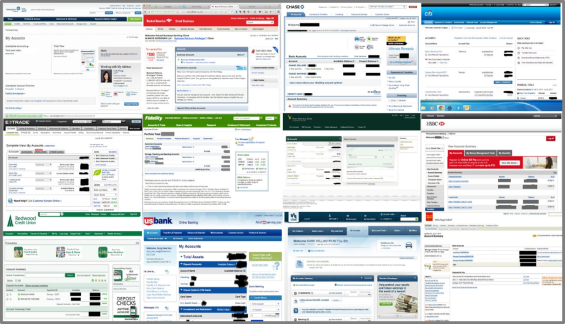

This is why the first screen of most online banking experiences look virtually the same in terms of design standards, experience and capability. Only the colors differ.

Here is a quick sampling of twelve relatively similar designs.

In the digital age, it’s time to cut the cord of history and deliver better experiences for customers. Here are three legacy ‘standards’ that need to change if we are to embrace the digital revolution in banking.

#1 Traditional Account Structure

When consumers log into most online banking sites and apps, they are typically greeted by a home page that lists out their accounts and balances in a basic table. Advanced systems will at least let the customer or member allocate ‘friendly’ names to each account.

In the days of paper and passbooks, this made sense. A customer had an ‘account’ that held their money, and maybe had a different type of account that had a different function, such as savings, and the only way to track these easily was the physical separation.

Today, this soloed allocation is senseless. Any balance is just a record in a database, so why do we need to artificially separate one portion of a person’s money from some other portion? With many consumers having 5+ accounts with an institution, this allocation goes against the way most people view their finances.

Money may be placed in different accounts, but usually there is a purpose in mind. So, why do we force customers to syphon their funds into silos created by the bank, and not a structure that supports the mental model of their life and finances?

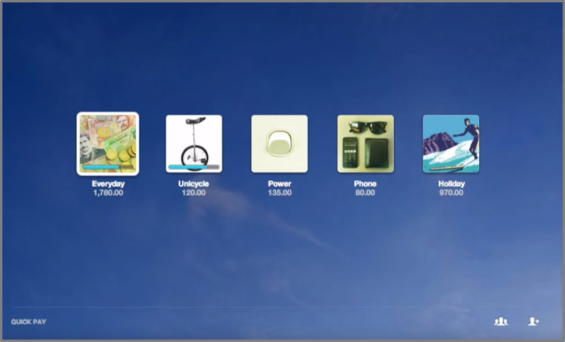

It’s time to get rid of ‘accounts’ in the classic sense, and let customers pick or create a structure that works for them, across all account types (including investments). Some institutions are experimenting with moving away from accounts in this way.

Below is a screen shot from BNZ’s (Bank of New Zealand) YouMoney service, that lets it’s customers create and manipulate ‘accounts’ on the fly, against any purpose, goals and type of money.

Watch their great video demo here: https://youtu.be/ghfV1OCUEww

There are valid regulatory and tax issues that will need to be overcome in the USA to kill off ‘the account’, but the benefits to customers is well worth the effort.

#2 Banking ‘In the Moment’

While living ‘in the moment’ is great self-help advice for us as humans, it’s less helpful with personal finances. Traditional banking tends to be very focused on a single moment in time (usually, the close of business the night before).

Again, legacy banking is evident, where it was critical to have the ledger of inflows and outflows, and a clear and accurate balance calculated at a single moment in time. For consumers, this tends to overemphasize the ‘now’, and provide less perspective on the saving and spending patterns over time.

For example, if a person gets paid tomorrow, their balance today may be significantly lower than average while their balance tomorrow will be above average. This does not help the consumer make good financial decisions.

As an alternative, we should provide the consumer a view of their finances over time, allowing them to make decisions based on their financial position compared to past (and projected) events.

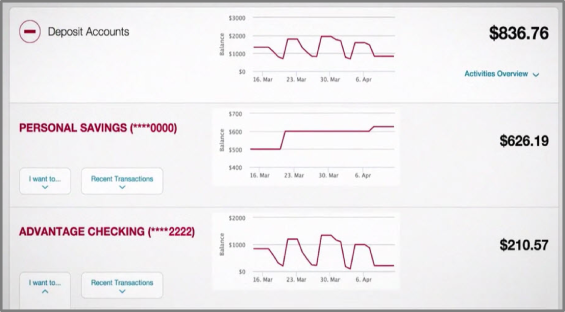

BOK Financial recently took a step in this direction by designing a new online banking experience that included simple balance charts for the previous month, prominently next to the customer’s balance. The screen shot shows the balance charts on the Bank of Oklahoma’s online banking experience. (Bank of Oklahoma is one of seven bank brands under BOK financial).

#3: Fragmented Money Movement

Why should a consumer be required to pay their landlord, their car loan, their energy bill and their share of last night’s dinner in different ways, with different design paradigms, and sometimes with completely different apps? Customers want to be able to easily pay anyone, or any entity, with a workflow starting from the same starting point, following the same steps.

This may be difficult to pull off, as there are many counter parties involved in bill pay, peer-to-peer payments and transfers. But at a minimum, banks should be burying the differences behind the scenes, delivering a similar, seamless experience for the consumer. For instance, build similar steps for paying a bill as transferring funds, but with as few additional pieces of information as possible for different types of payments.

Moving Forward

The banking industry must move away from ‘old school’ banking delivering an experience that leverages today’s digital and technological advances. For financial institutions that hold back from delivering the best digital customer experience, expect new disrupters to start nipping at your heels.

The examples provided are strong incremental improvements to the experience customers are receiving – but this is just the beginning. There is value for customers in each and every step forward, but until we start killing off some of the Jurassic Banking foundation on which today’s online banking is based, we won’t take full advantage of the digital promise for our customers.

Simon Mathews is Chief Strategy Officer at Extractable, where he leads business strategy and experience design teams that bring innovation and next-gen experiences to market for clients. He has over 20 years of experience in communications, advertising and digital agencies, working with clients including AIG, Bank of Oklahoma, BMO, First Republic and TD Bank. You can follow Simon on Twitter.

Simon Mathews is Chief Strategy Officer at Extractable, where he leads business strategy and experience design teams that bring innovation and next-gen experiences to market for clients. He has over 20 years of experience in communications, advertising and digital agencies, working with clients including AIG, Bank of Oklahoma, BMO, First Republic and TD Bank. You can follow Simon on Twitter.