Today’s consumers demand financial services to be available and delivered to them as seamlessly and ubiquitously as any transaction they complete with Amazon. And it’s not just about improving customer service … it’s about satisfying today’s hyper-connected consumer by delivering both service and sales through any channel the consumer chooses to use. The financial institution that fails to deliver sales, as well as service, through the platform of their consumers’ choice is doomed to stagnant growth.

Most consumers no longer need a branch or any other brick-and-mortar structure to consume financial services (though they may still visit their local financial institution’s branch for advice or validation about complex real estate or investment transactions, or complex servicing issues). Instead, an increasing number of consumers are transacting their financial business remotely through a variety of digital platforms: desktops, laptops, tablets, phones – even watches and glasses! And they get financial advice and information digitally also, through countless traditional financial and non-traditional websites.

Technology – The Catalyst for Change

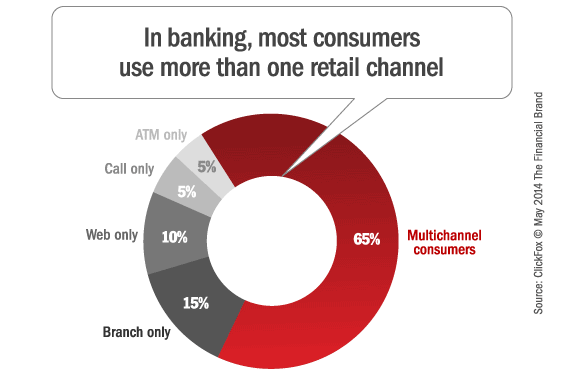

Digital technology is evolving rapidly … and consumers are adopting to new technology at record levels. The industry has experienced double- to triple-digit growth in mobile banking users over the last few years. The result is explosive growth of a hyper-connected customer base. Customers are connected to their financial institutions through multiple channels and devices. According to study by Mckinsey & Company, more than 65 percent of consumers interact with their financial institutions through multiple channels.

Unfortunately, this significant increase and shift in financial institutions’ total customer interactions has not resulted in any measurable improvement in the deepening of customer relationships or in consumer satisfaction. In fact, Accenture research suggests that about 34 percent of the total traditional banking products sold were from institutions other than the consumer’s primary bank.

The unplanned introduction of additional delivery and communication channels has led to a significant increase in operating expenses with very sub-optimal value creation. Customers want to transact with their financial institutions through multiple channels, wherever they are and whenever they want, based on their needs rather than conform to the operating model of their financial institutions.

And consumers expect their financial institutions to recognize them and acknowledge their real-time financial needs and status regardless of their choice of channel. However, many financial institutions have built incomplete operating models that improve service without significantly affecting sales … resulting in stagnant customer satisfaction on the one hand, and deteriorating sales force effectiveness and branch productivity on the other.

Buy ‘Strategic Planning Imperative: Capitalizing on Digital’s Promise‘

Building a Digital Banking Model

The operating model for financial institutions, especially regarding distribution, must change to serve digitally empowered consumers. Financial institutions must transform their current operating model in four ways to add significant value for their customers and add significant value for their brands:

- Create a high-touch, fully-integrated consumer experience supporting physical and digital sales and service. Enable consumers to use whatever physical channel or digital device they prefer to transact with you whenever and wherever they please is the key to an ‘optichannel’ experience.

- Empower consumers with digital tools and content to make a personalized product and service selection and sales fulfillment possible … thus enabling consumers to take control of their financial decisions.

- Empower frontline employees with cross-channel, real-time customer insight and intelligence to support both sales and service needs … dramatically increasing employees’ productivity.

- Garner commitment and mandate from upper management and boards in support of the above changes, both financially and emotionally, which must extend throughout the entire organization.

Integrating the Consumer Experience

Building a digital-first consumer delivery model that establishes an intuitive sales and service experience map for all core products and services (including well-defined service-level agreements and performance metrics) is the foundation for tomorrow’s Digital Bank. The process of mapping out the customer experience will capture the required variations in sales and service delivery by customer segments (for example, the mortgage purchase experience varies significantly based on whether a customer is a first-time home buyer or the customer is refinancing).

Once customers’ qualitative and quantitative intra- and cross-channel experiences are mapped by segments and needs and validated, then begins the development of a detailed integration and alignment plan that addresses:

- Cross-channel technology platforms

- Sales and service processes

- Employee goal setting and incentives

- Training and education

- Real-time MIS and advanced analytics

Empowering Consumers

According to an Accenture study, sales of mortgage through multi-channel digital platforms increased by 75 percent, while single-channel branch sales dropped by 16 percent. Consumers, by nature, like to be in control of their financial transactions. Financial institutions can reinforce consumers’ feeling of control by empowering them through ubiquitous access to multiple channels and access to an effective set of tools, calculators and personalized content. Depending on the complexity and nature of the transaction, sales agents at restructured branches or call centers can assist in the educating, advising and supporting of consumers in real time enabling better financial decisions.

Empowering Frontline Employees

A logical questions could be, “Why should we empower frontline employees when customers can transact across digital channels in real time”? First of all, empowering frontline employees with digital tools will significantly affect productivity. When frontline employees are empowered with consumer insight and intelligence through digital devices in a physical location, they can be incredibly effective and productive in serving customers who often start, stop, reactivate, and complete sales or service transactions using multiple channels.

Digital tools and access to insight also allows customer-facing branch employees, regardless of their physical location, a real-time, ubiquitous access to customers’ sales or service journey across all channels, helping employees to educate, advice and support customers to a successful, complete transaction.

Top Management Commitment and Mandate

Transforming the current operating model requires an unequivocal commitment and mandate from key business leaders throughout the organization. There are two components to this transformation: cultural and operational. It requires a complete change in employees’ mindset and the way employees interact with customers, and the way frontline employees interact with other frontline employees across all channels. It also requires an adjustment in how frontline employees interact with backend employees to support the new operating environment.

This is a journey and not a single event. There will be significant ups and downs as frontline and backline employees learn how to serve customers through multiple channels in real time. Organizational agility, adaptability, and speed to change are prerequisite for long-term success.

The Payoff

Changing to an integrated, ‘optichannel™’ sales and service model requires significant organizational, operational, and financial investment. But the ROI can also be significant. The following data was collected from financial institutions with an aggregate value of $7 billion. These institutions switched to an integrated ‘optichannel’ channel model over roughly a nine-month period with these results:

- More than a 200% increase in multi-channel digital sales

- 17% of customers added a second product to their shopping carts

- More than 18% increase in sales through real time smart lead management

- A 20% reduction in call volume to call centers.

Clearly, now is the time to change your operating model. Consumers are changing their behavior, aggressively adapting digital technology and making greater use of multiple channels, which requires a new, integrated way to interact with customers and employees. Evolving the current branch-focused operating model into a new ‘optichannel’ model will reinvigorate the way financial institutions and their branches serve consumers and grow business.

Meheriar Hasan is the CEO of Terafina and a seasoned financial services executive with more than 30 years of experience building direct/digital distribution channels generating significant new sources of profits at organizations ranging from retail banks, insurance, consumer finance to technology companies. Hasan is a leading thinker in the area of digital consumer channels, a frequent keynote speaker, lecturer and author on eMarketing, eCRM and digital technology, and an often-quoted expert in articles and on network news. You can also follow Terafina on LinkedIn by clicking here.

Meheriar Hasan is the CEO of Terafina and a seasoned financial services executive with more than 30 years of experience building direct/digital distribution channels generating significant new sources of profits at organizations ranging from retail banks, insurance, consumer finance to technology companies. Hasan is a leading thinker in the area of digital consumer channels, a frequent keynote speaker, lecturer and author on eMarketing, eCRM and digital technology, and an often-quoted expert in articles and on network news. You can also follow Terafina on LinkedIn by clicking here.