Just a few years ago, mobile banking apps were a key differentiator for banks and credit unions. Nowadays, mobile banking apps are table stakes. Over 90% of the institutions listed on FindABetterBank have mobile banking apps, and 44% also offer mobile remote deposit capture.

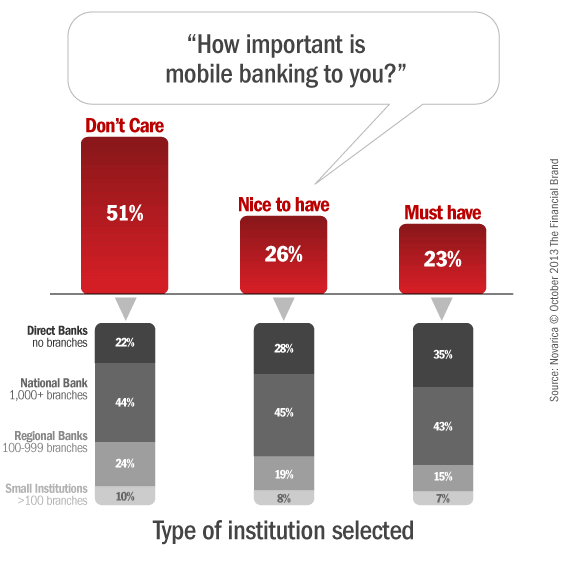

As more consumers adopt mobile banking, more will insist that any institution they switch to also provide this service. In Q1 2011, under 12% of shoppers on FindABetterBank indicated they “must have” mobile banking. Today, that number is 23%.

Direct banks like Ally Bank and Capital One 360 are winning the battle for these mobile-centric shoppers. In Q3 2013, direct banks were 38% more likely to be selected when a shopper indicated mobile banking was a must-have feature than when a shopper indicated they “don’t care” about mobile banking.

In fact, over 43% of “must-have” mobile shoppers cited low fees as the reason they chose a direct bank – the top reason among these shoppers. These mobile banking users aren’t as interested in paying for convenient branch locations. Shoppers who “don’t care” about mobile banking were 28% more likely to choose an institution based on convenient branch locations than “must-have” mobile banking shoppers.

Network banks and credit unions must address this disparity to maintain their market and deposit share over direct banks. Why? Direct banks’ lower costs and technology-oriented services will appeal to a larger share of consumers, as they begin adopting mobile apps for their everyday banking needs.

To date, direct banks own a small share of deposits overall. But technology adoption and a rising rate environment may soon change that: Fewer consumers will choose institutions based on the convenience of their branch locations; direct banks’ higher deposit rates will appeal to many consumers; more consumers will consider direct banks due to low fees. Suddenly, direct banks will own more than a blip of the overall deposit share. How will network banks and credit unions respond?