Financial marketers often fixate on evaluating people according to their generation, but that’s only a single dimension and will have you chasing Millennials and Gen Z as if it were a reflex action. The U.S had about 126 million households in 2020 and many of those were multigenerational. While individuals clearly make their own purchasing and banking decisions, major financial decisions are made at the household level, such as a couple deciding where they will bank. In fact, joint accounts are common in households as they can reduce overall fees and simplify daily life.

This is why looking at U.S. households’ banking behaviors by the generation of the household head proves critical. A useful filter is the “age of household head by household income” approach, as it speaks to the shifts in financial services needs as people move through different life stages. Census and other government data is very useful for evaluating markets using this lens.

A Surprise in the Data:

For all today’s focus on youth, households led by Baby Boomers formed the largest segment at 35% of all households in 2020. This was followed by Gen X (26%) and Millennials (24%). Far fewer households are led by Gen Z-led households, as many of those people still live with Gen X or Boomer parents.

Looking at Head of Households’ Income Levels

Digging into household income yields some interesting nuggets:

- Gen X-led households have the highest median household income of the segments at $82,000, followed by Millennials at $71,000.

- Boomer-led households’ median household income is only $62,000. That figure apparently is pulled lower because half of the segment is over the typical retirement age of 65.

- Gen Z-led households have median household incomes comparable to Silent Generation households — near $35,000.

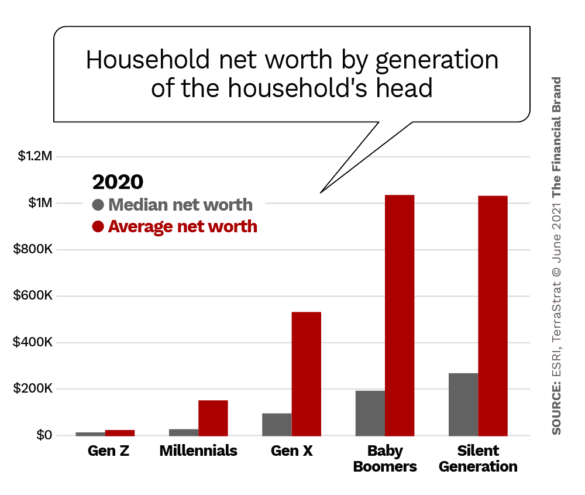

Age also plays a key role in each household’s net worth:

- Gen Z: Median net worth for Gen Z-led households is low, at about $10,000. With an average net worth of nearly $26,000, we can safely assume that many Gen Z households have net worth closer to zero. These young households have limited assets and are accumulating debt at an increasing pace.

- Millennial-led households have about three times the median net worth of Gen Z households at $30,000.

- Gen X households median income comes about three times the Millennials’ median at $94,000. Both segments likely have greater awareness of their net worth as they begin thinking about retirement down the road.

- Boomer-led households’ median household net worth is about double that of Gen X at $194,000, with an average net worth over $1 million.

- Silent generation households have a median net worth of nearly $270,000 and an average just over $1 million as well.

Both of these oldest segments are either in or nearing retirement, and drawing down on retirement savings to supplement any social security or pension benefits.

Boomers and the Silents hold the bulk of the country’s consumer net worth. What does this imply?

Many banks and credit unions have focused their marketing efforts on attracting the younger segments, especially Millennials and Gen Z, as do neobanks. The opportunity to connect with these digital generations, making a lower cost-to-serve population, represents a good long-term business model. The challenge is that these two youngest segments control only 6% of total consumer net worth.

You’re Not Done with Boomers Yet!

In the short term — the next 10-20 years — firms must continue to establish and maintain relationships with Boomer households. They comprise more than half of consumer net worth.

Read More:

- Is Everything Bankers Think They Know About Millennials & Gen Z Wrong?

- Verizon Infiltrates Banking with Neobank-Like Strategy

Channel Usage May Not Differ as Drastically as Some Think

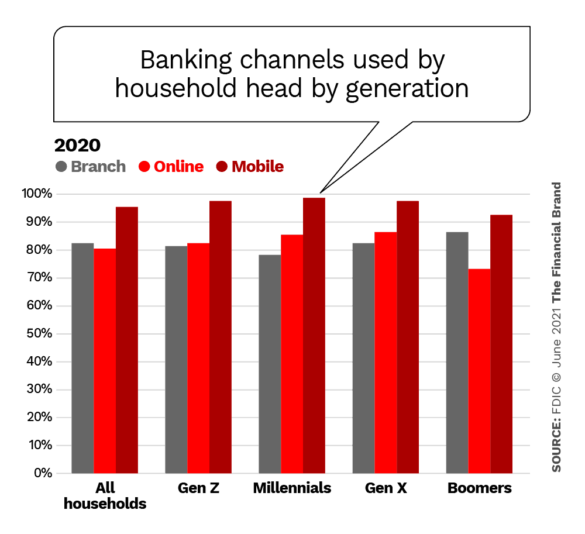

Every two years FDIC conducts a large-scale study of consumer banking behavior, with 2019 being the latest available data. The collected data can be disaggregated in several ways. Here is how it looks by generational households.

In my experience households “collect” channels. They use the one that is most convenient for each individual transaction category. FDIC’s study was confined to branch, online and mobile channels. The data indicates that across all segments most households use all channels over the course of a year. The three youngest generations have similar usage patterns, while Boomers, as expected, are slightly less likely to use digital channels. [A side note: The pandemic drove significant shifts to digital channel usage during branch shutdowns. The 2021 study will be interesting.]

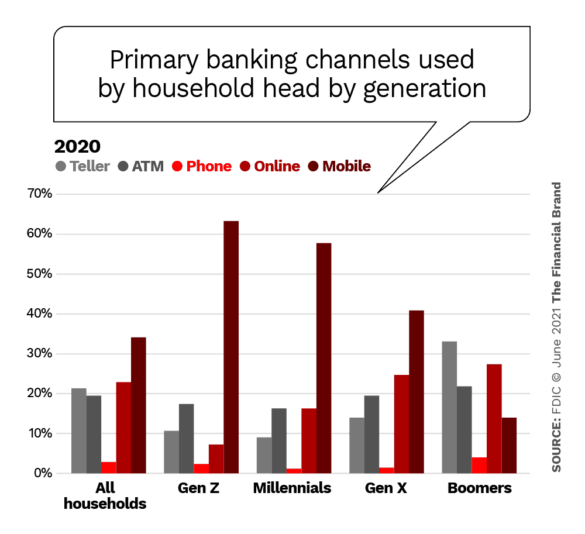

The survey also looked at which channel consumers consider their “primary” channel for banking. This is where we begin to see some differences between the segments. The younger segments, as expected, are more likely to consider the mobile channel as their primary channel for banking.

The mobile channel is considered the primary channel for all segments except for Baby Boomers. Mobile dominance declines with age. For the Baby Boomer segment, the branch is still seen as the primary channel for interactions.

Nobody is All One Thing:

Most notable in this research is that all segments use all channels. The difference is just a matter of degrees.

More than half of Boomer-led households view the physical channels (branch and ATM) as their primary channel.

Most people use all channels over the course of a year, across all segments. In my experience, as new channels roll out, consumers adopt the new channel over time and add each new channel into the mix of their interactions with their bank or credit union.

Much of the industry is absorbed by digital transformation. I worry whenever industry leadership chases the next bright shiny thing.

Read More: Gen Z Craves Good Tech From Banks+Credit Unions, Not Neobanks

What Do Consumers Want from Financial Institutions?

When a recent BAI study of the generations asked respondents what they wanted from banks or credit unions, it found differences between the groups.

Gen Z, the youngest segment, is new to the world of consumer finances. They are the most technologically knowledgeable, having grown up not knowing a world without computers or mobile phones. However, the 2020 TIAA Institute-GFLEC Personal Finance Index measures financial literacy and found that this generation scored significantly lower than the older segments. They seek education, wanting to learn how the system works. Meanwhile, today, their needs are straightforward. They need checking, savings (perhaps) and a credit card. Many are living paycheck to paycheck.

Millennials know the ropes and want banking to be made simpler. They seek transactional convenience. Busy at work or raising children, their days are full and going to a branch takes time. Their financial needs are more complicated. Home purchases are on their minds, if they haven’t already taken that step, yet many are still carrying student debt. Retirement seems light-years away. Millennials came of age with the internet and are comfortable with informal communications through digital channels.

Gen X is beginning to worry. They want advice from a financial services provider. They are in their peak earning years yet wonder where all the money goes. They are behind in saving for retirement according to many articles in recent years. Carrying a mortgage on top of some lingering student debt and helping their children pay for college creates barriers to saving more. While Boomers are optimistic that hard work will lead to personal benefits, Gen X is more interested in work-life balance. If any firm isn’t meeting their needs, they are more willing to move on.

Boomers seek security. Boomers feel they have done their time and built a retirement nest egg, but wonder “Is it enough?” Many worry they won’t be able to retire when the time comes. They have lived through many recessions, big and small, and have seen the impact on their savings and investments.

Generations Are Changeable Things, Not Frozen in Time

Households’ financial needs change over time. You can see it today by comparing the generational data. As each segment will grow older over the next ten years, with most Boomers retired, being replaced by Gen X in their peak earning years. Millennials will begin worrying about retirement for sure, and Gen Z will start dealing with home ownership and growing families.

All of this shifting demand driven by life stage changes will likely result in greater overall loan demand but reduced overall savings rates. The fight to capture low-cost deposits will be intense, in spite of the glut of money financial institutions currently have.

Rethink Branches, Don’t Close Them All:

In a J.D. Power study, Millennials and Gen Z were not only more likely to seek out advice, but were also more likely to use the advice they received, compared to older segments. Evolving today’s branches into tomorrow’s “advisory centers” makes sense. These consumers face increasing complexity.

- Gen Z: At 25 years old or less today, they have had limited exposure to how the system works and likely use only the most basic of products (checking, savings and possibly credit cards). But 10 years later, they will be immersed in more complex financial needs. The need for more complex financial products. Yet, they are the most technologically savvy of the segments and will handle routine transactions digitally.

- Millennials were all about transactional convenience 10 years ago, but now their worlds are more complex. They have the highest incomes of the segments with most in the family-formation mode. Retirement now seems way too close. Even though they may have high earnings, the anxiety about saving for retirement while juggling student debt and family education savings is intensifying. They need advice but aren’t used to going into the branch.

- Gen X is in their peak earnings years. Loan demand will still be strong and as will savings building with retirement only a few years out. Ten years ago, they sought advice. Did they get it?

- Soon Boomers will all be over 65 years old with the majority retired and out of the workforce. They sought security in 2020. If another financial crisis happens in the next ten years, how will they react? Will savings shift to annuities or low-risk investments? This group’s demand for loans will continue to be low and they will be still be net “de-savers” drawing down on their lifelong savings to supplement retirement pensions and social security.

Don’t Buy into Single-Dimensional Thinking About Generations

The interest in “generational” marketing to attract the younger Gen Z and Millennial households, who are digitally-savvy, has grown in prominence in recent years as neobanks have entered the marketplace. These firms aspire to create a large base of digital-only customers long-term.

While attracted to the transactional convenience, these consumers will prove the least satisfied with digital providers who only provide transactions. They want to be informed and educated. As they grow older and have more complex financial needs, they will want trusted advice.

There’s little discussion today about Baby Boomers and Gen X households, even though they control over three-quarters of consumer net worth. Whether it’s because financial firms believe Boomers and Gen Xers will not change their banking relationship, or that they still want expensive branches is unknown. What is known is that these segments form the greatest opportunity for profitable relationships.

The industry’s overall approach to driving costs down in all channels must be rethought. Providing transactional convenience is easy, as shown by the proliferation of neo-banks today. These new firms are disrupting the industry by carving off a small piece of what more traditional banks and credit unions offer. Building relationships with customers is harder and is done through human interactions, something neobanks can’t do today and will find costly to provide in the future.