New technologies and rapidly evolving consumer demands make change a constant in retail banking. Responding effectively to new trends requires constant vigilance and a comprehensive approach, particularly with the branch networks operated by banks and credit unions, where major change is underway.

Achieving and maintaining a competitive edge in branch networks starts with data-rich consumer profiles and advanced location analytics. This information guides critical real estate decisions and transactions that facilitate expansions, consolidations, and right-sizing.

A market-driven approach to branch optimization also employs customer experience research to ensure pleasing building designs, amenities, aesthetics, technologies, and service levels, geared to current and prospective customers. This helps preserve valuable investment capital, increases efficiencies, and maximizes profits.

And once location and design decisions are made, integrated project delivery (IPD) can make projects happen without delays or change orders.

Let’s take a more detailed look at the three critical steps of the branch optimization and design process.

Step 1: Location Risks & Rewards

How many branch locations, what kind, where and why? These are questions banks and credit unions need to ask regularly about their retail branch network.

The Covid-19 pandemic makes answering these questions urgent as the virus has changed consumer attitudes and behavior in ways not yet evident:

- Will your branches be as productive going forward? Are they sized right and configured well for future service delivery?

- Are consolidations in order? If so, what current metrics and leading indicators are you using to spot locations that may warrant closure?

- What markets may be ripe for expansion given the state of your competition, as well as new commuting patterns and consumer work habits?

Obtaining the answers comes from using a combination of big data market analytics and site-specific real estate savvy.

Optimal branch locations, sizes and functions can be effectively modeled with data to achieve maximum return on investment, boost efficiency and reduce costs.

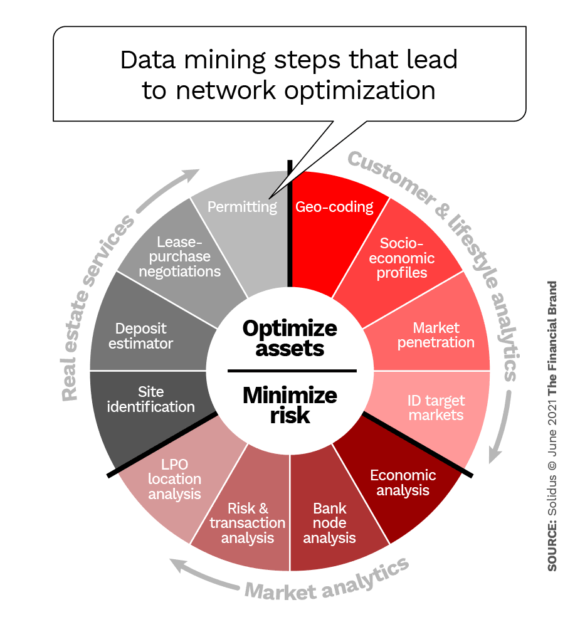

A comprehensive branch network optimization process includes a series of data-mining steps:

- Geo-coding: Drive-time mapping of current (and prospective) consumers who reside or work proximate to your current and potential branch locations.

- Market analytics: A traditional profile of an area’s population demographics, housing data, and the nature and volume of banking business conducted.

- Socioeconomic analysis: A deep-dive that identifies customer lifestyles, buying, saving and investment habits.

- Market penetration: Gauges your financial institution’s upside potential in current and prospective markets, based on market and consumer analytics.

- New target markets: Identifies where concentrations of your likely consumers reside and work — and potentially favorable clusters of enough business consumers to enable location of profitable Loan Production Offices (LPOs).

- Competitive “node analysis”: Assesses competition at each banking location in a target market — Who are they? How long have they been there? Is their share of deposits increasing or decreasing?

Be sure not to underestimate the critical role of transactional real estate. Finding the best locations in target markets is of utmost importance – and that ideal site or building may not be posted as available on commercial real estate platforms: In fact, real-life experience with local real estate markets shows that unlisted locations are secured more than half the time.

Local Knowledge Is Key:

Branch revenues can be profoundly affected by many local factors, such as morning and evening rush hour commuting patterns, traffic signals, certain corners of a given intersection, allowed signage and sight lines and future community development plans.

Accurately estimating deposits at a specific address is critical. With hundreds of thousands or millions of investment dollars tied up in a branch location, this is no small concern.

Read More: Rethinking Branch Networks Without Killing Growth

Step 2: Customer-Centric Branch Design

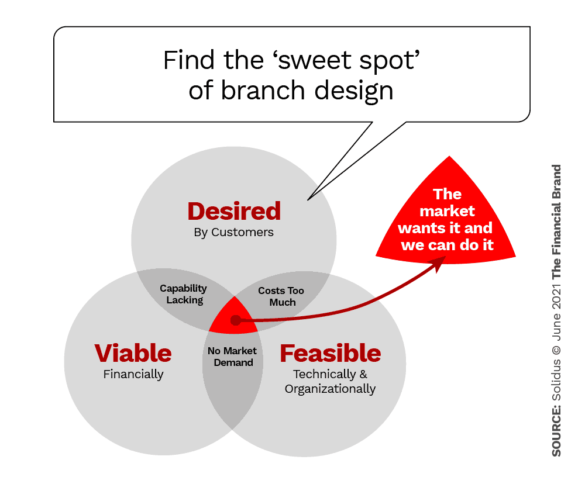

When it comes to how your current branches look, feel and operate, what appeals most to your consumers now and going forward? What investments will pay for themselves? How can you be sure?

Customer experience research allows you to model and predict consumer behaviors. This, in turn, allows you to introduce retail designs that will succeed.

Potential Gain:

A McKinsey analysis found that by implementing customer-centric branch design, a $500 million branch network would likely see an extra $500,000 in revenue each year.

A customer-centric focus also enables confident branch design and service-level decisions that will enhance customer experience, engage employees, improve operations, minimize risks and assure ongoing success through continuous learning.

As important, it can stop you from jumping at solutions that may seem attractive, but may lack enough market demand, cost too much to implement, or be beyond your organization’s ability to deliver. Instead, you’ll end up with a strategic roadmap that will provide a blueprint for future branch renovations and expansions.

Though we are all different as individuals, groups of consumers have preferences and tend to seek retail experiences that are familiar and reassuring. These preferences fall into four primary categories:

- Aesthetics – lighting, color choices (warm or cool), surface coverings, flooring, signage and retail communications, ambience

- Technologies – online and drive-through options, smart phone apps, financial modeling tools, digital signage

- Amenities – treats and eats, furniture styles (formal vs. casual), conference space

- Service Levels – tellers vs. universal bankers, traditional vs. modern, service hours, product mix, coin machines.

Once analyzed, customer experience research enables prediction of buyer behaviors with a high degree of accuracy. What’s more, once you know what counts — that is, what you must include as part of your design and service mix to please your consumers and ensure a competitive product — you can make smart decisions when it comes to some of your largest cost drivers: square footage, curb appeal, interior finishes, and staffing levels and consumer flow.

Step 3: Making the Change Without Breaking the Bank

Even with a customer-centric design established, numerous construction-related challenges — especially change orders — can derail the best plans. Unexpected charges and delays are the stuff of nightmares, busting budgets, blowing up deadlines and destroying relationships between owners, construction managers, architects and subcontractors.

Thankfully, there is a proven way to avoid the change-order trap. Integrated project delivery (IPD) is a best-practice approach to construction design and cost estimating featured in leading technical journals, taught at prominent universities, and endorsed by the American Institute of Architects. IPD assures seamless coordination of architectural design and engineering; open-book pricing, bidding and vetting; joint scheduling of construction trades; and a creative branding process. Silos are replaced by teamwork. Shared goals serve to identify and head off costly problems relative to design, specifications, construction processes, materials and timelines.

To succeed, IPD requires overt teamwork and trust among those responsible for every phase of project execution from design, estimating, bidding, and budgeting to scheduling, permitting, construction and branding.

Read More: Banks May Still Need Larger Branch Networks to Find Sales Success

Step three leads into a new cycle, which is continuous improvement, or, more specifically, a workplace culture that actively promotes and celebrates incremental, customer-centric steps that improve your processes, products, and services. Taking even the smallest steps over time will make a big difference in your branch network’s success, affecting everything from employee retention to innovation and profitability.

A successful continuous-improvement process must include these steps:

- Define what needs improvement. Most every service, process or product can be better — even the new website you launched last quarter could already benefit from revisions! Focus on what matters most, taking full advantage of the valuable perspectives of your front-line employees and ongoing consumer feedback.

- Analyze and diagram component steps. What are the sources of delays, errors, or people’s complaints? Start with those that cost you the most, as measured by financial losses, wasted time and resources, or aggravated customers.

- Redesign. Start with the end in mind. Diagram new ways of doing business that promise to eliminate or mitigate problem areas.

- Implement and monitor. Institute the new process, product, or service, but not before you’ve established metrics to measure success. For example, plan for “before and after” surveys of employees and consumers. Find industry benchmarks against which you can assess your company’s performance.

Make daily discovery the norm: Learn from experience. Continuous improvement relies upon empowering employees to pursue excellence, to propose and make change. Just be ready to enthusiastically share the rewards and excitement of a genuinely engaged workforce!