The drumbeat of warnings about the need for digital transformation may seem overstated at times. Heavy on the foreboding and predictions, light on actual results.

But research and analysis from two prominent consulting firms confirms that the transformation trend not only has long legs, but brings meaningful differences. In addition, banking leaders are realizing increasingly that change is occurring far more rapidly and broadly than many had expected only a year or two ago. Contrary to some current beliefs, this shift began before Covid 19 was an issue.

Some banks and credit unions, in fact, have already advanced far down the road to becoming digital organizations and have begun reaping the rewards — both financially and in terms of competitive advantage.

There’s No Going Back:

Even if Congress shuts the door on nonbank inroads into banking (unlikely), consumers won’t suddenly dial back their expectations, nor will fintechs just disappear.

In a new report, Accenture analysts highlight the performance improvements that digital transformation brings. The report focuses on operational efficiency — what the consulting firm calls the “operational maturity” — of financial institutions, measured by eight factors.

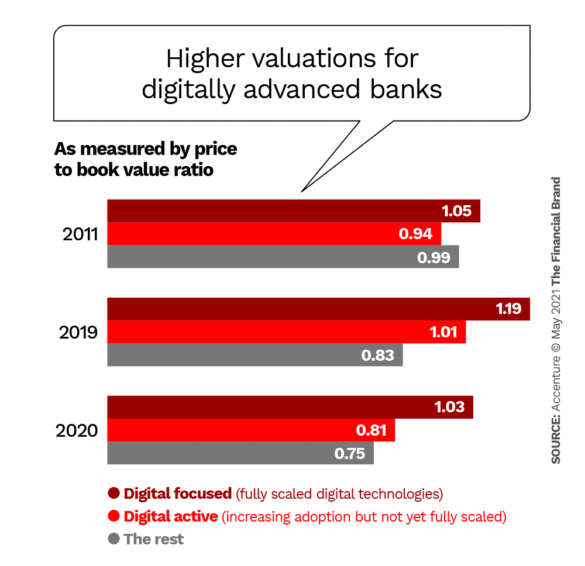

Digital Progress Impacts Valuations

Using financial data from S&P Capital, Accenture demonstrates that digitally focused financial institutions have already benefited significantly in terms of financial results. Digital leaders’ price-to-book value (P/BV) ratios on average were 18% higher than less-digitized peers in 2019, and 27% higher in 2020.

“Digitally focused” refers to financial institutions that have fully scaled digital technologies (e.g. analytics, artificial intelligence, automation and data systems) across the enterprise, according to Manish Sharma, Group Chief Executive of Accenture Operations. “Digitally-active” banks are increasing adoption but are not yet scaling across enterprise functions, Sharma tells The Financial Brand.

The higher P/BV ratios shown above are a function of cost improvement — operational efficiency — plus revenue improvement, the report states. Digitally focused institutions have increased operating income per dollar of assets from 1.22% in 2011 to 1.47% in 2019. That compares with figures of 1.23% and 1.27% for digitally active institutions. Banks and credit unions that are not digitally active saw operating profits as a percent of assets declineduring the same period (1.11% to 1.06%).

Read More: Digital Transformation Is About New Business Models, Not New Tech

Seven Operational Shortfalls

Financial institutions have been automating since before the invention of the digital computer and have, at various times, been technology leaders. But in the last decade or so, the pace and nature of change enabled by modern digital technology has challenged financial institutions to adapt.

Accenture’s study found that while operating model maturity is advancing in banking, it is doing so more slowly among financial institutions than in other industries studied.

Operational maturity is crucial because it is a measure of a financial institution’s “future readiness,” the firm states. That readiness reflects the ability to scale eight characteristics: 1. Data, 2. Analytics, 3. Leading functional practices, 4. Business-technology collaboration, 5. Agile workforce, 6. Advanced automation, 7. Stakeholder experience and 8. Artificial intelligence.

Of these eight, financial institutions lead other industries in only one: widespread availability of quality data.

The three areas in which banking has the biggest operational shortfall compared with other industries:

- Use of advanced automation tools, such as robotic process automation (RPA) that perform repetitive rule-based tasks.

- Workforce agility, encompassing a collaborative approach not only between teams but between humans and machines.

- Business-technology collaboration, the degree to which business and IT units operate in an integrated fashion using a joint governance model.

In regard to banking’s wealth of data, Accenture points out the challenge lies in extracting the full value of the data, such as the ability to provide real-time insights to consumers and businesses. Better use of analytics, AI and automation would make this possible, the report states.

Read More:

- 7 Essentials of Digital Banking Transformation Success

- Banks Can’t Be Agile With Outdated Tech and a Legacy Core

Improvement, But ‘Silos’ Are Still a Problem for Many

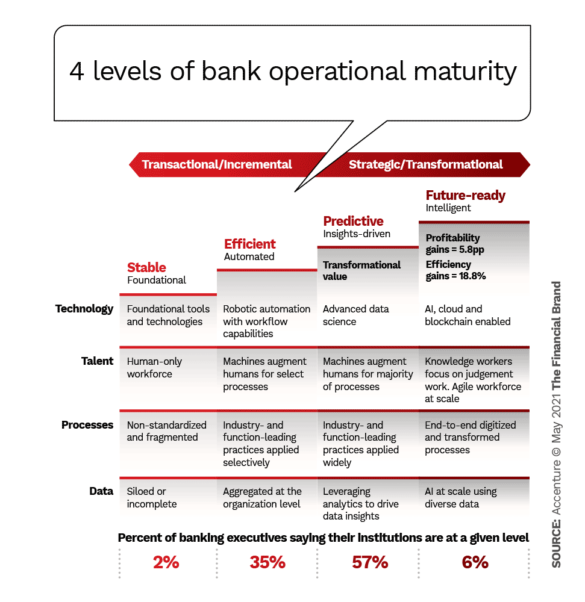

Four distinct operational maturity stages were outlined by Accenture. These are shown below, along with how banking executives rank their institutions. As the percentages indicate, notwithstanding the shortfalls outlined above, the industry has made progress in moving from the earlier stages of operational maturity to “future ready.”

The percentages above would seem to suggest that, at least among the 100 financial institutions represented in the survey, operational maturity has progressed further than the industry as a whole. Asked if he thought the characterizations were optimistic, Manish Sharma replied that the optimism corresponds with the adoption over the past three years of analytics and automation, and the hiring of data science specialists.

Although few banking leaders polled appeared to think their institutions suffered from siloed data, as shown in the graphic above, other observers believe many financial institutions still do.

Accenture observes that “Data has long been at the heart of decision-making for banks, but often data sets are fragmented across multiple silos.” More than seven in ten (71%) executives say they designed their operating models based on data rather than on executive experience or intuition, Sharma points out. Nevertheless, he states that rigid organizational structures still trap data between departments within a banking organization, which leads to pain points for consumers such as delays in response due to a lack of a centralized database.

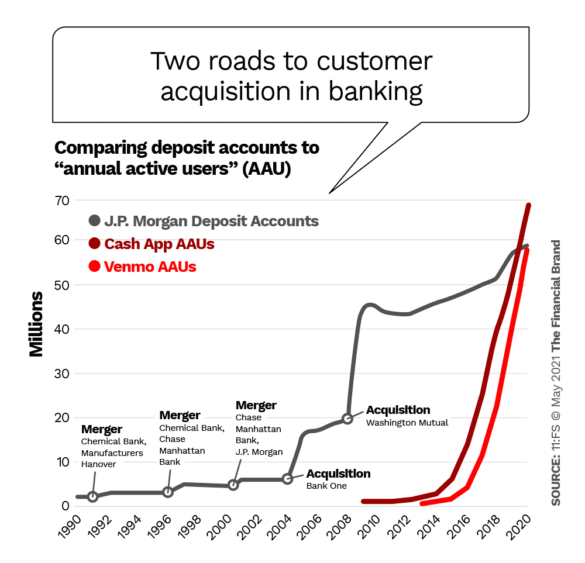

One of the notable capabilities of fintech companies is the ability to zero in on such customer pain points and devise a solution in a far more rapid manner than most traditional institutions can match (so far). This distinction can be seen graphically in the comparison below, prepared by digital consultancy 11:FS, showing how two fintechs — Square (which offers Cash App) and PayPal (which owns Venmo) — have been able to build a customer base equaling or exceeding what JPMorgan Chase has been able to do in a much shorter timeframe.

Read More: Lessons from a Bank Chief Transformation Officer

Practices That Hinder Banks’ Digital Progress

Financial institutions’ fixed cost structures and significant investment in legacy systems complicate the job of becoming operationally “future ready,” according to Accenture.

As a result, banks and credit unions typically follow an incremental approach to improving operations. “With limited funds to invest in operations, they simply plug the biggest hole first and those holes are often defined by regulatory and compliance priorities rather than enhancing competitiveness,” the report states.

“Where business executives have their own IT teams in order to get things done. … It creates all of these different islands within an organization, which makes it impossible for the entire company to work in a cohesive manner.”

— Bank Executive quoted by Accenture

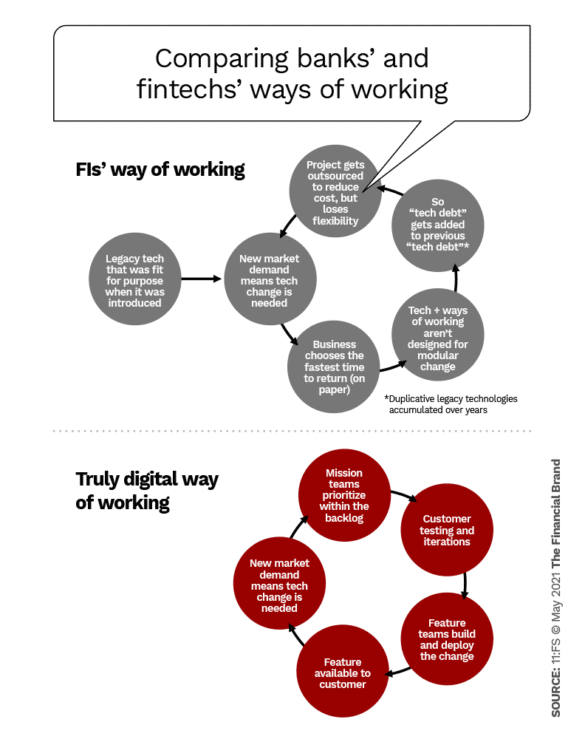

In its report, “Rebuilding Financial Service from the Inside,” 11:FS identifies three primary drags on achieving digital-powered growth:

- Short-term funding model: Typically a 12-month cycle weighted toward in-year return. Funding is allocated by business or product line.

- Existing ways of working: Decisions by large committees, with centralized strategy teams created to deal with complexity across silos.

- Compounded “technology debt”: The state of technology within a financial institution mirrors the organizational design, leading to heavy duplication and limited re-use. Use of modern technology is limited.

Truly digital businesses, such as most fintechs and even the big techs, have much faster ways of working, 11:FS points out.

Read More: How to Build a Data Culture that Supports Digital Banking Transformation

What Financial Institutions Can Do to Improve

Accenture urges financial institutions to “think big” instead of always making incremental improvements. Specific applications where that approach applies, according to Manish Sharma, include adopting cloud integration, remote process automation and implementing AI at scale.

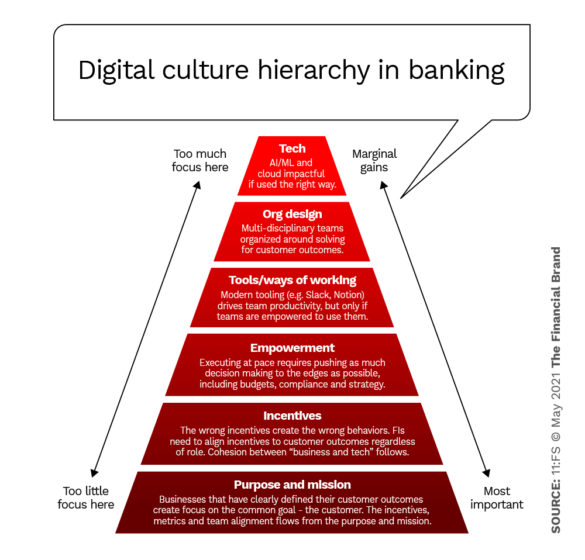

In its report, 11:FS provides a pyramid-shaped diagram encompassing many of the recommendations it makes for banks and credit unions to transform digitally “from the inside.”

11:FS recommends specifically that financial institutions must move away from their current unwieldy assortment of systems, technology and processes and adopt use of small, modular components that can easily be used to build any product.

In addition, a focus on modules instead of products will help break down silos. “Organizing horizontally leads to more knowledge sharing and dynamic allocation of people as the pressures on the business change,” the 11:FS report states. “Ops teams are more empowered to make decisions quickly.”

Bonus Point:

There are regulatory benefits from more modern operations. One example: Risk is reduced when information is shared in real time between teams.

Another recommendation from 11:FS is that financial institutions should consider changing from large, all-inclusive technology providers to using an assortment of more modern, specialist providers, to gain more flexibility.

Accenture refers to that process as developing ecosystem relationships, and stresses that such partnerships will help financial institutions leapfrog operational maturity levels. Such ecosystems force financial institutions to decide engage in “make or buy” decisions much more often. However, this doesn’t mean banks or credit unions can’t maintain their core operational systems and processes, Sharma states. They can instead build upon them.