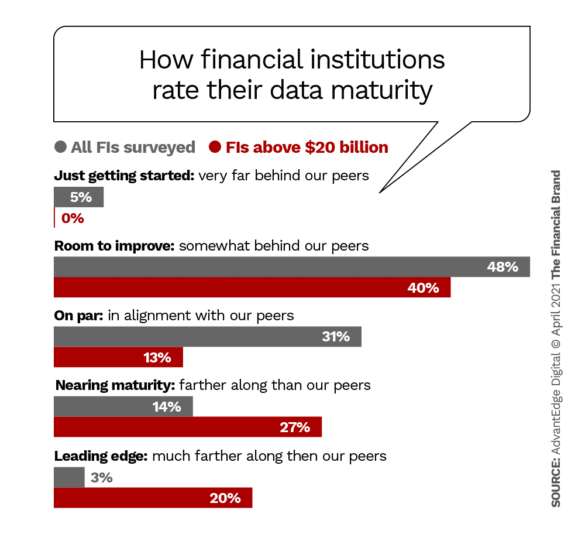

When it comes to digital transformation, a nearly universal truth seems to be emerging: Many banks and credit unions feel they are behind where they need to be.

In fact, in a recent survey of 141 financial institution executives, 53% reported feeling at least somewhat behind — if not very far behind — their peers. That response includes the perspective of executives representing institutions with assets above $20 billion. Among those at the largest institutions responding to the survey, 40% said they felt behind.

Who can blame them? The sheer pace of technology advancement is like nothing the world has seen before. Exponential advances in everything from data analytics and artificial intelligence to 5G, cloud computing and soon quantum processing are democratizing once out-of-reach technologies, making it difficult to keep up.

Big Tech Lending Experiences Ramping Up the Pressure

Lending departments, especially, are feeling the competitive pressure to keep up. Digital-native, “lendtech” providers are entering the auto, real estate and consumer lending marketplaces, ramping up borrower expectations for digital experiences on par with those delivered by big tech.

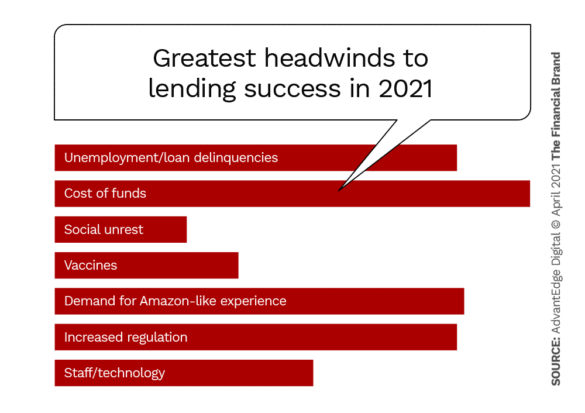

“Meeting demand for Amazon-like experiences” was the second most popular answer given by our survey respondents when asked to name the greatest headwinds impacting their lending success.

Loan Demand Is Strong – If You Can Win the Race to Funding

The unprecedented events of 2020 flooded credit unions and banks with cash, turning all eyes toward the lending team.

Credit union savings growth is the fastest it’s been in 35 years and is expected to grow by about 15% in 2021 due to stimulus payments, pandemic uncertainty, low gas spending and aging demographics, according to CUNA Mutual Group’s Credit Union Trends Report for February 2021.

In our survey, getting more loans on the books and earning increased revenue from both interest and non-interest sources topped the charts in terms of importance to credit unions and banks. The good news is that loan demand is out there. With low interest rates and unprecedented federal support for community institution lending, the trick is not convincing consumers to borrow — it’s winning the race to funding.

Targeting Young Consumers Requires a Strong Retention Strategy

It wasn’t terribly shocking to learn that the top three segments our survey participants are focused on growing over the next five years are Millennials (born 1980-1994), Xennials (born 1975-1985) and Gen Zers (born 1995-2012). Just a few of the strategies our survey participants said they were designing to earn business from these hot segments were:

- Automation, digitization and streamlined, easy-to-use products.

- Better online/mobile experience and tools.

- Digital transformation and straight-through processing (STP).

- Building personalized digital marketing automation and interaction platforms for highly engaged member groups.

- Developing mutually advantageous relationships by being proactive to people’s needs, rather than reactive to requests.

These are all great strategies and ones likely to be just as attractive to Gen X and Baby Boom consumers, too, in a post-pandemic environment. Why is that important for lenders to consider? Because the average debt balances of Baby Boomers (born 1946-1964) and Gen X (born 1965-1979) borrowers far exceeds those of Millennials and Gen Z borrowers.

If financial marketers are successful at bringing Gen Zers through the door, it’s important they stick around long enough for their life stage to allow them to fully engage with the institution’s lending services.

Keep in Mind:

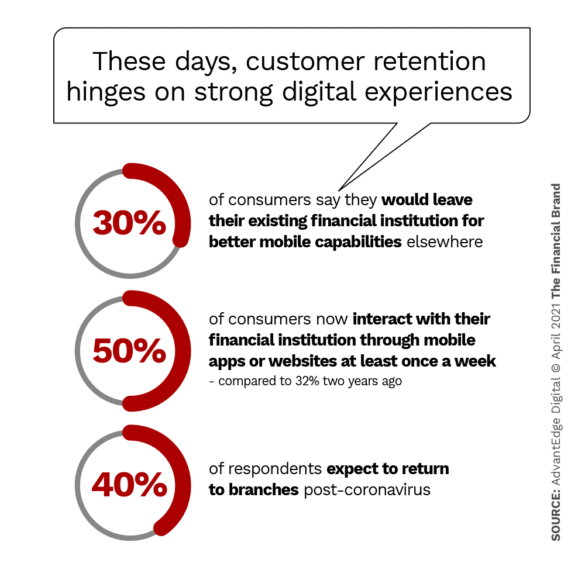

To retain consumers — and attract new ones — digital capabilities and experiences are paramount.

Of the more than 67 million credit union members in AdvantEdge Digital’s aggregate data set, more than half have a preference for digital services.

Digital Demand Drives Investment Decisions

Another potential trouble spot for lenders is how decisions around innovation are being considered and ultimately made. When it comes to digital investing, existing levels of engagement appear to be steering the ship.

Participants in the Financial Brand/AdvantEdge Digital survey said they plan to invest 2021’s digital transformation dollars in online loan applications and account opening experiences, as well as overall improvements to mobile and online banking.

Interestingly, 26% of the survey participants detected no change in digital engagement at their financial institution in 2020. Another 30% reported actual decreases in engagement last year. Is that because consumers were finding new providers to meet their increasing digital banking needs?

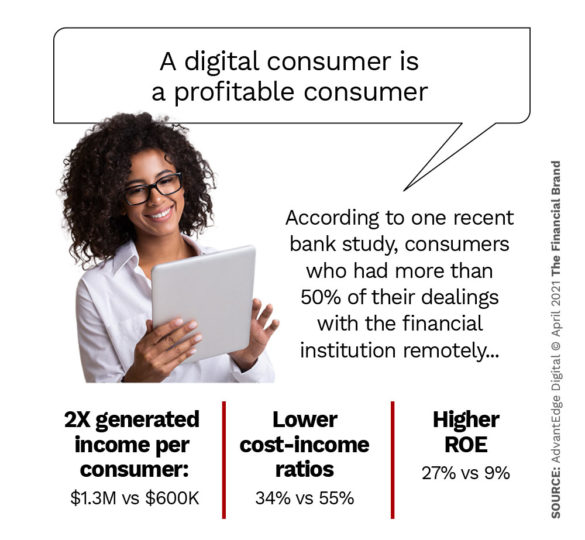

Knowing that a digital consumer is a profitable consumer, this underscores the opportunity cost of failing to lead consumers down a digital path. For financial institutions with a double bottom line imperative, the loss of engagement can be even more costly, given they may be losing business to providers less concerned about consumers’ long-term financial wellness.

Lenders Migrating to the Cloud to Achieve Agility and Scale

When it comes to making investments in digital, many financial institutions are looking to the cloud. Cloud-based software as a service (SaaS) solutions, in particular, are expected to gain a great deal of that investment — some $118 billion in 2021 alone.

According to Gartner, that’s due in large part to the pandemic, which forced organizations to optimize IT costs while supporting a remote workforce. Now that SaaS cloud applications have proven their value, the tide of cloud demand is unlikely to recede.

Notably, 93% of respondents categorized “operational improvements” as very or somewhat important to their lending success in 2021. This suggests lenders see a strong connection between process and outcome. Indeed, as we’ve seen at AdvantEdge Digital, streamlined processes and the integration of human-centered, intuitive technologies can have a strong impact on attaining new business and greater revenue.

Cloud-based solutions have a lot to offer in the realm of operational improvements.

Financial Institution Leaders are ‘Extremely’ Optimistic

Even after all of the pandemic chaos, fierce social unrest and regionally devastating natural disasters, 2020 left the majority of financial institution leaders with an optimistic outlook. 89% of those who took our survey said they felt optimistic about the future growth of their credit union or bank. Remarkably, more than half of those who said they were optimistic called themselves extremely so.

Digital Transformation is a Continuous Journey – Just Keep Moving.

Lenders who are feeling behind the pack on the journey to digital transformation are not alone. The important thing is to continue taking steps forward. Leaders who design their roadmaps to achieve quick wins, leverage momentum and pivot when necessary have the greatest chance of unlocking their digital potential, winning the business of more modern borrowers along the way.