Contact centers must sometimes feel like the Rodney Dangerfield of financial channels — they “Don’t get no respect!” But based on the role they played in the tumultuous pandemic year, they should.

With several months of channel data across various stages of the pandemic, we now have some insights into the new normal and the changing role of contact centers.

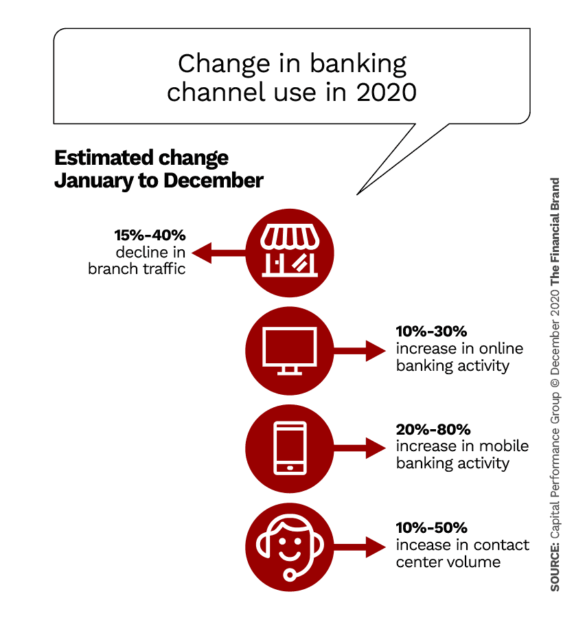

Branch traffic was down between 15% to 40% from yearend 2019 to December 2020, depending on the institution; online banking activity was up 10% to 30%, and mobile banking activity increased 20% to 80%. For some institutions, however, contact center interactions, even toward the close of 2020, remained elevated by as much as 50%.

There are few reasons to believe that the industry will go back to the old way of doing things, even as vaccines become increasingly available in the year ahead. That outlook is — or should be —welcome news for the industry. Financial institutions simply can’t afford the old normal given the interest rate, profitability and competitive challenges they face.

As banks and credit unions adapt to the new normal by reducing branch networks and accelerating digital agendas, three difficult questions emerge:

- How will financial institutions continue to deliver on their value propositions — many of which hinge on the quality of human-delivered service and personal relationships — in an increasingly digital world?

- How will institutions grow and foster new accounts given the role the branch has traditionally played in acquiring and servicing households?

- How will banks and credit unions connect their customers to more streamlined solutions without hindering the customer experience?

We believe that the contact center plays an important role in answering these questions. But to fulfill that role, it requires special attention.

Will Chatbots Dominate? Not Just Yet

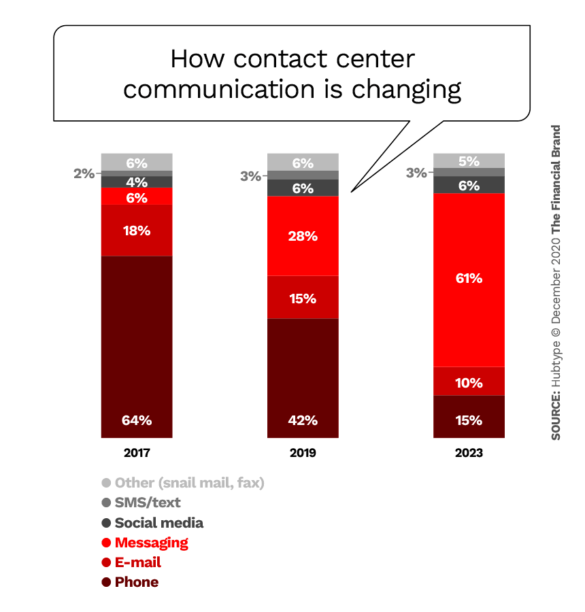

Well before the pandemic, the role of the contact center on the customer experience was changing as customers shifted to digital interactions. A study by Hubtype, an online customer communication service that works with Fortune 500 companies, demonstrates the growing shift from phone call volume to messaging via platforms like Facebook’s Messenger and WhatsApp platforms.

That shift is one reason many financial institutions have moved away from calling these facilities “call centers.” With that said, contact center volume remains elevated, and generating efficiencies is at the top of both near-term and long-term priority lists for most institutions. Therefore, much attention will be given to chatbots and artificial intelligence over the next couple of years.

“The key to delivering an exceptional customer experience in the contact center is making it easy for the customer to ‘bail out’ of automated interactions and immediately get to a human.”

— Nick Kieffer, Simmons Bank

Chatbot capabilities are becoming increasingly available and affordable in banking through a number of vendor offerings. While their capabilities keep improving, these technologies aren’t yet doing much to generate exceptional customer experiences or trust, however. Forrester found that only one-third of American customers trust chatbots to handle simple financial transactions and two-thirds don’t trust them to handle complex transactions. Further, nearly 80% of people polled want to speak with an agent as opposed to a chatbot according to a survey by conversational AI provider Uniphore.

“The key to delivering an exceptional customer experience in the contact center is making it easy for the customer to ‘bail out’ of automated interactions and immediately get to a human even though you’d like them to adopt the automation for efficiency purposes,” says Nick Kieffer, SVP of Customer Service, at Arkansas-based Simmons Bank.

Live Chat and Other Tools Boost Capabilities

For most banks and credit unions, a seamless transition from automated channels to a human is highly dependent upon the organization’s technology, quality of data, and the ability to design effective operational processes (particularly those related to authentication).

As contact center volume remains high, financial institutions continue to leverage email, text, chat, how-to demos and social media channels to drive adoption into more cost-effective automated channels while providing customers a choice for interacting with them. For some, the introduction and enhancement of live chat is an emerging solution.

Simmons Bank recently extended its digital communication capabilities through the introduction of a secure messaging team. The team consists of dedicated personnel who are specially trained to deliver well-crafted live-chat messages, provide a number of services that customers expect in the branch, and interact within the channel the customer is frequently using. The goals are to enhance the overall experience and help educate consumers about digital banking, explains Kieffer. The individuals on the team can handle up to three times the number of interactions as a phone agent, he adds.

With more accounts being opened online, other institutions are strengthening their digital onboarding and relationship management practices, with many of them assigning a banker from the contact center to provide personalized human contact. Umpqua Bank’s Go-To app, WSFS Bank’s myWSFS, and Commerce Bank’s Connect apps are just a few examples of keeping the bankers at the center of transactions, even if the customer interactions are initiated digitally.

The Contact Center as a Growth Engine

As the importance of the branch diminishes for many customers, digital marketing is playing an essential role to support direct household and product acquisition.

But does the contact center — traditionally a reactive unit — play a key role in household acquisition? For Community First Credit Union of Florida, the answer is a resounding yes.

In 2020, Community First established the “Express Team” as part of a new experience around membership opening and consumer lending. Given that many consumers still prefer to open new accounts with a human involved, the credit union created a dedicated team to process new memberships and open loans with one phone call.

To make this work, Community First revamped its account opening processes, staffed the Express Team with some of its best branch employees, and provided technical training to ensure a smooth experience. During the interaction, documents and signatures are gathered in real-time and underwriting decisions are made in under two minutes from an automated system (or by a small team of dedicated underwriters for members who are not instant-approved). Accounts are funded and the member is congratulated before the call is complete.

“Our members have absolutely been blown away by the experience” says James Urban, AVP, Member Experience Center at Community First. Through November, the Express Team is exceeding its new membership goals by over 700%, says Urban. The program is serving as a springboard to a number of profitable new member relationships, and also helps the credit union capitalize on the consumer refinancing boom.

4 Suggestions to Upgrade Contact Center Performance

It’s easy to say that in an era of fewer face-to-face interactions, an integrated digital/contact center strategy will be essential to keeping your people at the forefront of the customer experience. To achieve that, however, top management has to answer a couple of questions: What is the right strategy for the customer and for the organization? What customer experience are we trying to deliver in the contact center?

With a clear direction from the top, institutions can build out their contact center capability along these four lines:

1. Connecting the talent. The skillsets of an Express Team member, as used by Community First Credit Union, are very different than those of a live-chat team member, and from those of a video banker. Rarely can a single contact center employee succeed in delivering all of these different experiences. Therefore, getting the right people into the right job is essential.

2. Simplifying the job. Almost any contact center employee can describe the struggle of having to navigate across various systems to answer questions, process transactions, and open accounts. Management can alleviate many of these customer experience hiccups by streamlining processes and consolidating technologies.

3. Structuring management systems. With the roles and responsibilities of contact center employees now much more varied, performance measurement and incentive systems need to be realigned accordingly. In both examples cited above, the special units have their own goals and service-level agreements.

4. Managing remote work models. As most financial institutions pursue a hybrid remote-work model going forward, there will be significant opportunities to provide contact center employees with increased flexibility, enabling institutions to reduce physical office space, recruit beyond traditional geographic borders, and provide additional opportunities among the disabled.

Of course, the remote model has significant challenges as well. Financial institutions continue to struggle with onboarding new employees remotely. In addition, managing contact center volumes and staff productivity presents technological and management hurdles that will need to be addressed. Attention should be given to real-time dashboards that help to manage contact center capacity.

Done right, however, a high-performing contact center will result in enhanced customer experiences, operational efficiency, and deliver growth during a time when banks and credit unions must rely less on their physical delivery channels.