You could call Bank of America’s Life Plan app the digital planning tool for people who hate to plan, but know they should. That would be a lot of people. Two-thirds of the U.S. population don’t have any sort of written plan for their lives, and about half of them agree it would be valuable if they did, according to DHM research.

Life Plan was launched nationally in early October 2020, but has been in use by about 80,000 consumers since about the middle of 2019. Given the checkered history of personal financial management tools in banking, BofA takes pains to not call Life Plan a financial planning tool. Or, at least, it points out that it’s much more than that. Per a company statement, Life Plan is “A new digital experience through which clients can set and track near- and long-term goals based on their life priorities … and act on steps toward achieving them.”

“It’s a new breed,” said David Tyrie, Head of Digital, Financial Center Strategy and Advanced Client Solutions for Bank of America, during a presentation to analysts.

Two things about this product mark it as a development retail banking executives should be watching:

1. How Life Plan uses data. The solution incorporates data from many different parts of the bank — including content and customer data — and combines it, using artificial intelligence, with input customers give in the app. “We are really trying to use data in a different way,” Tyrie continues. “Most players use transaction-based data. Life Plan actually gathers input from the customer and what’s important to them and matches that with transaction data to create a better user experience.”

As Tyrie told analysts: “This gives you a preview of how we’re envisioning using data in the new world of banking. Digital banking has brought convenience to everyday banking, but is rapidly moving towards becoming a much more personalized operating system for your financial life.”

2. How Life Plan is omnichannel. The digital solution functions within both BofA’s mobile app and its online banking platform. It doesn’t sit, “off to the side,” in Tyrie’s words. “This is not a separate experience,” he states.

Life Plan is also integrated with the bank’s digital assistant Erica. And like that AI-powered app, the more Life Plan is used the more intelligent it will become, Tyrie notes.

Perhaps more significantly, Life Plan operates in parallel with the institution’s 4,200+ banking centers. Banking center associates see not only the same data that a customer using Life Plan sees, but in the same format, according to Eve Varner, Digital Planning Executive, who has overseen the Life Plan development and launch. That move confirms BofA’s commitment to a digital+human strategy.

“We’re seeing incredibly rich conversations triggered between our associates and our clients,” Varner told analysts. “I feel like our [people] really know them and really care about what’s important to them.”

How Life Plan Works

Life Plan is available for free to any Bank of America customer through its app and online banking. In the dialogue that follows, Varner addresses where the uptake has been strongest so far.

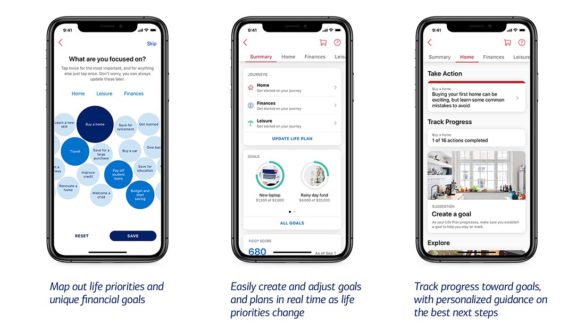

Everything about Life Plan starts with a consumers selecting what’s important to them in their life right now as well as in the longer term. BofA employs a form of gamification to accomplish this, using a series of “bubbles” that people click on in the app.

As shown, the bubbles are labelled with various goals or needs. Clicking once highlights that goal. Twice makes it larger — a priority, in other words. Consumers can revisit this selection any time as situations change within their lives — being furloughed during the pandemic, for example, or after making a decision to move to a new home.

The Life Plan categories fall into seven “buckets”: Finance, Family, Home, Health, Work, Leisure and Giving. Each of these categories and the specific goals and tasks selected lead to logical next steps within the app, such as creating a budget to meet a down payment. Life Plan also helps consumers track their progress toward these goals and steps and will prompt with “gentle nudges” at times.

In addition, a user can reach out and connect with a bank staffer at any time either directly or by setting an appointment.

The Financial Brand spoke with Eve Varner about Life Plan to find out more about the megabank’s strategy for the solution, its experiences with it so far, and next plans.

Read More: Why BofA – Not Fintechs or Amazon – Should Keep Bankers Awake at Night

Bank PFM solutions have had poor uptake over the years. How will Life Plan be different?

Eve Varner: The huge difference with Life Plan is that we don’t start the conversation with how much money do you have and how do you want to invest it? It’s not about that. So it doesn’t feel like an arduous, daunting, overwhelming exercise that most of us as consumers don’t feel their qualified for.

We’re saying, “Let’s start with what you’re trying to get done today.” That’s the difference and that’s why we’re seeing it resonate with our clients. And with our associates too, because it’s a much more natural conversation to have with clients.

Clients might end up managing their cash flow or allocating an investment. But those activities are in service of a set of goals and objectives that they have set up.

What sets Life Plan apart from Mint and other fintech financial planning tools?

Varner: Mint and its compatriots obviously are very good at what they do, but they’re narrowly focused. Life Plan is very broad. It’s really the connective tissue between all of the possible resources we would want to put in front of a client depending on what they’re trying to do.

That’s very different from a single-focused aggregation capability or an investment allocation capability. We have those capabilities, too, and Life Plan makes sure we put them in front of you if they’re of use to you and depending on what you want to do.

Is this something consumers will use on a regular basis?

Varner: Life Plan is not a one-and-done type of traditional financial plan. It’s an explicit recognition that there’s a bunch of stuff that goes on in anybody’s life at any given time, which is going to change over time. So inherently we expect to see ongoing sustained engagement across all of our platforms.

Life Plan will become the way that you engage with the bank because it’s really engaging through the lens of what’s important to you. As your life changes Life Plan will adapt and help keep you on track or update your goals with you.

What kind of activity have you seen so far and in what channels?

Varner: Just to give a sense of the interest, in the week after the national launch we had 8,000 Life Plan conversations or sessions. It’s been increasing daily since then.

So far the overwhelming majority of people are interacting with Life Plan in the mobile app. But we also see many who initiate the experience in the app and then come into a financial center. That could lead to a conversation with a relationship manager or a lending officer or a small business banker. And then the third category is people who are introduced to Life Plan by an associate.

With in-person conversations it starts narrowly. But as the client works with an associate and uncover more objectives and goals, it starts to impact other family members. So we’re seeing Moms bringing in kids to open up first credit cards and savings accounts, or bringing husbands or wives or partners. We’ve seen quite bit of that, actually. People realize this is a different kind of conversation I’m now having in this bank and I want my family to be part of it.

Read More: Consumer Frustration With Banking Apps and Mobile CX Lingers

Does Life Plan appeal equally across generations?

Through the pilot and into the early days after the launch, we’ve been over-indexing in Gen Z and younger Millennials. These folks tend to gravitate and spend more time with digital experiences. When we look at the goals they’re selecting, it’s really the getting-started type objectives around setting up a budget, establishing credit and saving for a new apartment or home.

In addition, with the COVID situation, people feel overwhelmed and under-prepared to deal with the changes in their life or setbacks and they’re asking for help. Life Plan has really resonated with them.

Older Life Plan users are leaning more on in-person interaction — either initially or through a follow-up from the app. We’ve made it very clear that this product is really omnichannel and on the client’s terms.

What’s an example of how you provide help in the Health category?

Varner: It would depend on how old you are and what your financial situation is. If you’re young, it could be simply some educational content around staying healthy and keeping fit. If you’re a little bit older and conscious about health care cost, it could be content about how much health care cost to allow for in your retirement plan. Or education around an HSA account.

How does Bank of America benefit from Life Plan?

Varner: Our job is to surface the right resources at the right time. Sometimes that’s an account, but that’s really not the primary objective. It’s really about what is the information and education and recommendations that would help you make progress on your goals. if ultimately that ends in some kind of fulfillment, that’s okay because it was in the context of something that client wants us to do. We will do well by just giving clients what they need.

In addition, Life Plan gives us really rich and robust insights into what’s on our clients’ minds. And that in turn is extremely valuable for our associates and let’s them have much more relevant and timely client conversations.

Next Steps for BofA’s Life Plan App

During the analyst presentation, David Tyrie described the current Life Plan app as version 1.0, but said they’ve already mapped out three future versions. While 1.0 has what he calls “basic functionality” relating to the seven life categories, later editions will be adding “more content, more capabilities, more solutions” for higher net worth individuals.

Eve Varner adds that right now, “we’re focused more on the client who doesn’t have the benefit of the hand holding of an advisor and is looking for help.”

Looking ahead on a more technical point, Varner says that while Life Plan at present pulls data only from within the bank (other than content from outside experts), incorporating external client data makes sense and is on their road map.

Asked by an analyst how BofA will assess whether Life Plan is a success, Tyrie said it will hinge on two factors predominantly:

1. How many people use this to set goals and what is the status of their meeting the goals?

2. From a internal perspective, Has Life Plan increased digital engagement with our client?