Banks are constantly looking for ways to increase lending and reach potential customers with new products and services. As mobile devices are growing in popularity, more institutions are adopting a mobile-first strategy, positioning their products and services to be accessed from any device. Aside from mobile banking, some institutions are deciding to branch out and develop apps to attract customers in earlier stages of their purchasing decision process.

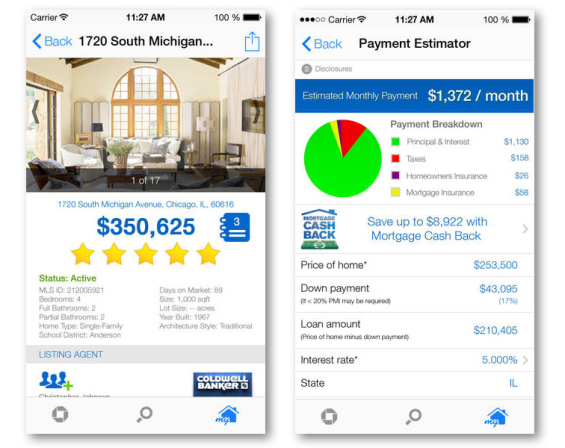

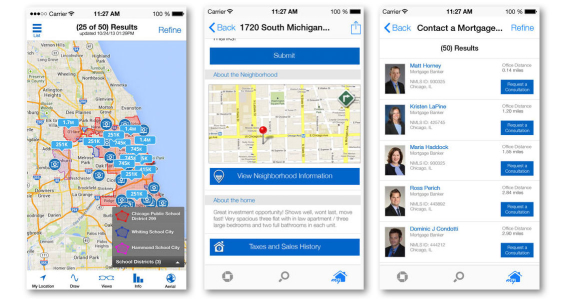

Recently, Chase Bank launched a mobile app for potential home buyers to aid in their process of finding and financing a new home. With the Chase myNewHome app, users can search for homes, rate their favorites, and compare features with other listings. Chase has built this app to ride the wave of other popular home buying apps such as Zillow and Trulia.

Recently, Chase Bank launched a mobile app for potential home buyers to aid in their process of finding and financing a new home. With the Chase myNewHome app, users can search for homes, rate their favorites, and compare features with other listings. Chase has built this app to ride the wave of other popular home buying apps such as Zillow and Trulia.

While these apps have already established popularity and traction, Chase is hoping to drive adoption with their existing customer base as well as entice new customers. As financial institutions approach this trend, many will need to conduct a cost-benefit analysis to determine the viability of building their own custom app or to advertise within apps already on the market.

Development Costs vs. Advertising Cost

Development costs for a custom mobile app can range based on how extensive and robust the app will be. Typical costs for development can range from $5,000 to $100,000 and could take upwards from 6 to 12 months to build, test and publish. Beyond development costs, there will be monthly maintenance and annual hosting fees as well.

Advertising within popular home buying apps has an initial investment cost and supplemental fees as well.

Popular home buying app Zillow offers two ways lenders can advertise on their network. One option for advertising is in the Zillow Mortgage Marketplace (ZMM), which requires a setup fee of $25 with an annual commitment of $20,000. Although the ZMM is one-size-fits all solution, stating, “Zillow Mortgage Marketplace (ZMM) is best suited for mortgage lenders who are successful sourcing online business, at scale.” Zillow says that successful ZMM lending partners: embrace transparency in the marketplace, employ a centralized origination staff, and utilize a lead management system such as Marksman.

Advertisers will also need to use a product pricing engine through one of Zillow’s API Partners. Partners include Optimal Blue, Loantek, Loansifter, LoanXEngine, and Leads360. Prices for product pricing engines will vary among providers. Zillow’s cost-per-click model uses dynamic pricing with the national average ranging from $0 to $15+ per click.

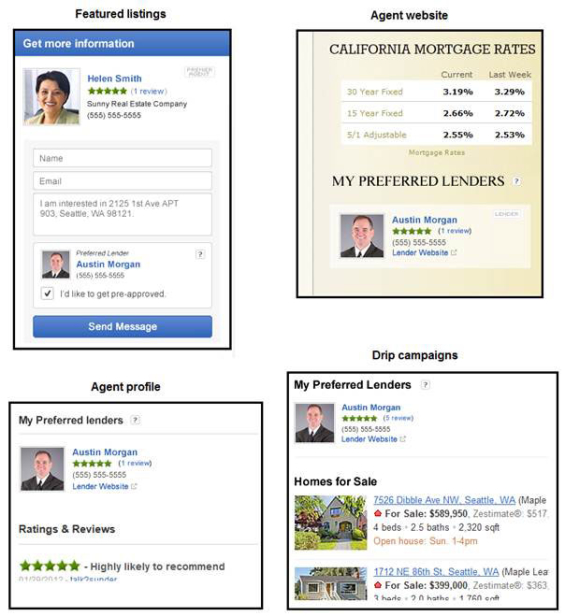

Zillow also offers lenders the option to co-market with listing agents. Agent and Lender co-marketing is for professionals who want to share marketing costs on Zillow. By sharing marketing costs, agents and lenders can often reduce their marketing spend and increase their ROI.

A Premier Agent can invite a lender to share marketing costs with them. The agent specifies the dollar amount he/she would like each lender to contribute; up to 50% of the agent’s total spend per lender. Once the lender confirms (they will get an invitation via email and have the ability to review/confirm their participation), the lender will immediately start appearing alongside the agent on Zillow.

A lender who co-markets with an agent will appear in the following places: On the agent’s featured listings, on the agent’s profile, on the agent’s Premier Agent Website, and on any e-mail campaigns the agent sends to clients from Zillow.

Customer Base and Housing Market

Approaching this decision, institutions will need to consider customer base and their local housing markets. It is likely that Chase decided to move forward with their own app because their products and services are already online focused, projecting a favorable adoption rate among it’s existing customer base. For institutions considering a private-label app, the percentage of current customers using mobile banking should be a strong factor when considering adoption rate. Another factor is the local housing market in which the institution operates in. Before approaching a private-label app, institutions should take a strong look at the housing markets they serve and what the growth rate is projected to be over the next years.

Customer Centric

Whether choosing private-label or in-app advertising, each institution needs to consider the end-user. Consider how the users will interact with the app and the experience it provides. If the app doesn’t provide the experience the user was intending, then it will be a wasted effort. Customers want an experience that is easy-to-use, visually appealing, and has information accessible at all times. If your app or the app you decide to advertise in doesn’t meet this criteria, then you will need to rethink your options.