Industry news articles continue to report that banks are reducing the overall number of branches. It’s a bit more complicated than that, however, as some banks are also opening new branches in target markets to support growth, or to test how new smaller or open floor plan branch designs can meet the changing needs of customers.

Other banks are planning to decrease the size of their branch portfolio, but are taking it slow as they make difficult decisions around which locations to close. And then there are still some banks holding fast to their branch locations as part of their strategy to ensure high levels of customer service and engagement.

There has been significant migration of transactions from more expensive branch channels to digital channels over the past several years. At first glance, this is a positive shift. After all, banks have been promoting self-service capabilities and 24-hour convenience through their online and mobile channels for quite some time.

And when it comes to completing routine requests, digital interactions continue to be cost effective. The problem is that most banks are still not great at generating digital sales, or providing seamless online account applications across all their products.

For that reason – and also due to online security concerns – branches continue to be an important sales and service channel. Yet, according to Celent, as fewer customers visit for routine transactions, there are naturally fewer opportunities for face-to-face customer engagement. The reduced foot traffic means less cross-selling and up-selling by branch employees.

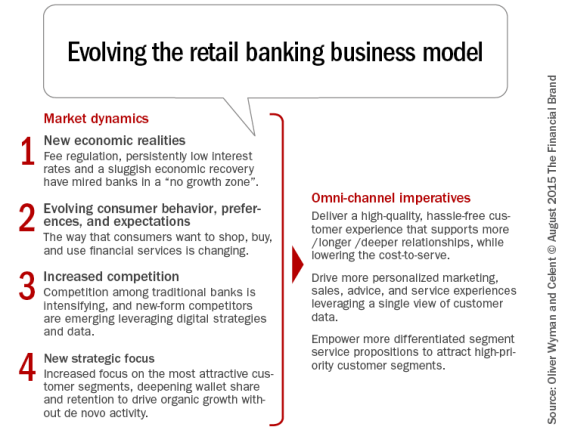

Celent highlights the market dynamics banks are facing above. Banks are evolving their consumer and small business models within the context of their omnichannel strategy, and this process is quickly intersecting with their concurrent need for branch transformation.

- Large numbers of customers are turning to digital channels like online and mobile, and interacting with their service providers via social media

- Expectations for a seamless omnichannel banking experience are being set by consumer transactions in other industries, but banks have been slow to respond

- Banking regulations have reduced the profit margin on bank products and services which increases pressure on all areas of the bank to offset this by generating new sales

- Brick-and-mortar locations are expensive to staff, operate and maintain, adding to the need for branch transformation.

Even as retail banking executives agree that branch transformation is important, it’s only one of many strategic initiatives, and in Celent’s survey of North America financial institutions, it ranked fourth behind digital banking channel development, omnichannel delivery, and customer analytics to improve sales and marketing effectiveness.

Since that survey, Celent created a new Branch Transformation Research Panel to look more deeply into the objectives, priorities, risks, barriers and likely outcomes of the growing trend that is branch channel transformation in North America. At semi-monthly intervals, this panel of retail banking executives (clients and non-clients of Celent Research) is asked research questions and the resulting data is analyzed by Celent to provide additional market insights.

Defining Branch Transformation

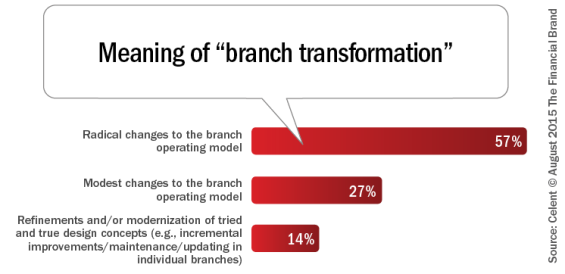

Panel participants were asked questions on their definition of branch transformation, where their financial institution is on its branch transformation journey, and how long they expect it to take as well as other questions on the likely ‘end game.’ Although 81% of the responding financial institutions agreed that branch channel transformation was imperative, there was no real consensus on the meaning of branch transformation.

Without clear agreement on the definition of branch transformation across the industry, it becomes even harder for retail banking executives to decide what it should mean for their financial institutions. Across the asset tiers, financial institutions are commonly motivated to improve branch channel efficiency and effectiveness in order to grow top line revenue and improve efficiency ratios. “These are still early days, however,” said Bob Meara, a senior analyst with Celent’s Banking practice and coauthor of the report, “with just 1 in 10 surveyed financial institutions having a clear vision for the branch.”

Driving Active Branch Channel Investment

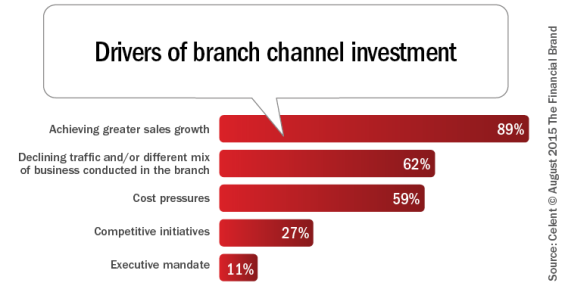

Financial institutions that are well into their branch transformation journey often share common objectives: greater sales growth and cost reduction.

As might be expected given the differences of opinion on the definition branch transformation, the research noted that many retail banking executives don’t expect that significant improvements in branch efficiency and effectiveness can be obtained without tackling a wholesale redesign of their branch network. Celent believes that a combination of rolling out new branch designs to some locations and investing in technology to optimize the face-to-face interactions in the branch can have a big impact.

The quality of the branch experience – which directly influences customer experience and sales production – is driven by the quality of the frontline employees, and the tools that can help them provide high-quality, consistent and personal interactions with customers. Although there are several different applications designed to do just that, many of these technologies are often overlooked by financial institutions exploring branch channel transformation. Celent profiles five examples and shares case studies to highlight the benefits that each can produce. One of these applications is desktop and process analytics.

Benefiting from Desktop and Process Analytics

Across many areas of the bank, technology can be used to capture and analyze customer interactions and employee behavior. Web analytics software can track customer visits and the flow of pages viewed during each session on the bank’s website.

Contact centers closely manage their operations using key performance metrics and data from ACDs, and screen and call recording. In contrast, there is little visibility into employee behavior – or the nature or quality of employee interactions with consumers – across the often large numbers of branch locations at many financial institutions.

Desktop and Process Analytics (DPA) enables banks to track and analyze the applications used by each employee throughout the day, indicating productive and non-productive time as well as hidden capacity. It can also capture the activity and process flows as employees use their computers throughout the day to help managers understand how work is being performed.

This insight can identify the need for process improvements, as well as objectively evaluate individual performance for task effectiveness, and where an employee might need coaching or additional training. DPA can also determine where employees are adhering to their scheduled activities, and where banking regulations or policies are not being followed, so that managers can intervene to address potential risk or non-compliance.

Commonwealth Bank of Australia’s use of DPA and Workforce Management is highlighted in a case study in the report, Optimizing Face-to-Face Interactions: The Missing Link in Bank Branch Transformation. As part of its “Right People, Right Place, Right Time” initiative, the bank improved its effectiveness and efficiency, while also delivering improved customer service. Desktop and Process Analytics was used to monitor 12,000 desktops in their branch network and provided management with timely and comprehensive information that helped the bank improve productivity beyond the business case expectations, while improving customer satisfaction to record levels.