With the tectonic changes altering retail banking — “trillionaire” banks spending billions on digital technology and sophisticated marketing, consumers increasingly able to switch institutions (or divide up their business) on an app — can a $50 million, $200 million or even a $500 million credit union expect to survive, much less thrive?

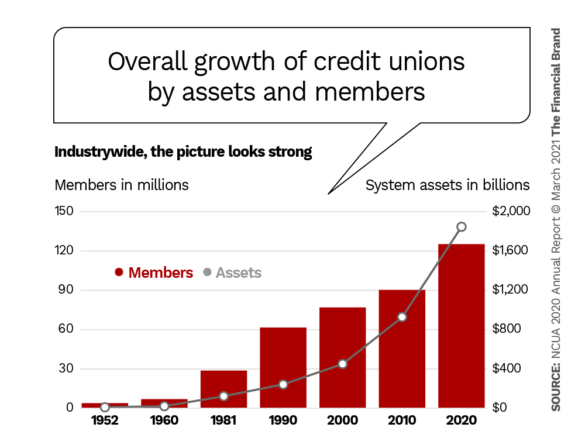

Credit unions, much like community banks, have seen their share of doomsday headlines. Yet thousands remain. In fact, the credit union industry saw significant growth in terms of total assets and members in 2020, as shown in the first of the two charts below. But that industry-wide picture masks significant pressures building up within portions of the industry.

That stress prompts some observers to state that credit unions below a certain size — some put it as high as $1 billion — are in jeopardy. The belief is that many smaller credit unions will be forced to merge into a larger institution to achieve the scale needed to exist.

It’s easy to dismiss such views as exaggeration, yet here is what the industry’s regulator says in its 2020 Annual Report:

“Small credit unions face challenges to their long-term viability for a variety of reasons, including lower returns on assets, declining membership, high loan delinquencies, and elevated non-interest expenses. If current consolidation trends persist, there will be fewer credit unions in operation and those that remain will be considerably larger and more complex.”

Sobering Fact:

While overall membership continues to grow strongly, about half of federally insured credit unions had fewer members at the end of 2020 than a year earlier, NCUA states.

The federal agency defines “small credit unions” as those with less than $100 million in assets. There were 3,387 of them by that measure at yearend 2020, representing 66.4% of all federally insured credit unions.

By contrast, many of the largest credit unions grew rapidly in both assets and members in 2020.

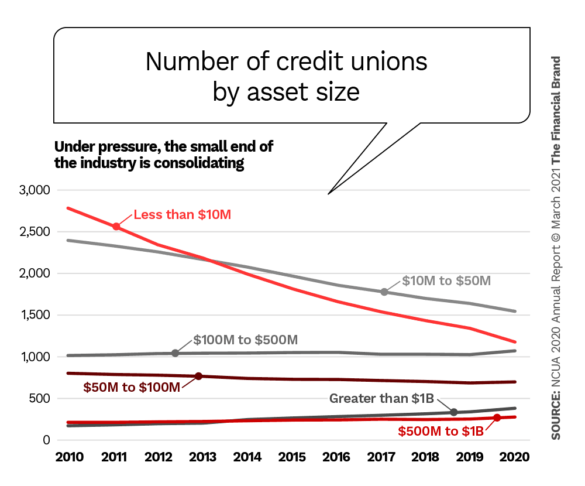

The second of the two charts shows clearly the precipitous decline in the ranks of small credit unions, particularly those with $50 million in assets or less. Even as hundreds of small credit unions have been disappearing, the biggest have grown bigger.

A Tale of Two Industries

The impact of all these competitive forces, including stiff competition from fintech lenders and neobanks, is being felt very unevenly within the industry, as shown in the table below. Return on assets for the smallest credit unions is tiny, and only rises to levels that will enable an institution to grow at the larger institutions.

Beyond ROA, most measures of growth for the smaller institutions were negative in 2020, while the large institutions saw strong growth.

Key credit union stats by size of institution

| Asset Categories | ||||||

|---|---|---|---|---|---|---|

| As of Q4 2022 | Less than $10 million | $10 to $50 million | $50 to $100 million | $100 to $500 million | $500 million to $1 billion | Greater than $1 billion |

| Number of credit unions | 1,159 | 1,541 | 687 | 1,063 | 279 | 370 |

| Number of members (millions) | 0.8 | 4.1 | 4.5 | 18.9 | 14.1 | 81.9 |

| Total assets ($ billions) |

4.8 | 39.5 | 49.4 | 237.5 | 197.0 | 1,316.2 |

| Total loans ($ billions) |

2.2 | 18.2 | 25.3 | 140.8 | 128.0 | 848.2 |

| Total deposits ($ billions) |

4.0 | 34.5 | 43.4 | 209.1 | 170.8 | 1,125.8 |

| Average ROA | 0.06% | 0.32% | 0.43% | 0.50% | 0.61% | 0.78% |

| All Credit Unions | Year-over-Year Growth | |||||

| Deposits | -12.3% | -2.9% | 3.0% | 6.1% | 16.4% | 26.0% |

| Total loans | -24.5% | -18.2% | -11.1% | -8.6% | 3.5% | 9.2% |

| Total assets | -13.1% | -4.2% | 1.8% | 4.3% | 14.1% | 22.9% |

| Members | -19.3% | -15.7% | -11.3% | -9.5% | 1.8% | 9.7% |

Source: NCUA 2020 Annual Report

“Thousands of credit unions face the prospect of shrinking market share and declining ROA if they cannot achieve the scale necessary to evolve,” says Jim Perry, Senior Strategist for Market Insights. “There will be exceptions, but competition is more intense, the consumer is less loyal and the pressure to consolidate is growing. Credit unions must face the reality that size and strength matter.”

Even NCUA points out that many credit union customers have several financial institution alternatives and can move funds quickly and easily among them. In fact, of consumers who consider a credit union to be their primary institution, just over half (56%) also use a bank for some type of financial service, the agency states.

Read More: Digital-First Banking Doesn’t Mean Chasing Every Fintech Innovation

Impact of the Megabank Magnet

In a report, banking research firm Raddon warns credit unions that “Your members are flocking to the big banks daily.” The company found that of Gen X and Millennial consumers it polled, the percentage who said a big bank is their primary financial institution increased from 38% and 47% respectively to 52% and 68% over the two-year span from 2018 to 2020.

Robert Flanyak, President and CEO of Chrome Federal Credit Union, Washington, Pa. ($168 million in assets), has first-hand experience with the impact of megabanks. He tells The Financial Brand that the largest banks have discovered his region. “Two years ago, Chase had zero branches in southwestern Pennsylvania. They now have 22. Bank of America two years ago had zero. They’re up to about a dozen branches now.”

“Back in the day we would like to compete against Bank of America because we always felt our service and our attention to members would make us stand out. But now it’s different. The digital piece has really taken over.”

“The reason most new checking accounts today are being opened with the big banks is not because they have nice people sitting in the lobby. It’s because they’ve got great digital products, a brand that resonates with Millennials and are excellent at target marketing.”

— Bob Flanyak, Chrome FCU

Switching Surge: Will it Help or Hurt?

The pace of consumers switching primary financial institutions may be headed for a tear in the second quarter of 2020, according to data collected by Rivel from its database of about 200,000 financial institution customers. About a third of households are thinking of switching now, according to Bruce Paul, Managing Director, Banking Research.

Rivel’s data shows that about 21% of credit union members say they are unhappy or open to switching primary banking institutions. “That sounds bad,” says Paul, “but it’s lower than the 31% of bank customers who say the same.”

The researcher notes that high levels of switching bode well for credit unions because 64% of households say they would at least consider using a credit union. But here again, the edge goes to the larger credit unions. Rivel’s data shows that about 10% more consumers are looking to leave a smaller credit union than a larger one. “Compound that over a couple of years and that’s a big difference,” Paul states.

Read More: Why Building Digital Banking In-House Can Work for Small Institutions

Is it About Size, Scale or Mindset?

“It’s really an oversimplification to say you need to be $500 million or $1 billion or $2 billion because there are so many variables,” Chrome FCU’s Bob Flanyak states. “We all need to get bigger so that we can afford to do more. But don’t use that as an excuse to finding new and better ways to serve your members.”

By aggressively partnering, Chrome has doubled down on technology, including an upgraded website and mobile app that resonate with Millennials and Gen Z. This strategy also allowed the small credit union to become SBA certified in time to take part in the PPP programs, bringing it new business relationships.

The Chrome CEO observes, however, that not all credit unions are coping well with the rapidly changing environment. It’s not really about scale, he says, but about mindset. “Credit unions that don’t evolve, they’re basically dying a slow death,” he states.

“Size doesn’t necessarily automatically imply you will succeed,” observes Amanda Thomas, Founder and President of credit union marketing specialist TwoScore. “I’ve seen credit unions that are large and they’re just coasting and not doing anything different. And I’ve seen a lot of small credit unions do the same thing. It all comes down to your philosophy and the grit,” says Thomas, who has worked at a $30 million credit union.

Amplifying on the mindset point, James Robert Lay, Founder and CEO of the Digital Growth Institute, differentiates two types of thinking: “If an institution’s leaders want to go down the path to a digital future, they will find the resources. But if they start out by saying, ‘We don’t have the resources,’ they’re already behind.”

“COVID should have been a wake up call to really spur a change,” says Lay, but he sees too many credit union leaders falling back on what they think they know. He likes to ask them, “Have you ever opened an account with a fintech or neobank?” They’re smart people, he observes, but there’s a gap between intellectually knowing something and experiencing it.

Some of the very same forces threatening the survival of small institutions also provide the means to adapt and succeed. The growing number of fintech providers enables very small credit unions to offer online account opening, card controls, loyalty programs and P2P payments, notes Jennifer Addabbo, CEO and Co-Founder of CU Engage. “A modern digital presence makes them seem bigger,” she says. “It’s a great leveler.”

Near-Term Merger Outlook

Jim Perry cautions that small credit unions can’t simply “nibble away” at large, expensive initiatives such as personalization, security and an efficient infrastructure. “The post-pandemic consumer is not going to wait around while credit unions make incremental steps forward,” he states. That’s why he believes a merger or acquisition is the fastest way for small credit unions to achieve the scale to be able to keep up.

“I think that that trend is going to start to pick up later this year as the realities of these financial dynamics really come home to roost,” predicts Chrome’s Flanyak. “And those that haven’t prepared, those that haven’t kept current, they are going to be stuck.”

Putting an exclamation point on that statement, he says a couple of small credit unions have reached out to him to join up with Chrome, because they’re having a hard time coping with this environment.

While there is no definitive answer on how big a credit union needs to be to survive, it’s obvious from the observations above, including from the industry’s own regulator, that small credit unions (under $100 million) face a dire future on their own.