Omnichannel was well entrenched as a concept long before “fintech” became common parlance. But to Jason Bates, a founder of a challenger bank, the term omnichannel is still the “king of buzzwords in retail banking.”

Bates, Deputy CEO of 11:FS and co-founder of Starling Bank and Monzo, says that omnichannel is “doomed,” because it’s based on a false assumption.

“It grows from the idea that ‘channels’ are all equivalent and interchangeable,” he says. Unsurprisingly, he argues that digital channels trump physical channels — both in importance and impact.

Fintech influencer Chris Skinner hates the term “omnichannel” too, adding a “vomiting emoticon” after using it in an article. Why? Because it reflects backwards thinking, in his view. “You’re adding things to an old structure, rather than redesigning the structure to be digital,” he explains. “Digital should be at the core.”

But search for “omnichannel banking” and the majority of headlines you’ll turn up are similar to this one: “Why Banks Must Have an Omnichannel Digital Strategy.” And many reports from reputable sources can be found discussing the importance of omnichannel.

So what gives? Is omnichannel a legitimate, even vital, strategy for banks and credit unions to follow? Or is it or a waste of time and resources?

Why Omnichannel Can Be a Distraction

Most experts in the banking industry agree the term omnichannel evolved from the concept of “multi-channel.” The earlier term referred to the availability of multiple ways to do one’s banking — branch, call centers, ATMs, websites and more recently mobile apps. Consumers would start and end in each of these channels. There was little overlap. Each had its own tech stack.

With omnichannel, consumers can float between the channels. As Pradip Patiath, a senior partner in McKinsey’s banking unit explains, people could start in a branch, pick up where they left off on their mobile app at home, then finish the process by phoning the call center — with all their progress and information seamlessly transferred along the way.

Ideally the experience would be similar no matter how the consumer engaged. How often do they do that? According to research by McKinsey, people use more than one channel to complete a task upwards of half of the time.

So how could anyone argue omnichannel is a bad thing? Why the pushback? Speaking with omnichannel naysayers and critics, three themes emerge:

“It’s a mistake thinking that consumers care about channels. Consumers care about experiences.”

— Steve Dennis, SageBerry Consulting

1. Omnichannel is too focused on upgrading the existing way of doing things. As Chris Skinner suggests, banks and credit unions need to expedite their evolution into truly digital-first enterprises.

2. It diverts attention from more important matters. Retailers, who have been wrestling with omnichannel as much as anyone, offer a strong lesson. “It’s a mistake thinking that customers care about channels,” states retailing consultant Steve Dennis in Forbes. “Customers care about experiences, about solutions, about ease and simplicity.” Or as Ron Shevlin, Cornerstone Advisors’ Director of Research, observes, “Consumers will use whatever channel is most convenient for them. They just want the job done.”

3. Given current systems, the sheer complexity presents a high hurdle. “Pulling off proper omnichannel banking is ninja-level in complexity,” says Chris Nichols, Chief Strategy Officer for CenterState Bank in a article. “Most of the ‘experts’ throwing around ‘omnichannel’ do so with little regard for practicality and little respect for having to deal with a traditional core system.”

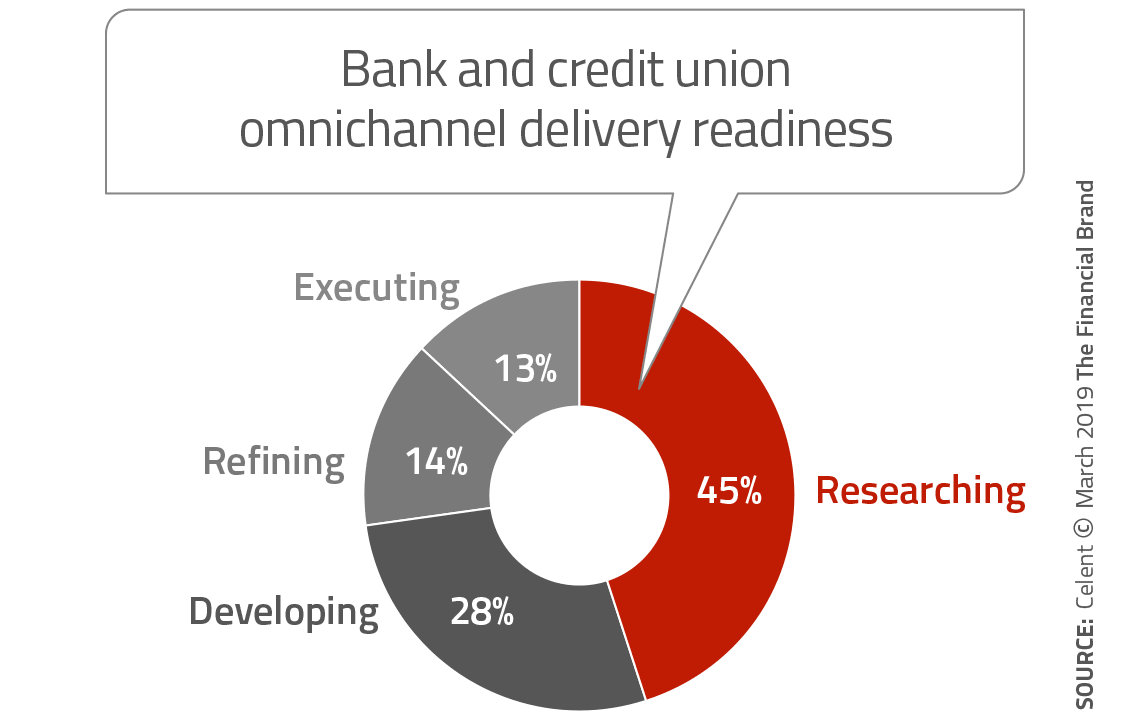

That third point has likely been a cause of the slow progress being made by banks and credit unions in implementing omnichannel banking, according to 2019 data collected by Celent.

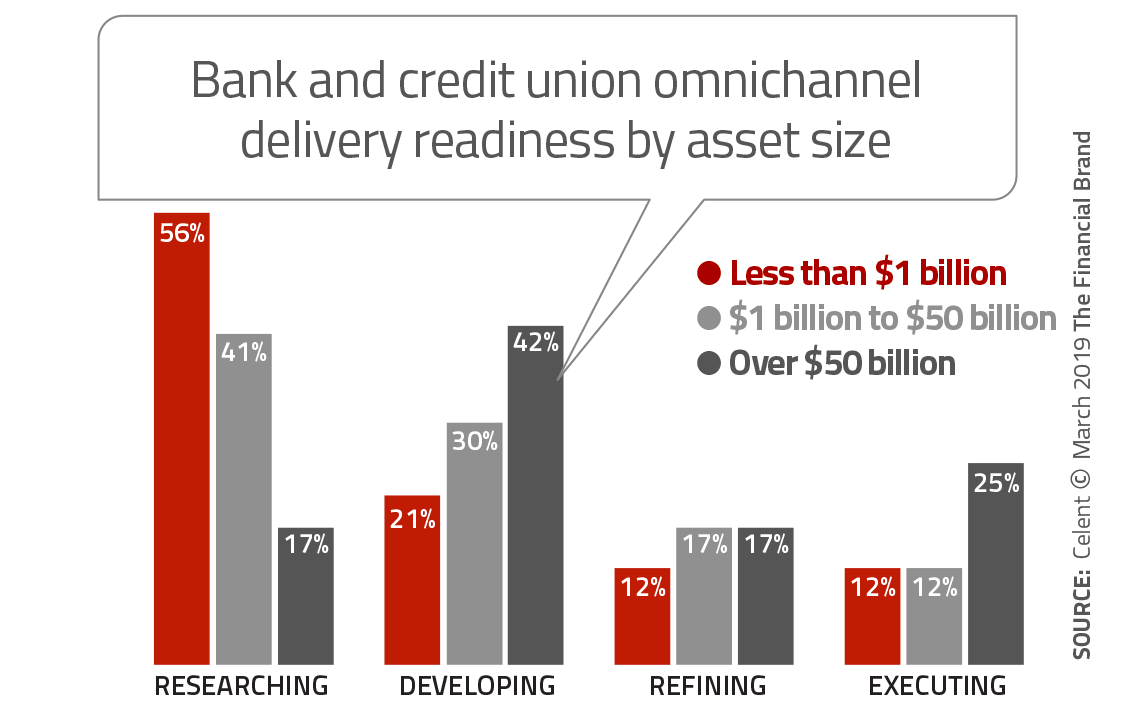

The 11% of institutions saying they are “executing” an omnichannel strategy is up from 9% in 2017. Celent Senior Analyst Bob Meara describes that increase as “clear progress, but slow-going.” Regarding the chart above, Meara says that “ironically, even though the large banks have a comparably massive task to deliver omnichannel, they remain clearly ahead of smaller financial institutions.”

Among community-based financial institutions of less than $10 billion in assets, Celent data show that about half of both banks and credit unions are still researching omnichannel capability. Credit unions have a slight edge over banks in executing, 11% to 8%.

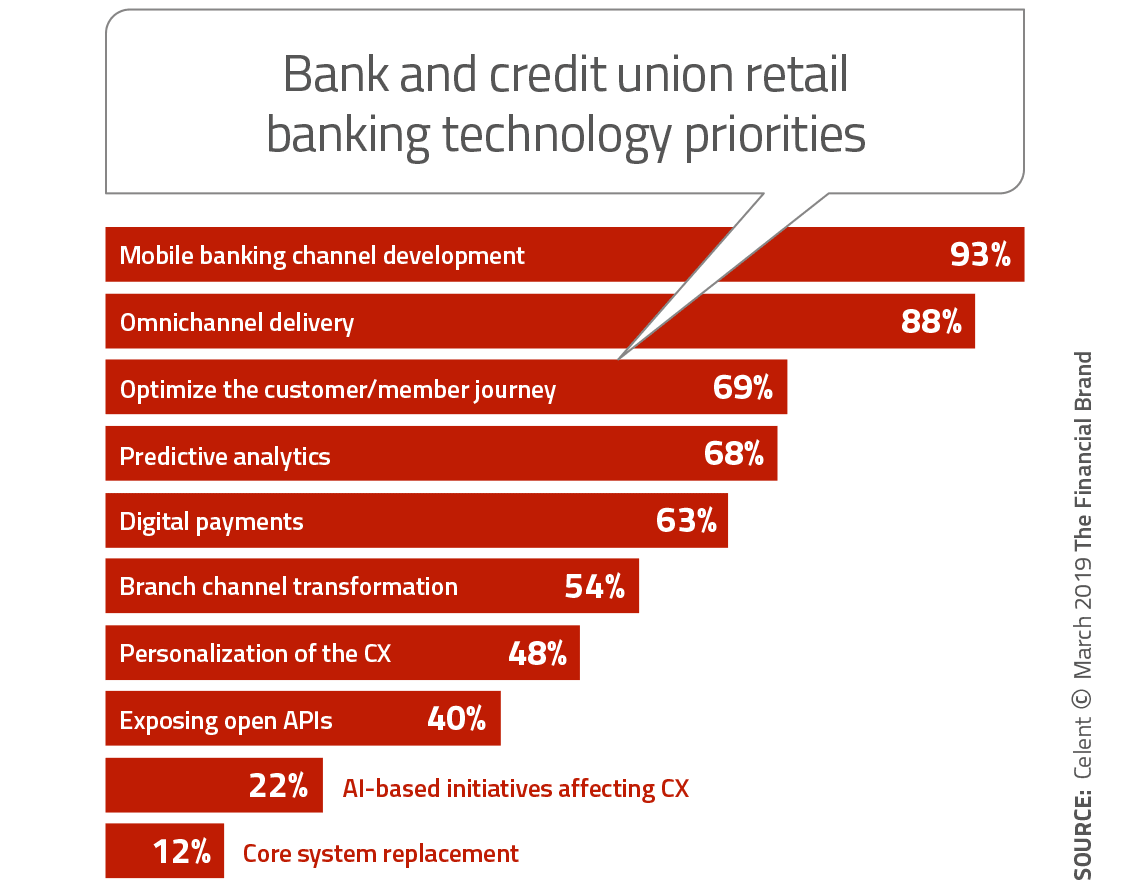

Despite the lag in actual implementation, Celent’s data show that omnichannel delivery is a close second to mobile channel development (88% to 93%) in what banks and credit unions say are their most important retail banking technology priorities.

Read More:

- An Omnichannel Approach to Onboarding Banking Relationships

- 4 Key Strategies to Create a Future-Proof Digital Bank

Is Omnichannel a Cop Out?

Although some proponents advocate for retiring the term “omnichannel,” McKinsey’s Patiath argues that in reality “omnichannel,” “mobile first,” and “digital first” all point to essentially the same capabilities.

“They’re all part of the fundamental debate about how consumers want to interact with financial services providers,” he says — both now and in the future.

Yet Patiath describes omnichannel, as it’s usually intended, as a cop out reflecting banking institutions’ uncertainty over how consumer engagement will evolve. Branches are at the heart of this uncertainty. Patiath points out that use of branches is declining sharply across most demographic segments in the U.S., and the number of branches continues to decline. Not infrequently, this creates a “prisoner’s dilemma” scenario for banks and credit unions, Patiath explains. That is: two banks have branches across the street from each other and each would like to close its branch. Neither does so, however, because if Bank A shuts its branch first, Bank B ends up winning.

An omnichannel strategy allows consumers to interact with their banking provider in any way they choose, which is inherently more expensive and complicated, Patiath notes. By contrast, he says, a company like Tesla, can make (and has) the decision to abandon physical dealerships, selling its electric cars only online, making a forward bet.

Read More:

- Financial Institutions Must Kill Pain Points in Their Customer Experience

- Fixing Banking’s Pain Points Takes More Than Digital Bells & Whistles

True Digital Transformation vs. Flashy Window Dressing

Celent’s Meara says retail banking executives acknowledge that a single platform across the enterprise would be the desired end-game. The issue is that their needs right now are more limited and immediate. “Today, so many banks just want to stand up a digital onboarding capability or something like that, and they need it fast,” Meara explains. “They’ll say to vendors, ‘Don’t tell me I’ve got to revisit all of my back office workflow to avoid putting “lipstick on a pig. That would take years and millions of dollars to implement’. They’ve got an itch and they need to scratch it.”

“Contact center agents should be able to say to a customer, ‘Oh, I see you stopped at this point. What can I help you with?'”

— Bob Meara, Celent

Meara understands says this is short-sighted. “Sharing data and delivering consistent yet customized brand experiences to customers across all points of engagement is synonymous with digital transformation,” he observes. And that is a change that is essential.

For example, if a consumer has gotten part way through, say, a checking account application, has a question and calls a bank or credit union’s contact center, the agent should have the context for that call. “They should be able to say, ‘Oh, I see you stopped at this point. What can I help you with?’,” says Meara. “And if it’s a relatively simple thing, the agent, suitably equipped, could say, ‘I can finish this for you in about 30 seconds.’ Versus ‘Oh, we’re going to have to start all over again.’ That’s just stupid.”

Unfortunately it’s all too common, especially in the branch, according to Meara. “That’s because so many banks, even if they have halfway decent digital onboarding capability, are still using really dated platform sales systems in the branch. And the two systems don’t talk.”

Why Omnichannel Is Overkill For Some

Offering a different perspective, CenterState Bank’s Chris Nichols says, “Omnichannel may be the wrong strategy and may lead banks down the primrose path of higher cost and more complexity.”

“Omnichannel may be the wrong strategy and may lead banks down the primrose path of higher cost and more complexity.”

— Chris Nichols, CenterState Bank

When a consumer starts and stops an application, the banker explains, the information is not stored in the institution’s core system because an account hasn’t been opened yet. Most banking institutions don’t have “data lakes” where such information could be stored, he says, and even if they did, achieving a similar look and feel across channels and a similar workflow — all needed for true omnichannel banking — would require “tons of money and engineering talent.”

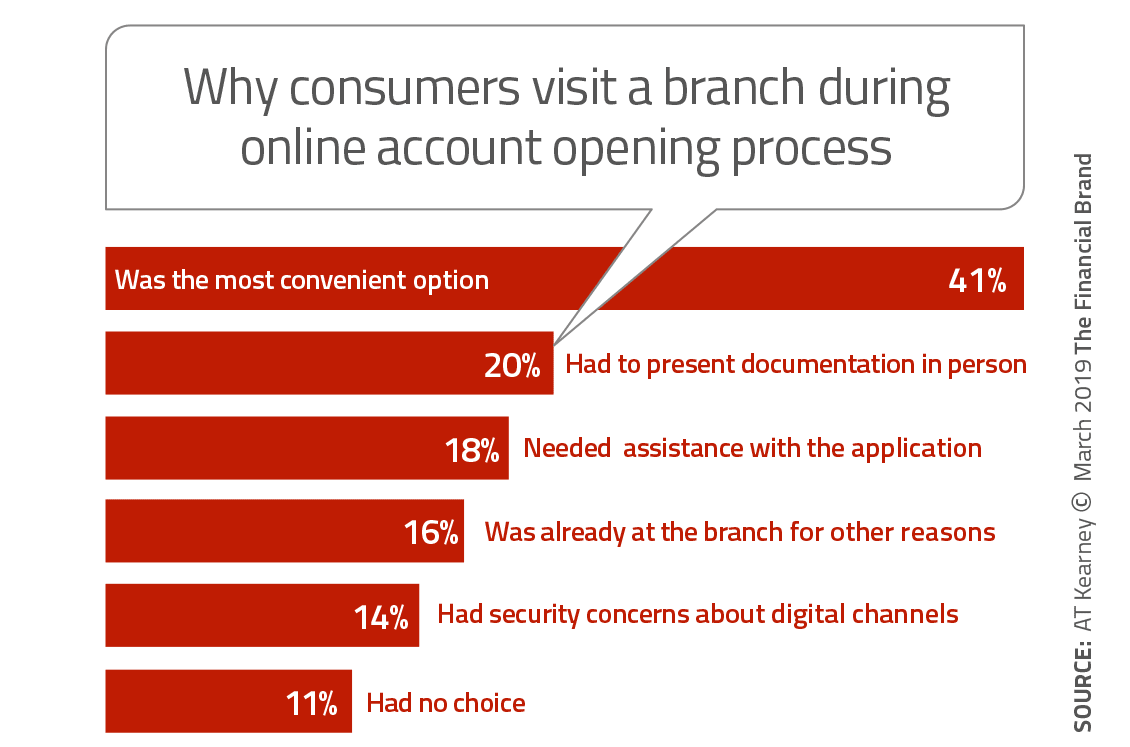

Citing data from A.T. Kearney, Nichols says 40% of consumers opening new primary accounts at large banks used multiple channels, up from 25% in 2015. That suggests omnichannel capability is more important, not less. But a closer look at the data is revealing, says Nichols. The same study asked the 40% specifically why the branch was involved.

As Nichols observes, about a quarter of consumers were forced into the branch not because they wanted to go there but because the bank or credit union required it (for ID, a signature, etc.). “Create a better digital account-opening process, and a material chunk of that 40% are likely to stay home in their fuzzy slippers to open up an account,” Nichols states.

The data also suggest there is a large group of consumers unfamiliar with digital account opening or who have security concerns. Appropriate education could significantly move the needle.

“Omnichannel strategy is not wrong,” Nichols concludes, “but it might be overkill for a great number of banks that can’t afford the required technology.” It could be better for such institutions to concentrate on optimizing a single platform — mobile most likely — rather than spreading resources across all channels. A bank or credit union doing that, Nichols believes, might conceivably leap-frog a larger institution wrestling with a full omnichannel implementation.