Every year brings waves of speculation about “Will we still need branches in the future?” And every year brings evidence that while the future outcome is anyone’s guess — depending on how far out you go — financial institutions are making significant adjustments in their ongoing branch transformation efforts.

Each year Kiran Analytics asks more than a hundred financial institutions how they are progressing with their branch journeys and how their approaches have changed. Four key findings emerged from this year’s study.

1. The Reasons That Make Branches Important Have Shifted

In 2016, just over two out of five (43%) bankers said that branches are important to brand building and reputation. By 2019 that number climbed to 53% — an increase of 23% in just three years.

The survey found relevance of the branch is increasingly balanced between relationship growth (including account opening) at 56%, face-to-face interaction at 59% and building brand and reputation at 53%, as mentioned. This new balance is reflected in lower branch density as banks and credit unions enter new markets with well-placed, very visible branch anchors in key areas.

The importance of this new dynamic is reflected in this comment by Stephanie Gillespie, SVP, Head of Digital Technology KeyBank, as told to American Banker: “Every time a client walks into a branch, we see that as a gift. And we want to take full advantage of that interaction.” Gillespie went on to explain how the use of digital technology is helping the large regional bank to “amplify and inform human interaction with a guided conversation.”

2. Revenue Growth Now Drives Branch Optimization

From 2009 to 2017, U.S. banks consolidated about 9% of their branches. Since 2017, however, the emphasis has shifted from branch closings and consolidations (a cost reduction focus) to the addition of new, high-tech, high-touch branches or renovations of existing branches (a revenue development focus). Bank of America provides one example of this shift. Another is Regions Bank which has consolidated about 300 branches over the past five years and opened about 40 of a planned 150 new branches, according to Shawn Bradley, Executive Vice President responsible for network strategy and design.

“In 2017, just 20% thought adding branches was important, while 45% said that in 2019.”

Data from the Kiran Analytics survey supports this trends. In 2017, 67% of the bankers indicated branch consolidation was a key driver of network optimization. In 2019, only 21% said branch consolidation was the main focus. In addition, from 2017 to 2019, there was a big jump in institutions stating that “adding/acquiring new branches” was becoming more important for network optimization. In 2017, just 20% thought adding branches was important, while 45% said that in 2019.

These new and enhanced branches achieve efficiency through cashless formats, technologies such as video conferencing, kiosks and other tactics, creating optimal customer experience with greater financial return. Regions’ new and renovated “Nexus” branches, for example, are designed to emphasize customer convenience and higher value interactions.

3. Staff Reductions Are Largely Complete for Many Institutions

Only 17% of the surveyed institutions in 2019 indicated that reducing overstaffing is a top priority compared to 48% three years earlier. Most banks and credit unions addressed overstaffing by eliminating such roles as assistant branch managers and full-time tellers from many branches.

Depending on the size and location of a branch, the average number of full-time equivalent employees per branch varies between five and ten. In order to reduce branch staffs, many financial institutions have taken several steps over the past few years. These include:

- Migrating routine transactions to digital channels

- Centralizing branch activities

- Deploying smart branch technologies

- Modeling labor at the market level to provide greater efficiency.

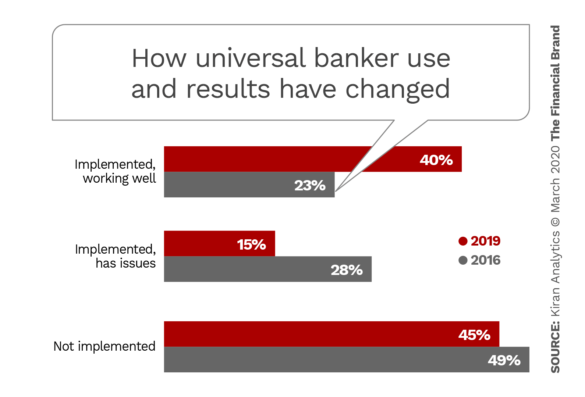

4. Successful Universal Banker Implementations Have Nearly Doubled

In a related branch trend, the survey shows that implementation of the universal banker role continued its gradual rise. 55% of institutions had deployed these types of employees in 2019, up from 51% three years earlier. This growth reflects the long-term reduction in branch traffic and shift in focus from transactions to advice.

Moving to universal bankers is not an easy transition, so it is notable that success in implementation has risen dramatically now that best practices have been identified and banks and credit unions have deployed these types of employees for several years. Another factor driving the success of these employees is the evolution of the universal banker role to include multiple levels with differing emphasis on sales versus transactions or with specialized skills such as mortgage lending or business banking.

“As we looked at the evolution of customer preferences for branch interactions, we wanted to ensure all of our bankers could meet those expectations,” states Stacy Regnier, VP of Business Transformation, Commerce Bank. “We transitioned all of our dedicated teller and financial services representative roles into universal bankers in order to do just that.”

Workforce Analytics Slowly Move Down Market

In 2017, nearly three out of five (59%) respondents indicated their bank’s commitment to using workforce analytics was high or very high. In the 2019 survey, Kiran asked bankers to rate their investments rather than their commitment. The results show that despite earlier indications of strong interest, it has not translated into substantial and consistent investment so far. Specifically:

- 20% said their institution invests substantially and consistently in analytics for workforce management.

- 48% said they are just beginning to invest in this area and the results are not yet visible.

- 32% said their bank “talks a good game” but doesn’t invest or support it.

One reason for the modest level of investment in workplace analytics overall is that the majority of financial institutions making substantial investments are the large banks. As more midsize banks, such as First Horizon, begin to implement these tools, a down-market movement may gain traction as it has with other banking technologies.

“As customer interactions with the bank were evolving, we wanted to make our branch staffing decisions based on sound analytics rather than instincts,” explains Ben Hopper, SVP of Retail Strategy for First Horizon. “Our branch transformation initiatives driven by analytics and labor modeling enabled a 9% shift in work content from idle time, operations and administrative work content to customer and community engagement.”

(Editor’s Note: Kiran Analytics has since been acquired by Verint.)