It’s doubtful many banking professionals view financial education programs as a serious marketing tool. Such initiatives often feel like little more than an obligatory community service, and thus receive perfunctory attention from the senior leadership team. And that’s typically where it ends.

However, data suggests that financial literacy is much more than just a feel-good exercise that garners an approving nod from regulators. According to a study by Raddon Research Insights, people who understand the basics of personal finance are both more engaged and more profitable for the banks and credit unions that provide them with financial education.

Consumers Get an ‘F’ for Financial Literacy

Raddon found that average the American grossly overrates their level of financial literacy. The research and consulting firm, a unit of Fiserv, fielded a survey to 1,200 participants. Almost half (44%) the respondents identified themselves as “extremely” or “very” financially literate.

But a 15-question financial literacy quiz that accompanied the survey indicated otherwise. More than half failed. Only 6% scored an “A.”

Here is one of the questions from the quiz, along with the percentages of respondents who chose each of the possible answers.

Q14: A typical emergency fund should have how many months’ worth of expenses?

(A) 3 months (28%)

(B) 6 months (57% – correct answer)

(C) 9 months (12%)

(D) Don’t know (3%)

Lynne Cornelison, author of the Raddon report, says consumers are generally more likely to identify themselves as “extremely” or “very” financially literate as they age or rise into higher income brackets. The only exception to that, she says, was with Gen X (currently people between the ages of 39 and 52), many of whom took the brunt of the Great Recession of 2008. Difficulty can be humbling.

What’s In It for Financial Institutions?

Raddon’s research found that consumers overall are most likely to turn to their primary financial institution (55%) when seeking resources for financial literacy, followed by online sources (45%), and their family and friends (39%).

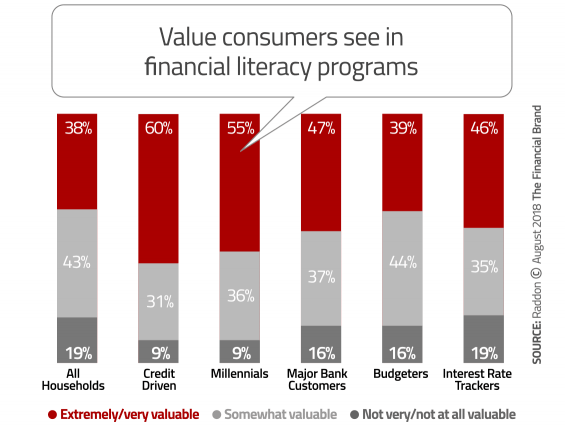

Over a third (38%) said that if their primary financial institution offered a financial education program, they would find it “extremely” or “very” valuable. Even stronger responses came from Millennials and credit-sensitive consumers.

The good news? There’s a payoff. According to Raddon, financially literate customers:

- Believe their institution hosts literacy programs for the greater good and support of the consumer, and not for the company’s own financial benefit.

- Are more open to advice and guidance from their institution.

- Exhibit higher usage in most savings/investment products.

- Show lower lobby usage levels and are less likely to occupy a bank employee’s time.

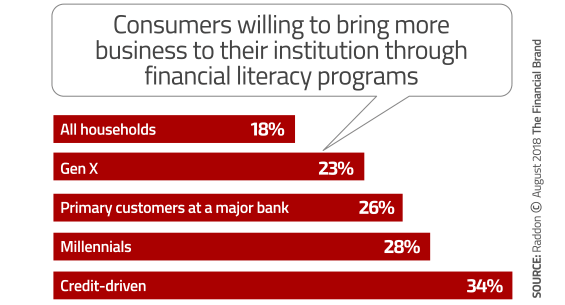

When asked if a financial literacy program would prompt them to bring more business to their primary financial institution, 18% overall said that it would.

‘Budgeters’ Can be Profitable

“The idea of being disciplined enough to live within a budget appears to be a gateway behavior to other strong financial habits,” Cornelison says.

But how many consumers actually do this? Based on the survey sample, consumers are split 50/50. The segment that budgets most often (65%) are described as “Credit Driven” in the report — an important group for financial institutions.

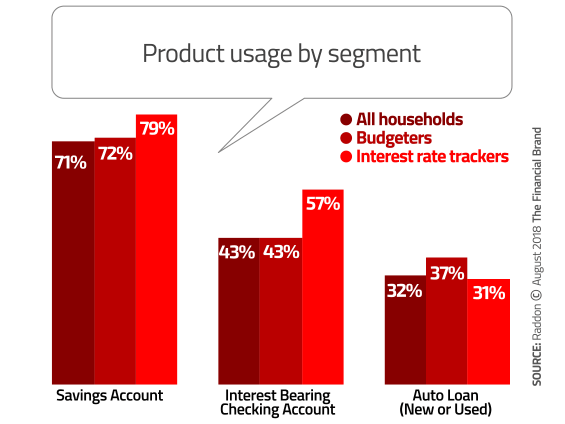

Roughly one in four respondents in Raddon’s survey said they track interest rates, with older consumers being more likely than others to do so. As the data illustrates, “rate trackers” have higher usage of depository products than “budgeters” and higher than the overall sample. For loan products, the differences are less consistent.

Raddon said that something as simple as identifying consumers who budget should help point financial marketers to consumers who are not only responsible in their spending, but also likely to use more financial products. For those who don’t budget, the firm recommends that financial institutions educate them about the benefits of budgeting. Institutions can also provide online or mobile access to help consumers monitor funds as a way to deepen a relationship and inform consumers about other products and services.

Four Action Items to Improve Financial Education Programs

The average U.S. consumer clearly has room for improvement in financial literacy, said Raddon, which represents an opportunity for financial institutions to develop more engaged customers who value their bank or credit union as a trusted resource.

Here are four specific suggestions made in the Raddon report:

1. Start your outreach early. when consumers are in the early stages of their financial life. This will not only benefit the individual but will lay the groundwork to solidify your position as their primary financial institution.

2. Offer digestible chunks. Whether offered in-person or online, multiple, smaller educational sessions will help avoid information overload. That may keep the consumer coming back for more information.

3. Prioritize the content. Focus on the three most popular topics: financial planning, retirement, and wealth management.

4. Don’t drop the ball. Follow through on what you started. As your customers adopt what they have learned, reward them for their efforts and accomplishments.