For consumers, the prospect of changing banking providers can feel overwhelming. Between direct deposits, automatic withdrawals, online/mobile banking and bill pay, the barriers to switching are high. And learning a new system for online banking, online bill pay or mobile banking can be intimidating.

That makes inertia is a powerful force in banking, with many variables affecting consumers’ decision to switch or stay put. As Dan Latimore, SVP of Celent, points out, consumers may dislike their current banking provider, but a variety of nagging questions and fears prevent them from actually pulling the trigger and making the switch.

For starters, people don’t see much difference between one institution and another. Why switch if the experience isn’t going to be any different or better with a new bank or credit union? Fair question. If the fees, rates and product features are essentially the same, why bother?

“In the absence of a markedly better alternative, inertia sets in and they remain where they are,” Latimore observes.

There’s also the issue of familiarity. Consumers believe that managing their bank accounts are a tedious and complex affair. After they’ve taken the time to learn the ropes at Bank X, do they really want to abandon their investment and switch to Bank Y?

“Consumers are familiar with the foibles of their current bank, and while they may be unhappy with it, they at least know what to do and what to avoid,” says Latimore. “They don’t know the ins and outs of the alternative banking providers, and don’t think that they’ll be much better off if they switch.”

If inertia is a problem in the banking industry and consumers are disinclined to switch, financial institutions are largely to blame. They have done everything possible to make it a pain in the ass to leave, a strategy they euphemistically call “stickiness.” Every bank and credit union strives to make it easy to open a new account, but almost no one makes it easy to close an account. It’s like a venus fly trap — once you’re in, you’re stuck.

“There’s been a longstanding hypothesis that consumers stay with their current banking provider because it’s too inconvenient to switch,” says Latimore. “A related hypothesis is that if it were only easier to switch, more customers would do it. Both hypotheses are wrong.”

To support his assertion, Latimore points to the UK banking industry, where financial institutions are required to make switching easy. Thanks to a government mandate, banks have been forced to complete the switching process within a seven day window. Technically speaking, the initiative has been a success; nearly every time a banking customer switches providers, it takes seven days or less. Consumers in the UK are largely familiar with this bank switching program, and studies show that they believe it is now significantly easier to move from one provider to another. And yet switching levels have remained basically flat in the UK.

Does that mean you shouldn’t aspire to make the switching process as simple and straightforward as possible? No. Conversely, it doesn’t mean you should make it any more difficult for your existing customers to leave.

“Stop spending so much time on making your offerings sticky,” recommends Latimore. “They’re likely already sticky enough and your efforts could be better spent elsewhere, like delighting your customers.”

Remember, there are always two sides to the “switching” coin. Yes, you are trying to woo new customers to your institution, but at the same time, you are also trying to keep your own customers from abandoning ship. Instead of making your checking products more sticky to prevent attrition, you should focus on keeping them happy. It’s a classic carrot vs. stick(y) situation.

What Drives Consumers to Switch?

Consumers either switch banking providers because (1) they have to, or (2) they want to. In the first case, a consumer usually relocates from one area to another where their current provider doesn’t have a presence. But beyond making your digital/remote service delivery channels as robust as possible, there isn’t much you can do about movers — if someone feels they need a physical branch in Philadelphia and you’re based in San Diego, you don’t really have any options.

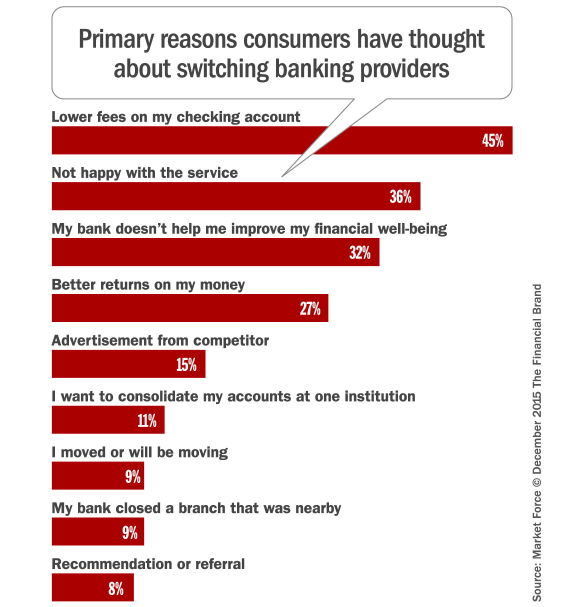

Financial marketers need to concentrate on those consumers who voluntarily decide to switch. According to a study from Market Force, one in five banking customers are not satisfied with their relationship with their primary bank. Their research found that 12% of all banking customers are considering switching banking providers within the next six months. The primary reasons cited centered on both dissatisfaction with fees and the service provided by the institution.

“Consumers are tired of feeling like a number,” says Jim Dellavilla, Chief Client Officer at Catalyst. “They are fed up with paying fees on their checking accounts and gaining little to no interest on their money. They want access to consumer-friendly technology and are looking to be rewarded for their business.”

What really grinds consumers more than anything is poor service. In a study by Credio, dissatisfaction with customer service was found to have the strongest correlation with a customer’s willingness to switch banks. With an inverse correlation of -0.486 between customer service satisfaction and NPS, customer service has a greater influence on a customer’s departure than any other metric they evaluated.

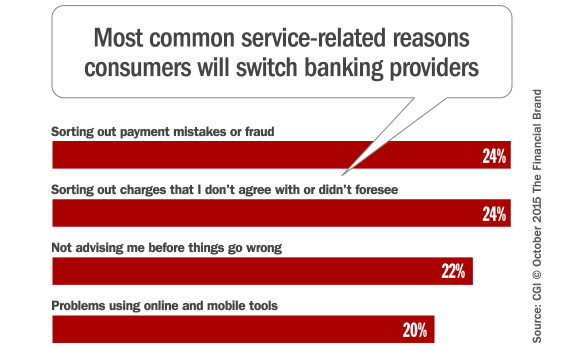

Of the consumers who switched to another provider due to poor service, Accenture says that more than 80% said they could have been retained, mainly if their issue had been resolved on their first contact with the bank.

Make Switching Easy

In a study from Kasasa, six in 10 U.S. adults who have never switched banks (61%) believe switching banks would be at least somewhat difficult, but among those who have actually switched, 8 in 10 (81%) say it wasn’t difficult at all. Just 19% of Americans who have switched banks say it was at least somewhat difficult.

Millennials, in particular, overestimate the difficulty of switching banks. Among those ages 18 to 34 who have not switched banks, 69% believe it is at least somewhat difficult to switch banks, compared to just 54% of Americans ages 55 and up who have not switched banks.

Even though the UK’s mandate to make bank switching easier hasn’t produced a huge spike in switching activity, that doesn’t mean you shouldn’t do everything possible to remove friction and eliminate obstacles in the process.

“One of the biggest pain points for consumers switching banks is recreating all of the payees in a new online bill pay system,” observes Dellavilla at Catalyst. “Most banks do not allow consumers to export bill pay data such as payee addresses or account numbers in an attempt to make it more difficult to switch. But automated switching platforms such as Deluxe’s SwitchAgent and ClickSWITCH are on the path to making this process more seamless for consumers.”

Dellavilla says marketing messages pointed at prospective switchers must reassure them that it can be both painless and straightforward.

“Provide peace of mind by letting prospective customers know that you will be there to make sure that nothing falls through the cracks,” Dellavilla says.

In a white paper on switching in the banking industry, Catalyst provides the following ideas and recommendations to improve the process:

- Provide a step-by-step guide for getting a debit card, ordering checks, setting up online banking and accessing mobile banking

- Create a quick reference to the bank routing number and consumer’s account number for direct deposit and automatic withdrawals.

- Make demos for online banking, online bill pay and mobile banking readily available.

- Offer a dedicated customer service representatives who specialize in switching accounts and are available through online chat or telephone.

- Create a new role for a “Switch Concierge” in local bank branches who can sit down with consumers while they set up the new accounts.

- Consider offering a “smooth switching guarantee” to back up the claims that switching can be painless.

In your marketing materials for checking account products (e.g., your website), you can include testimonials from happy customers and include comments from those who have already made the switch.

“People look for firsthand experiences, reviews and feedback from friends, family, or community members when considering a switch,” adds Dellavilla. “They want to know how satisfied current customers are, and what there is to like about doing business with your institution. If possible, try to foster personal connections with prospective consumers to build trust during this time.”