Routine banking transactions are migrating increasingly to digital channels as COVID-19 restrictions that led to a boost in remote workers changed the landscape of where and how people bank. As branch foot traffic continues to decline, the industry is again talking about the “hub & spoke” concept for branch networks.

While much has been written about a coming spike in branch closures, it’s yet to occur. Meanwhile, many banks and credit unions have been reconsidering branch strategy and the “hub & spoke” model has come up as a way to slim existing branch networks as well as a way to economically establish a viable presence in entirely new markets.

Key Question:

Is there something to this strategy? Or is the term just becoming a temporarily popular buzz-phrase?

In a long career in branch siting, I’ve studied many different branch network models in hundreds of markets across the country, as well as overseas. Some models work better overall, and others work best in select situations. The key is to know when and where to deploy any approach.

New Market Forays Benefit From 6%+ Critical Mass

Unless you are an e-bank, when you enter a new market where you have a limited pre-existing customer base, you need to focus on branch building. The branch is the most effective way to attract new consumers — but remember it may take ten years for that branch to reach maturity. During these early growth years, your focus should be on building a branch network — a connected set of branches that cover your target segments with minimum overlap.

I’ve written before about the “6% branch share rule.” It states that you double the probability of above-normal deposit growth if you have at least a 6% branch share in a market. Building branch density is an important component of maximizing your customer base growth.

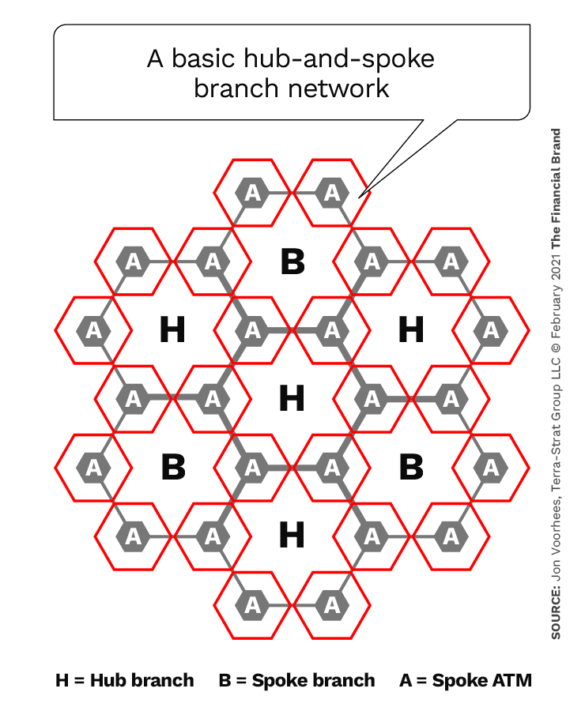

Some large financial institutions have discussed entering new markets through the construction of a “thin” branch network. Typically, these types of networks offer a version of the “hub & spoke” concept, with a limited number of branches spread across the market at some of the busiest retail zones. Those branches are complemented with a few remote ATMs interspersed at secondary or smaller retail locations.

Bottom Line:

So far, I haven’t seen thin networks deliver consistent success.

One challenge for those trying this approach is that for remote ATM deployment to succeed an institution needs to have a large existing base that will drive transaction volumes. Surcharge revenue won’t cover the costs of ATM deployment anymore, because ATMs are so ubiquitous today. Remote ATMs play a role in a successful branch network, but only when you have the base to make sufficient use of them.

Read More: Trimming Branch Networks? Many Financial Institutions Find It Tough

Hub & Spoke Models Can Work Well (In Existing Markets)

Hub & spoke models have been around in many industries for years. In fact, these models follow classic location theory, which says that consumers will travel longer distances to do things that are needed infrequently. In other words, the more frequent the need for a specific transaction, the closer consumers want to be to a site that can deliver it.

Reilly’s Law of Retail Gravitation says that the greater the attractiveness of the retail site, the larger its trade area or draw will be.

While Reilly’s law defined attractiveness as sheer retail size — historically that’s why malls developed — attractiveness can be defined by other measures, such as the number or variety of services provided at a specific site. For retail banking, here is how you should think about the hierarchy of functionality:

- At the lowest level, you have limited-service cash-dispensing remote ATMs. They provide limited functionality but are needed fairly frequently.

- One level up would be deposit-taking remote ATM sites. These machines can handle both withdrawals and deposits, so from a consumer’s perspective, they offer greater value. If the machines offer remote interactive teller access (ITMs), that’s another bump up in value. LINK

- The next level would be an instore or supermarket branch. These sites typically offer basic teller services, an ATM, and one service representative to handle account issues or new accounts, but with limited privacy. (Note that these are notoriously not profit centers.)

- Then, basic traditional branches will generally offer more capabilities and staff, making it easier to get things done. If those branch sites have drive-up lanes, then they are more valuable.

- Many branches add more value by adding specialists, such as small business bankers, mortgage representatives or investment advisors. These sites are often referred to as “flagship” branches.

Read More: Rethinking Branch Networks Without Killing Sales or Growth

Different Types Of Sites Offer Different Levels Of Attraction

When looked at from the consumer’s perspective, these format differences offer different levels of site attractiveness. Similarly, you can differentiate locations too.

- A standalone building removed from other retailing has limited draw or attractiveness.

- A strip center with a collection of small retailers offers more choices for “one-stop” shopping.

- A commercial corridor of a collection of strip centers offers even more choices to consumers.

- Small shopping centers with a larger anchor store (typically a grocery) are more attractive. The larger the center the better.

- Big box centers tend to be few and far between, so their draws are larger.

- At the top end of this hierarchy are malls that offer a wide variety of goods. For banking, though, malls present some challenges as you don’t want to be inside the mall because it limits visibility and accessibility — not to mention the beating many malls are taking in general.

Combining both location and site attributes, high-level “hubs” would be located at big draw locations and offer the broadest level of services. “Spokes” would be more prevalent and could be a combination of different formats depending upon each locality’s specific needs. You would need to have enough “hubs” to still cover the market, recognizing they have larger trade areas than the lower order “spoke” sites. One way to think of “spokes” is as infill sites in between the “hubs.”

Key Insight:

These “hub & spoke” retail models require a large base, as they are most effective when deployed to maintain and grow a market. They are less effective for new market entry for the simple fact that you will be spreading a limited number of interactions across multiple sites.

If you have an existing market with deep penetration, then this model can be useful to scale back branches and replace them with lower order remote ATM sites. Based on my own experience, I still maintain that when your institution is new to a market, your best bet is to build a branch network that reaches at least 6% branch share. This approach increases the probability of faster and greater success in building your base. In such cases hub & spoke may not provide sufficient density.

Jon Voorhees is Director of Distribution Strategy and Business Development at TerraStrat Group LLC. Previously Jon led retail distribution strategy teams at multiple large banks including Bank of America, where he also led the retail distribution execution team. Jon can be reached at [email protected]