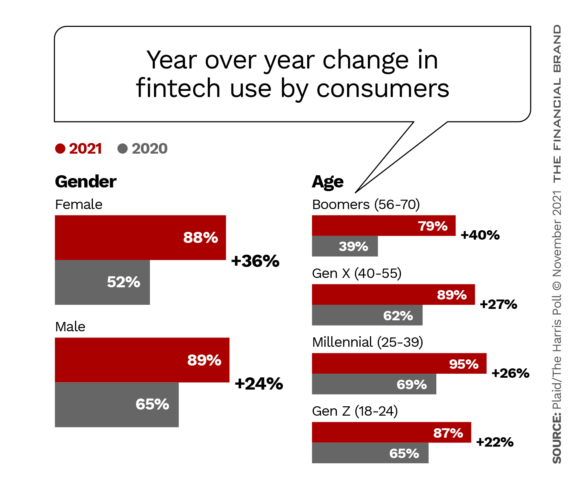

Fintech is no longer just about money and banking — it has quickly become a part of every aspect of life. Between 2020 and 2021, the portion of U.S. consumers using fintech grew from 58% to 88%, according to a report by Plaid and The Harris Poll.

That’s striking in itself, but an even more remarkable finding is that while consumers still hold greater trust in traditional financial institutions compared to nontraditional competitors, the gap is not that great. The report, based on a survey of 2,000 U.S. adult consumers, found that 77% of the overall population trust financial institutions with their financial information, compared with 69% for both tech companies and retailers and 63% for fintech companies.

In fact, Millennial consumers now have an essentially equal level of trust in nonbank financial providers as they do in traditional finance institutions. Here’s how it breaks down: retailers (80%), traditional financial institutions (79%), fintechs (75%). With Gen Z, fintechs actually come in higher than banks (66% to 63%).

Key Point:

Three quarters of U.S. consumers (76%) say the more they use digital tools to manage their money the more they trust them.

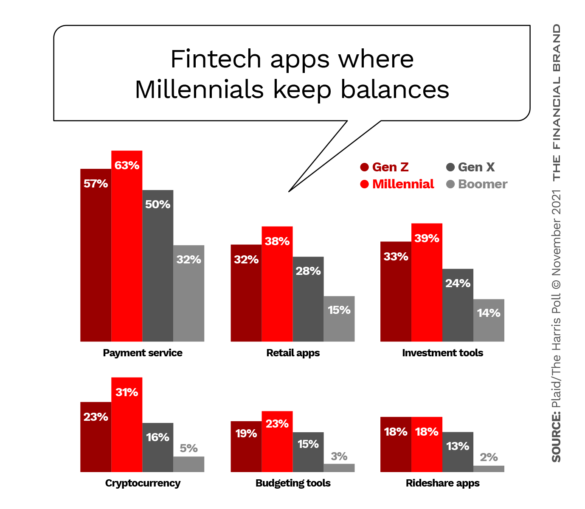

This increased trust manifests itself in a willingness to store balances — uninsured for the most part — in fintech applications such as Venmo, Starbucks, Robinhood, Coinbase, Digit, and Uber. Millennials are the most willing to do this.

As mobile apps and payments expand, fintech now has moved beyond traditional banking capabilities to everyday parts of life. Things like mobile ordering, grocery delivery, ride hailing, and P2P payments have all acclimated consumers to digital and automated finance.

Also notable is that while people have more fintech apps on their phones, they use fewer of them on a daily basis. The report attributes this partly to the fact that consumers are moving more from experimentation to longer-term engagement. Nearly 70% of respondents now say they have a routine around using technology to manage their money.

Upward Trajectory:

The percentage of Americans who use fintech daily rose 30% in one year from 37% in 2020 to 48% in 2021.

The shift in trust has been impacted by the pandemic. A physical location has become less important and changed the equation for gaining trust, observes Jim Marous, CEO of the Digital Banking Report and Co-Publisher of The Financial Brand. With increased digitization, the 4 Ps of marketing — product, price, place, promotion — are increasingly being replaced by the 4 Es — experience, every place, exchange, evangelism. “Combined, these components are shifting the criteria for gaining trust,” Marous maintains.

Read More: Why Banking Needs to Do More Than Talk About Financial Inclusion

Consumer Behaviors and Attitudes Change

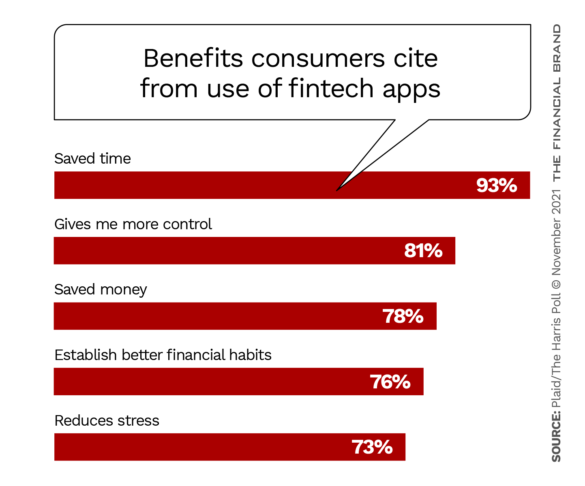

Many of the new behaviors consumers adopted in 2020 — changing how they live, work, shop, and bank — have become permanent. Of survey respondents who used fintech in the past year, more than 80% said they’ll retain these behaviors moving forward. Many have discovered fintech can improve their financial well-being, giving them the confidence, control and financial habits to make better decisions about their money.

Nearly half of users said fintech had a positive impact on their financial understanding, while others said it helped them progress towards their financial goals or improve their financial management. Survey respondents said they used fintech to address challenges like sticking to a budget, saving more and investing. Digital savings and investing tools were popular apps, with seven in ten consumers saying the more they use fintech, the more confident they feel about their finances.

As consumers gravitate more towards digital finance experiences, they’re also placing a greater value on connectivity. 80% of respondents said it is important to connect their bank account to the apps they want, and 76% said the ability to connect is a top consideration when choosing a bank.

Read More: How Neobanks Are Catering to the Youngest Generation of Consumers

Fintech Makes Finance More Inclusive

While some fintech companies like to make grandiose claims of how they’re fostering inclusivity and social benefits, there’s growing validity to the idea. The Plaid/Harris Poll report found fintech usage is now even surpassing traditional banking usage for many underserved communities.

For example, the number of Hispanic and Black respondents saying they used technology to manage their finances was greater than those who reported having bank accounts. In fact, fintech usage rose dramatically in 2021 across every demographic.

One notable social impact of fintech’s adoption across all demographics is that it’s breaking down the taboo of talking about money. Seven in ten respondents say fintech has made finances more social and enjoyable to talk about. These trends are especially more pronounced among younger people and minority populations who now talk with friends about things like investing.

Robo-App Impact:

Younger consumers using apps like Robinhood and Webull develop expectations for simple interfaces and the ability to invest with less money.

In addition, half of those that used fintech said they did because a friend or family member recommended it. “As fintech reaches mass adoption, people experience it like other mass-marketing consumer goods, sufficiently relevant to ask friends and family for advice and guidance, while still consulting experts as needed,” says the report. “The more people are able to talk about their finances with their social circles, the better they can understand their own needs and find the right tools to address them.”

Robo-investing apps, built by non-bank fintech firms, made it easy for users to invest with a small up-front amount, observes Mark Allen, Senior Vice President at Access Softek. And while many banks and credit unions haven’t viewed them as competitors, robo-advisors have proven that strong interface and simple to use services are attractive to consumers.

Bigger Changes Ahead

Growth in fintech that many expected to take another ten years has now happened in only two. Consumers are going through big changes in how, when and where they interact with their money.

The Plaid report summarizes several findings about what consumers want in their financial services:

- Consumers want apps and services that work when and how they want and that make it easier to manage money.

- They expect interoperability and want apps and services to provide connected experiences, regardless of the providers.

- People value services that not only help them save money but achieve better financial outcomes.

- They expect impact to increase with use, benefiting more from technology the more they use it.

These evolving consumer expectations will continue to fuel innovation across every segment of finance. “With the current pace of adoption and innovation, we anticipate a fully digital financial system within this decade,” the report predicts.