At a time when the world was focused on health concerns, consumers also became more vocal in their belief that corporations must be more active in environmental and societal issues. The financial services industry is at the epicenter of this transformation, being asked to commit to a purpose beyond profitability, supporting diversity, equity and inclusion strategies.

The question becomes: To what extent are financial institutions devoting resources to promote financial inclusion – providing access to affordable products and services for a much broader marketplace than covered in the past? A study by Deloitte found progress is being made, while clearly signalling that much work still needs to be done. The study surveyed 300 senior financial institutions executives in the United States who are connected to or responsible for financial inclusion initiatives.

Banks State They Are Committed to Financial Inclusion

According to the Deloitte research, more than three in four respondents consider financial inclusion to be a core pillar of their overall corporate social purpose strategy, with almost the same percentage of organizations stating they have a clear vision and action plan to further their financial inclusion agenda.

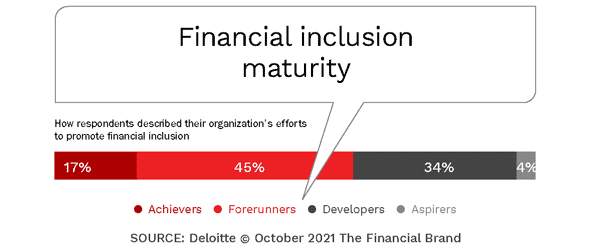

Deloitte categorized financial institutions into four broad categories based on their financial inclusion maturity:

- Aspirers: Have planned financial inclusion initiatives but have not yet initiated any activities.

- Developers: Are in the initial phases of launching financial inclusion strategies or have launched them and are gaining traction.

- Forerunners: Have mature financial inclusion strategies and activities in place and are seeing progress.

- Achievers: Have accomplished their financial inclusion goals and what they set out to do.

As shown below, 96% of financial institutions indicated they have some level of financial inclusion initiative underway, with 17% stating they have achieved what they set out to accomplish (‘achiever’ status). Another 45% self-assessed themselves to be ‘forerunners’.

It is important to note that nine in ten respondents did not consider financial inclusion to be independent of good financial results. In fact, all of the respondents from Aspirer organizations put a high value on profitability while indicating that cost and technology are top challenges in prioritizing financial inclusion. Another challenge is that many organizations said they lack a singular point of ownership of financial inclusion strategies.

Challenges to Financial Inclusion:

Financial institutions cited financial cost concerns and technology constraints as the most common challenges to prioritizing financial inclusion.

Read More: The Increasing Need for Talent, Inclusion and Diversity in Banking

Financial Inclusion Begins With Employees

Numerous studies have found that an employee that is dealing with financial stress is not as productive at work. Offering employees ways to improve financial well-being can also boost employee engagement and morale across the organization.

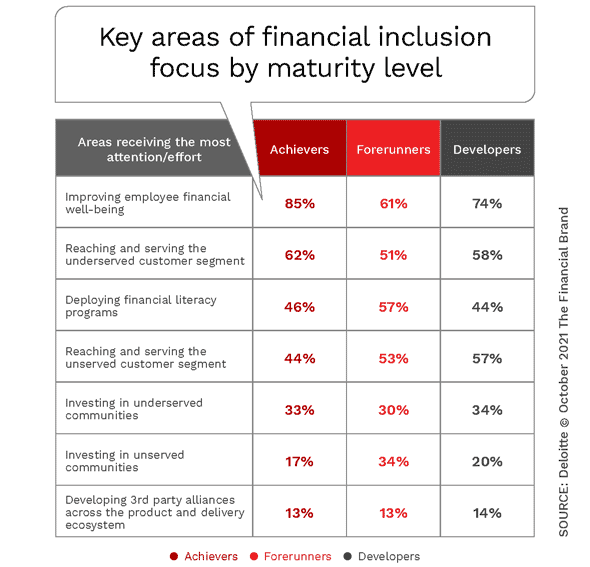

With this in mind, financial institutions at all levels of financial inclusion maturity place the greatest emphasis on improving the financial well-being of employees. Across all levels of maturity, reaching the currently underserved customer segments ranked second (55%) with serving the unserved customer segment being third (53%). Building financial literacy programs was also a major area of focus for financial institutions at all maturity levels.

Read More: Financial Marketers Must Align Purpose, Mission & Values Now

Big Gap Between Underbanked Needs and Financial Offerings

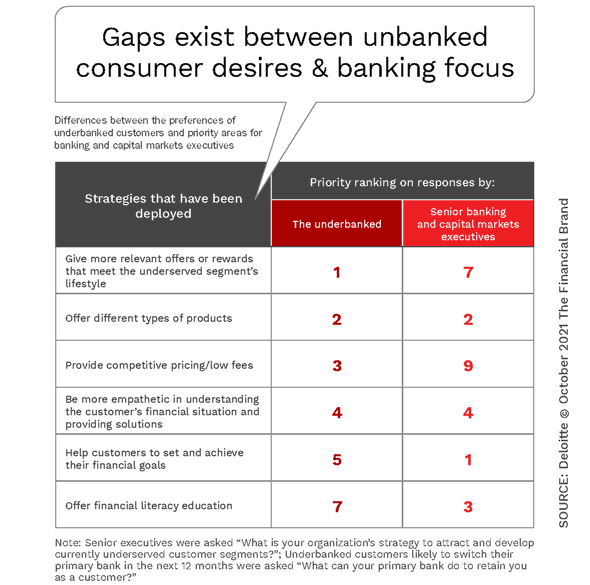

When financial institutions were asked about their strategic priorities around servicing the underbanked consumer segment, they ranked helping customers set and achieve financial goals, being more empathetic to customers’ financial situations, and offering financial literacy resources as the top three areas of focus. The problem is that the underbanked consumer has a significantly different set of priorities.

The strategies that most financial institutions are focusing on are far more aspirational than what underbanked consumers revealed to Deloitte. The priorities of the underbanked consumer were the availability of different types of products, more relevant lifestyle-related rewards and offers and competitive pricing or low fees.

Data and Applied Analytics Drives Inclusion

It is very difficult to reach historically underserved segments of the marketplace using legacy products, processes and technologies. Not only will the serving of these markets be highly inefficient, but also ineffective since needs and solutions will remain unaligned.

Progressive organizations like WeBank, Alibaba and PingAn in China all leverage deeper data sources, technologies like artificial intelligence (AI) and machine learning (ML) and highly automated back-office operations to serve the previously unbanked population … at a profit. These are the same pillars of success implemented by many fintech organizations, especially in the offering of credit services.

According to Deloitte, “Financial institutions can train models to focus on more equitable, alternative data to help eliminate bias. They can use payment history, such as rent, cell phone and utilities payments, to get an alternative view of consumer financial behavior.”

Data, Technology and Inclusion:

Nearly 50% of financial institutions said they plan to leverage technology and business model innovation to scale financial inclusion efforts over the next 6 to 12 months.

Leaders Must Place Purpose on Par with Profits

There is no argument that the banking industry is well positioned to support much greater financial inclusion than it has in the past. Not only do banks and credit unions have the financial resources to support underbanked and unbanked communities, but they also have access to the data, technology, and networks to deliver financial inclusion solutions at scale… and at a profit.

While more than 60% of responders to the Deloitte survey categorized their organizations as either ‘Forerunners’ or ‘Achievers’, there is still a significant gap between what is being delivered to these markets and what the unserved and underserved customers say they want. There is also a lack of clear evidence that organizations are ‘moving the needle’ quickly or broadly enough. It is commendable that organizations are focusing on the financial well-being of employees, but the focus must now move outside the organization.

More than broad statements in support of financial inclusion within shareholder reports, there is a need to change legacy culture and strategies that currently place profits before purpose. This requires leadership that will embrace change and build partnerships with providers of alternative distribution channels and services used by the targeted segments.

Until leadership in financial institutions goes beyond ranking themselves as better than their peers, there is a need to deliver on the promises made and the needs of the markets being left behind.