Young Americans Have Never Been Wealthier – Or More Stressed. Can Banks Help?

Median household wealth for Americans aged 25 to 39 surged to record levels after the pandemic, thanks to both generous fiscal policies and asset inflation. Yet a new Treasury Department paints a dire picture, arguing that the benefits of record wealth are being undercut by mounting debt, skyrocketing housing costs and personal challenges ranging from mental health deterioration to social isolation.

By David Evans, Chief Content Officer at The Financial Brand

Simple Subscribe

Subscribe Now!

The report: How does the Well-Being of Young Adults Compare to Their Parents’?

Source: U.S. Department of the Treasury

Why we picked this report: Economic signals and consumer sentiment, particularly among younger Americans, have been moving in opposite directions. Does the gap create growth opportunities, in terms of new products and services, for banks?

Executive Summary

Young adults today face markedly different economic challenges compared to their parents’ generation, with significant implications for retail banking. The good news is that some indicators like women’s earnings and recent household wealth have improved. But many young Americans still struggle with financial fragility, declining labor force participation, and mounting costs. The landscape is shaped by soaring housing and childcare expenses, unprecedented student debt levels, and changing household formation patterns.

These shifts create both challenges and opportunities for financial institutions to adapt their products and services to better serve this demographic’s evolving needs.

Key Takeaways

- Young adults’ household formation patterns have shifted dramatically, with increased rates of living with parents (rising from 12% to 16% for ages 25-34) and delayed marriage, creating new demands for flexible banking products and modified lending criteria.

- Student loan debt has grown nine-fold since 1989, with 40% of young adults now holding student debt compared to 15% in 1989, highlighting a need for specialized debt management and refinancing solutions.

- Housing costs have nearly doubled relative to income since 1990, while childcare and healthcare expenses have risen sharply, suggesting opportunities for innovative savings and lending products.

What we liked about this report: It correctly identifies important discontinuities between raw economic data and overall sentiment for a demographic cohort critical to the U.S. economy in coming years.

What we didn’t: It’s inherently a political document, highlighting actions taken by the outgoing Biden-Harris administration and not-so-subtly carrying water for the administration’s focus on student loan debt. The report also awkwardly intermingles economic data with social and cultural issues, at one point presenting a graph of forecast increases in global surface temperatures side by side with one projecting total federal debt held by the public.

The Changing Financial Landscape for Young Adults

Economic mobility and labor market shifts: Today’s young adults face a fundamentally altered economic landscape compared to their parents’ generation. The traditional path to middle-class financial stability has become more complex, as labor force participation among young men has declined to less than 90%. This decline is particularly pronounced among men without college degrees, who have seen their real earnings drop by nearly 10% since 1990.

There are bright spots, notably in women’s earnings. Women with bachelor’s degrees, who now represent 47% of young women workers, have experienced real wage growth of 15.1% since 1990, reflecting significant progress in workplace equity and access to higher-paying positions. These divergent trends between male and female earnings, coupled with broader changes in workforce participation, are reshaping household economics and financial decision-making patterns.

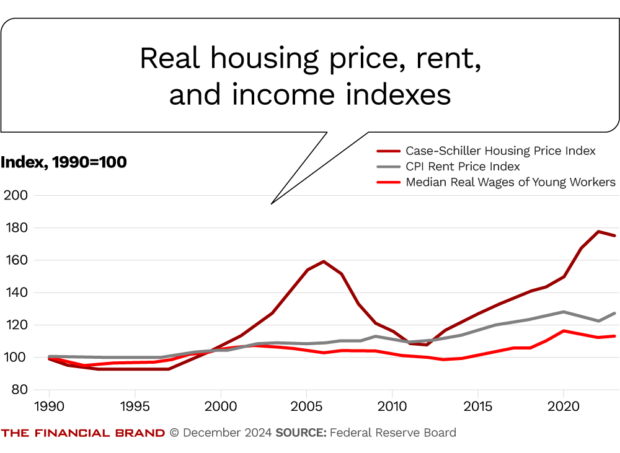

Housing affordability and family formation: The cost structures facing young adults have shifted dramatically, with housing affordability emerging as a critical challenge. Median home prices have nearly doubled in real terms since 1990, while real wages have shown only modest growth. The impact extends beyond housing into family formation decisions, with marriage rates declining substantially and fertility rates dropping to historic lows.

The Story of the Data:

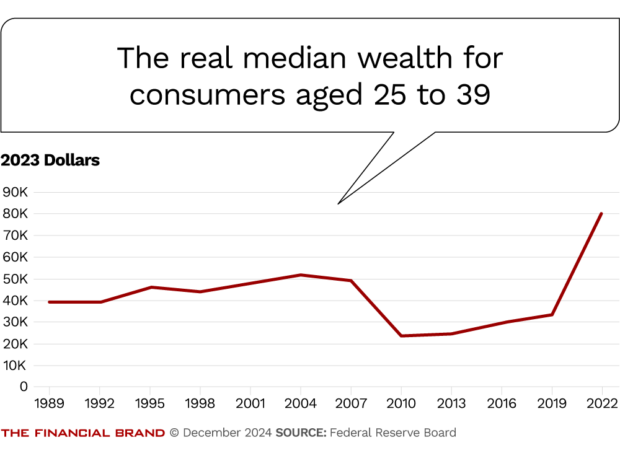

Real median wealth for young Americans surged by 140% in 2022, reaching historic highs, although this masks significant balance sheet challenges including doubled non-housing debt levels since 1989.

Adding to these pressures, childcare costs have risen sharply, often consuming a significant portion of young families’ income. More than 90% of Americans now live in counties where median rents and house prices have grown faster than median household incomes since 2000, creating a widespread affordability crisis that particularly affects young adults trying to establish independent households.

Debt burden and wealth accumulation: The surge in median wealth masks significant underlying challenges. Student loan debt has become particularly burdensome, growing nine-fold since 1989 and now accounting for more than half of non-housing debt for young adults.

The proportion of young adults carrying student debt has increased dramatically, from 15% in 1989 to 40% in 2022. This debt burden has far-reaching implications, often delaying household formation, reducing homeownership rates, and discouraging pursuit of public service careers.

Notably, about 42% of student loan debt holders between 25 and 39 years old do not have a bachelor’s degree, suggesting that many have taken on significant debt without securing the higher earnings typically associated with college completion.

Mental health and future uncertainty: Young adults today face unprecedented levels of uncertainty about their financial futures, compounded by growing concerns about fiscal sustainability. Mental health challenges have increased significantly, with the share of adults ages 18-25 reporting poor mental health doubling between 1993 and 2020.

Social isolation has also risen, with young adults spending approximately one hour less per day on social engagement compared to 2003. A 2019 survey found that 48% of Americans “always or sometimes felt isolated from others,” with younger respondents reporting the highest levels of loneliness. These mental health challenges can significantly impact financial decision-making, risk tolerance, and long-term planning abilities.

The outlook is further complicated by mounting concerns about climate change impacts and the sustainability of social safety net programs, with Social Security and Medicare trust funds projected to face depletion in 2033 and 2036 respectively.

Demographic and technology shifts: The aging of the U.S. population has created additional challenges for young adults, who now compete for housing and jobs with a larger cohort of older, more established workers and homeowners. In 1990, households headed by 25–44-year-olds represented 44% of all households; by 2020, this share had shrunk to 32%. This demographic shift has contributed to housing market pressures and may be limiting career advancement opportunities for younger workers.

Simultaneously, technological changes and globalization have transformed the job market, reducing opportunities for workers without college degrees while creating new pathways in the digital economy. These structural changes require young adults to be more adaptable and financially resilient than previous generations, often necessitating multiple career changes and ongoing skill development throughout their working lives.

Dig deeper into generational banking trends: