Wealth Management Is Transforming. Which Banks and Challengers Will Come Out on Top?

With an imminent, massive wealth transfer expected over the next twenty years, banks and challengers must position themselves to meet the needs of a new breed of customer. Data from digital banking research platform FinTech Insights show the scope of the work U.S. banks and challengers must do to meet those needs.

By Alexandros Argyriou, CEO of Fintech Insights

Simple Subscribe

Subscribe Now!

$84 trillion.

That’s how much wealth will change hands over the next twenty years, according to consulting firm Cerulli Associates — about four times the U.S.’s gross domestic product.

And $72 trillion of it will go to Millennials and Gen Zers, 74% of whom expect wealth managers to be at least as good at digital as Amazon, Apple, and Google, according to Deloitte.

But it’s not just what The New York Times has called “the greatest wealth transfer in history” that’s reshaping wealth management.

The proliferation of robo-advisors — algorithm-based investing apps like Acorns and Robinhood — has made the sector accessible to customers who don’t fit the traditional “ultra-rich” profile, thanks to simpler eligibility requirements and user-friendly app interfaces.

Needless to say, shifting demographics are also bringing about a change in what customers want — indeed, expect — from wealth management services. And a smooth, frictionless, digital-first experience is top of the list.

So which U.S. based banks and challengers are best positioned to serve this new breed of customer? And which ones are lagging behind?

We used our digital banking research platform FinTech Insights to explore and evaluate the current state of the market.

A Growing Market With Limited Options

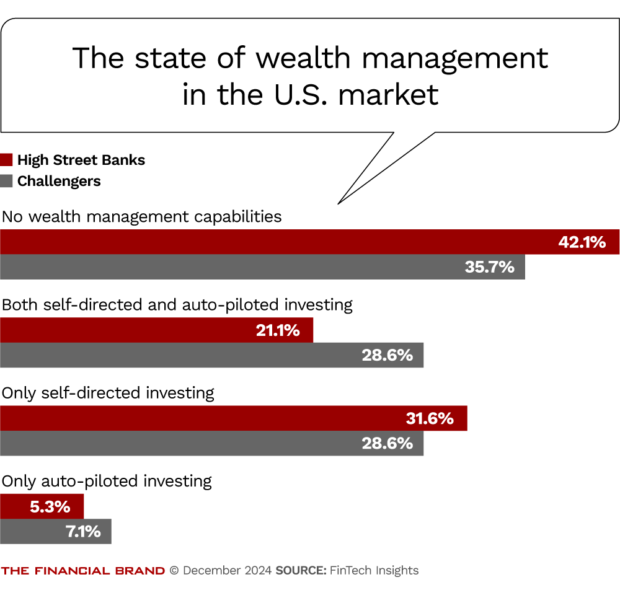

A look at our sample — 19 incumbent banks with a national presence, and 28 challengers — revealed that when it comes to digital wealth management services, consumers are far from being spoiled for choice.

Overall, 38% of the firms in our sample don’t offer any investing capabilities. Out of the 62% that do, the majority only offer self-directed investing. Firms that support robo-investing are in the minority.

Perhaps unsurprisingly, incumbents lag well behind challengers.

Forty-two percent of incumbents — almost half our sample — didn’t have investing capabilities, compared to 35.7% of challengers. Of the 11 incumbents with wealth management capabilities, only 4 offer both self-directed and robo-investing (21.1%). Six offer only self-directed investing (31.6%), while 1 offers only robo-investing (5.3%).

By contrast, 18 out of the 28 challengers in our sample (64.3%) have some form of wealth management functionality, with 8 offering both self-directed and robo-investing (28.6%).

A further 8 challengers (28.6%) offer only self-directed investing, while 2 (7%) offer robo-investing only.

Learn more:

- Don’t Wait to Develop Wealth Management and Investor Initiatives

- The Future of Financial Wellness: The Evolution of the Debbie App

- The Great Wealth Transfer: How Banks Win the Next Generation of Business Owners

Robo-investing: Who Does It Best?

The typical customer seeking out robo-advice is very different from the high-net-worth individual incumbent banks and other legacy wealth management firms usually target.

Not only are they digitally-savvy and increasingly well-informed — thanks to the proliferation of online forums and other educational resources — they also tend to be on average salaries, which means they can’t afford the minimum investments traditional firms usually require.

With this in mind, we evaluated the firms in our sample that have robo-investing capabilities to find out how easy they make the process of opening a robo-investing account, based on the following two criteria:

How long does it take to open a robo-investing portfolio? We set the benchmark for ease at 2 minutes or less

What’s the minimum investment amount required?

Out of the 15 firms in our sample with robo-investing capabilities, 7 — around 46.7% — make it possible for a customer to open an account in two minutes or less: Acorns, Albert, Citizens Bank, e-trade, Moneylion, Revolut, and SoFi.

The speed of onboarding gives these firms a significant advantage over their competitors.

In a 2022 Signicat survey, 68% of respondents reported abandoning a financial services product application because it took too long. While these numbers refer to European customers, it’s likely there are similar levels of dissatisfaction in the U.S., especially taking into account that, according to Censuswide, 87% of businesses surveyed reported abandoning an application.

But three of these firms — Citizens Bank, e-trade, and Revolut — fall at the second hurdle, by requiring a minimum investment of between $100 and $2,000. By contrast, Acorns, Albert, and SoFi don’t have a minimum investment threshold, while Moneylion has a very accessible threshold of $1.

Out of the firms that have a setup which takes longer than two minutes, Betterment is the only one with an accessible minimum threshold, as it doesn’t have one. So, if it were to simplify its account-opening procedure, it could gain a considerable competitive advantage.

Wealth management is changing. Are you ready to catch the wave?

With a compound annual growth rate of 6.43% and total assets under management expected to hit $1.9 trillion by 2028, according to Statista, robo-advising is one of the most exciting growth opportunities — if not the most exciting — in wealth management.

But the great wealth transfer we’ll see over the next 20 years means change is also coming to the high-net-worth space. According to consultants Cerulli Associates, 87% of those who inherit wealth fire their advisor. And the quality of digital capabilities will have a lot of weight on their decision about who to work with next.

As things stand, our data shows that few challengers — and even fewer incumbents — are in a position to make the most of this opportunity.

To put it more bluntly, U.S. banks and challengers have work to do. And those who can get that work done the fastest stand to gain outsize rewards.