Target Unique Consumer Segments With Specific Checking Products

Simple Subscribe

Subscribe Now!

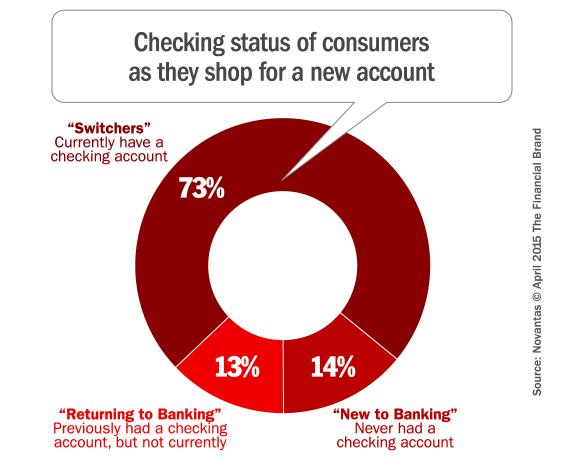

In March 2015, nearly a third of shoppers looking for a new checking provider on FindABetterBank indicated that they don’t currently have checking accounts. It’s easy to assume these might be Millennials shopping for their first checking account. But actually, slightly more than half this group indicated that they’ve never had a checking account. The rest said they had a checking account at one point, but don’t currently.

Consumers that currently have checking accounts (i.e., “Switchers”) have different functional requirements and behaviors than those who are “new-to-banking” and those who are “returning-to-banking.” As a result, different types of checking products appeal to each group.

New-To-Banking. 53% indicate that their lowest daily balance will be under $500, and 52% will have a direct deposit. They’re 63% more likely than Switchers to want a debit reward card or those that are returning-to-banking. The best products for these shoppers provide digital banking services and good ATM access, but do not require direct deposits to waive service fees. Products that require another type of activity, such as a minimum number of debit card transactions for purchases or payments can work for this group.

Returning-To-Banking. It’s not always the case that financial trouble is why someone used to have a checking account, but doesn’t today. People going through divorce or a death in their immediate family can also find themselves temporarily without checking accounts. Regardless, those who are returning-to-banking are most likely mass-market shoppers — two-thirds indicate their lowest daily balance is under $500 and they have less interest in digital banking and broader ATM access. Reloadable debit cards are less expensive alternatives for shoppers who might fail a Chex Systems inquiry.

Switchers. These shoppers express more functional requirements than shoppers that don’t currently have checking accounts. Eighty-four percent said they have a direct deposit and 58% said their lowest balances are over $500. Checking products that appeal to this group provide the features many want (ATM fee rebates or access to a large surcharge free network, mobile banking) and require a monthly direct deposit to waive monthly service fees.