Banks Target Gen Y with New Style ‘Free’ eChecking Accounts

To win millennial consumers, banks are offering contemporary ‘eChecking accounts’ that are free as long as you don't use any ‘retro style’ checking features like writing checks or visiting branches.

Simple Subscribe

Subscribe Now!

During the financial crisis and because of new banking regulations, many banks and some credit unions had abandoned their free checking account products in favor of checking accounts requiring minimum balances to waive monthly fees. The rationale (for banks) was that in a low-rate environment with fee revenue under pressure, it’s difficult to make a profit from low balance customers who have these free accounts.

While young consumers are less interested in using traditional checking services, banks should consider adding behavior-based incentives (e.g., a direct deposit, use on online billpay) to provide these account holders with free access to ATMs.

Every institution needs to win young consumers, and yet most people under 30 years old carry low balances. To address this weakness in checking product portfolios, institutions have begun rolling out digital banking accounts with fees for things like writing checks, teller transactions and paper statements. These types of accounts have more appeal to young consumers because Gen Y consumers.

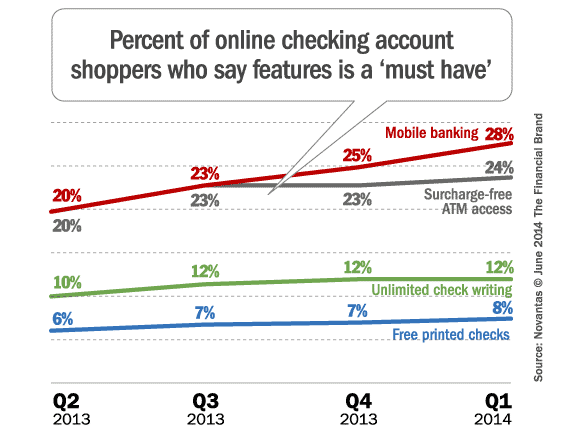

- Don’t care about unlimited check writing. According to a recent BankChoice Monitor survey fielded by Novantas, just 23% of checking account shoppers over 50 years old said they “must have” unlimited check writing and only 9% of shoppers under 30 years old said that the feature was a must have requirement.

- Want to bank on their smartphones. Unsurprisingly, only 21% of checking shoppers 50 years or older tell us that mobile banking is a “must have” feature requirement, compared to 40% of respondents under 30 years old.

Gen Y consumers are less likely than others to be turned off by accounts that charge for banking the old way. But most of these new style ‘eChecking’ accounts don’t include access fee-free ATM access… and that’s a huge turnoff for Gen Y consumers. A better checking product for Gen-Y consumers would be to charge fees for old ways to bank and connect ATM Fee rebates (or access to a surcharge-free ATM network) to a desired behavior like having a direct deposit or using the debit card a certain number of times.