How Leading Credit Card Apps Are Adding Features to Boost Spending

America's credit cardholders increasingly favor mobile interactions. Issuers, taking note, are increasingly designing for the mobile-only user base. The resulting apps are handheld financial command centers that enhance retention and accelerate spending.

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Major credit card issuers are increasingly turning their card mobile apps into handheld command centers that can do everything from providing instant virtual replacement of a lost physical card or secure mobile checkout to offering a ready source of answers to transaction queries — in some cases, including detailed receipts of transactions with cooperating retailers.

Digital promotion is an additional focus: A growing number of issuers are allowing non-customers to use the issuers’ card apps to shop for new cards and to compare offerings. In-app applications for new cards are becoming more common, with 70% of issuers providing a mobile entrée to apply. (Four out of 10 support applications within their app, while three out of 10 transfer the would-be applicant to a mobile web application.)

These findings are from Keynova Group’s 2024 Mobile Credit Card Scorecard, a study based on the usage of actual card accounts and their mobile access points by the research firm’s analysts. The 10 U.S. card issuers whose offerings were evaluated include American Express, Bank of America, Barclays US, Capital One, Chase, Citibank, Discover, PNC, U.S. Bank and Wells Fargo. Bank of America scored highest overall and for its mobile app. Wells Fargo and American Express tied in the evaluation of mobile web customer experience. The study uses 350 criteria to weigh each issuer’s mobile channel offerings.

Overall, Keynova found that issuers increasingly design for a mobile-only card customer base, according to Beth Robertson, managing director.

“They are creating opportunities for expanded card utilization by promoting digital wallets and secure mobile payments and by better communicating the rewards structure and earnings potential associated with specific credit cards,” says Robertson.

One overall shortcoming that Robertson observed is educational content within credit card apps. This element tends to be much stronger on issuer websites than mobile.

Appealing to Mobile-Based ‘Points Mongers’

Robertson says that more issuers are offering multiple ways to search and filter transactions so users can better understand charges to cards as well as how effectively they are tapping card providers’ rewards programs.

Here’s the carrot for issuers: The study notes that the latter capability, combined with more detailed information within mobile channels about card earnings and redemption possibilities, can encourage additional spending on a given card to maximize rewards. Nine out of 10 of the issuers show how much a transaction has earned for the cardholder and four out of 10 indicate what earning rate applies to a given transaction.

An ability to keep tabs on reward redemptions year-to-date is a feature awaiting further adoption. Only one in five issuers offer that service in their app and only two in five offer it via mobile web.

In contrast, it’s easier to track earnings in card rewards programs. Five out of 10 of the issuers’ apps report year-to-date rewards, as do six out of 10 of the issuers via mobile web.

Read more: Three Must-Have Features for Next Gen Banking Apps

A Solution to Mystery Charges, Right in the User’s Hand

Charges that cardholders don’t recognize are a common source of disputed transactions and customer angst.

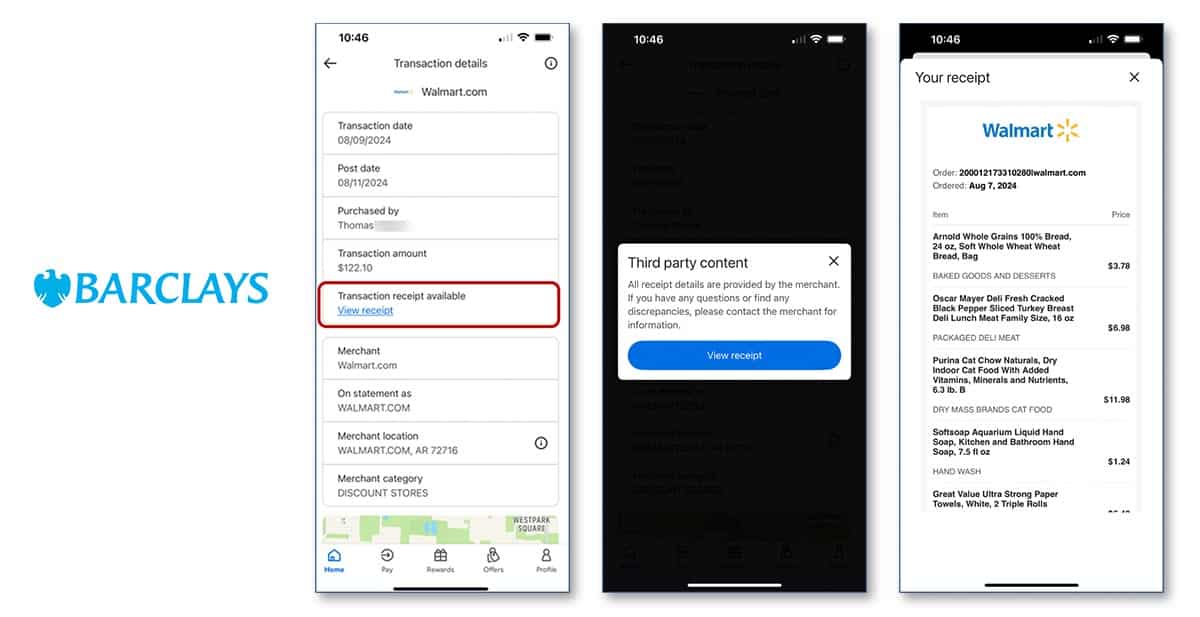

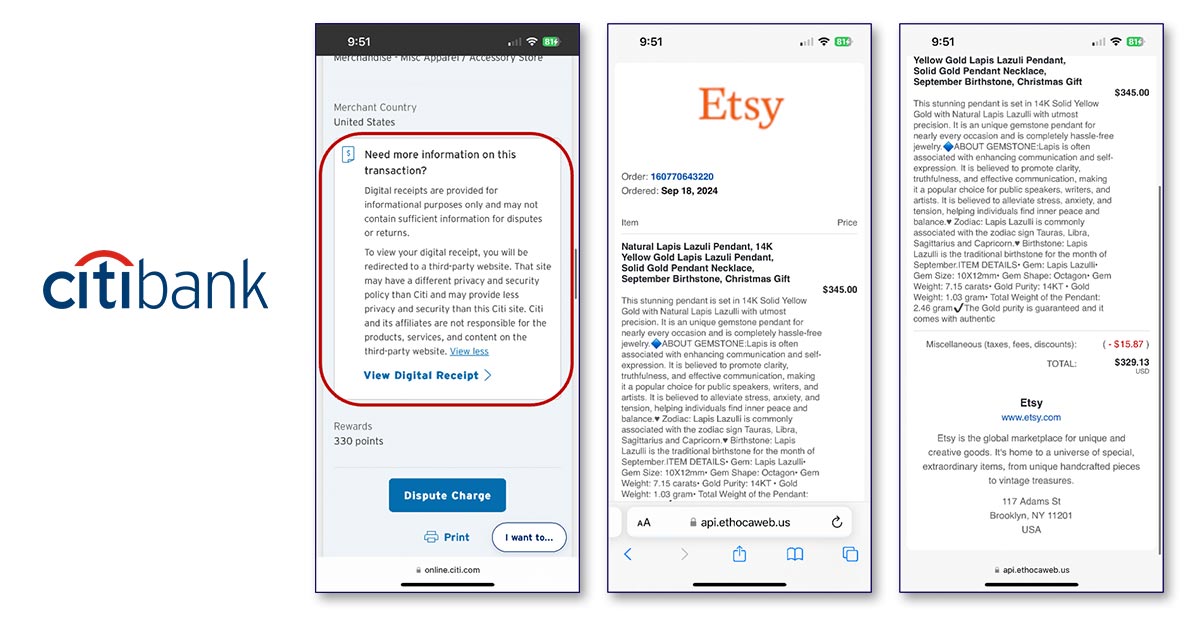

“More of the issuers are providing more transaction detail,” says Robertson, “so that if you click on a charge, you’re able to see not just the merchant’s name, but also their address. You might see the merchant location on a map. You might be able to click to view the receipt.”

In the vanguard are Barclays U.S. and Citibank, their offerings illustrated by the screen captures below, provided by Keynova.

Barclays and Citibank are among the card issuers working with merchants to provide self-service guidance to “What the heck is this charge?” (Images courtesy Keynova.)

Robertson says it will take a while to build out this capability across the board, because it generally requires coordination with each merchant. Barclays’ feature, above, depends on the bank’s relationship with Walmart.

She believes such cooperation will grow. “I think both parties will see the value as they see the potential for a reduction in disputed transactions and the research effort that goes along with those,” says Robertson.

Read more: Credit Card Delinquency and Balance Growth Will Moderate in 2025

How Credit Card Mobile Channels Increasingly Synch with Digital Wallets

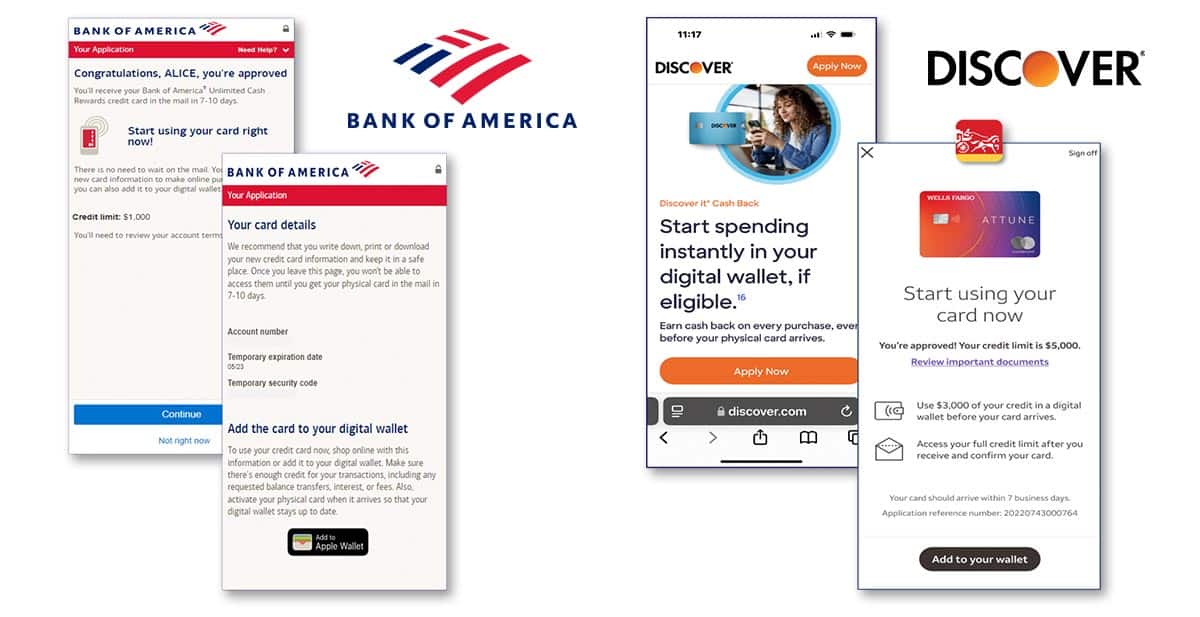

It’s increasingly common for major banks’ websites to provide detailed instructions on how to put the institutions’ credit and debit cards into popular digital wallets. Issuers have been augmenting mobile channels in multiple ways to get their cards into the wallets, seeing that move as a means of increasing “share of wallet” in the transaction sense.

The study found, for example, that half of the issuers studied give newly approved cardholders the option of using their cards immediately by transferring account information into their choice of digital wallet from within the mobile channel. Sometimes that option is included in the activation process.

Keynova’s report points out that this helps put the issuer’s card at the top of the consumer’s digital wallet of choice.

You’ve been approved for a card, why wait for snail mail to use it? Issuers increasingly help consumers get their cards into digital wallets for immediate spending — which also increases usage for that brand. (Images courtesy Keynova.)

Nowadays issuers commonly provide people who have asked for a replacement for a lost or stolen card the ability to immediately have the card replaced and virtually added to a digital wallet. This enables them to use their card without waiting for delivery of the plastic. Three out of five issuers give this option in some form.

Two out of five issuers are pulling rewards redemption into consumers’ digital wallets, enabling them to purchase with rewards from the digital wallet.

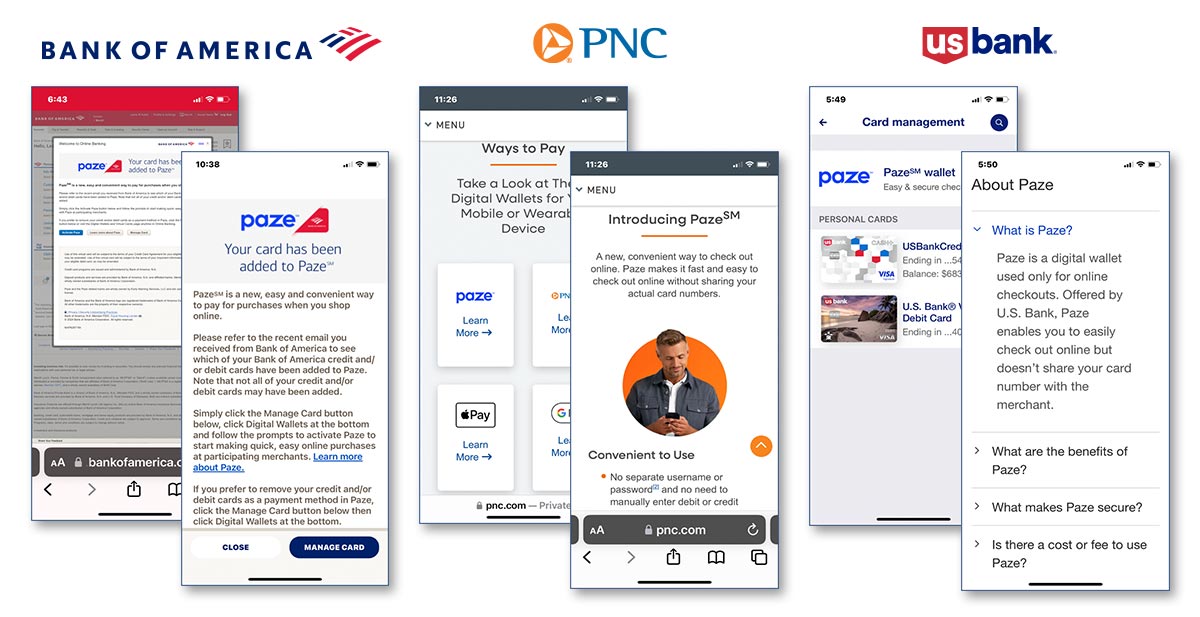

Six out of 10 issuers now offer some form or forms of secure mobile checkout. The report notes that this has been increased by the introduction of access to the Paze wallet from the Early Warning Services consortium by participating bank issuers.

Read more: CFPB Targets Large Digital Payment Apps, But Will It Stick?