Credit Card Delinquency and Balance Growth Will Moderate in 2025

"New normal" has become a post-Covid cliché, but now that stimulus and debt relief have been wrung out of the system, a clearer picture of card credit is coming into focus. The good news: TransUnion says the rate of growth of card debt will slow next year. On top of that, serious card delinquencies will stabilize.

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

On the roller coaster otherwise known as the U.S. consumer credit economy, have we come to a relatively flat section of the ride?

TransUnion forecasters think the impacts of pandemic-era stimulus and post-pandemic inflation growth are fading, with the former squeezed out of the economy and the latter easing.

The result will be two-fold, according to TransUnion, and both will play out over the course of 2025.

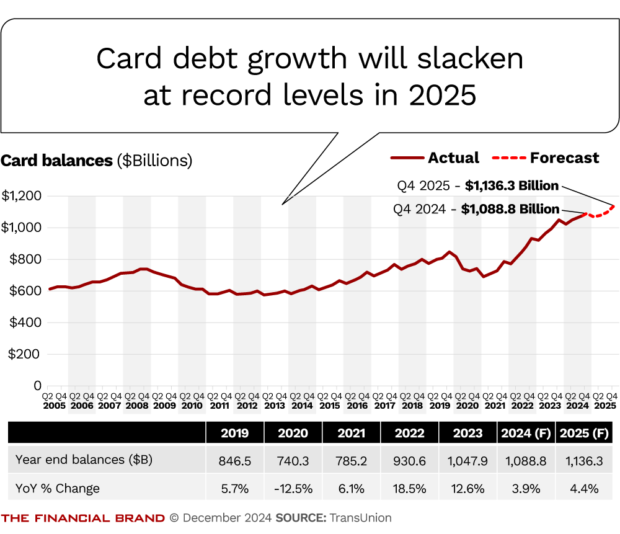

First, take overall credit card balances, still at record levels. The company projects that after seeing credit card usage rates grow, breaking the $1 trillion barrier in 2023, the rate of growth will level off. As shown in the first chart in the next section, after growing at double-digit rates in 2022 and 2023, company projections indicate that growth will fall into low single digits in all of 2024 and will continue in single digits through 2025.

To be clear, total credit card balances are still expected to increase in 2025. TransUnion forecasts that they will reach $1.136 trillion.

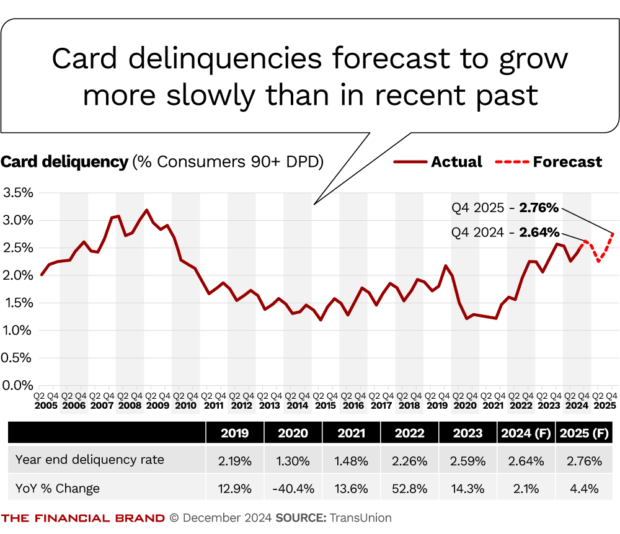

Second, the rate of growth for serious credit card delinquencies — those 90+ days past due — will continue to grow, but at lower levels versus the recent past, as shown in the second chart. Serious delinquency levels are still projected to increase in 2025, up 12 basis points by yearend, versus a projected 5 basis points by the end of 2024 — contrasted with 78 basis points in 2022 and 33 in 2023.

TransUnion also projects that auto loan delinquencies — those 60+ days past due — will become stable in the final quarter of 2024 and decline over 2025 to finish at 1.38%. Mortgage delinquencies — those 60+ days past due — will tick down slightly over 2025.

An exception to the falling delinquency rates will be unsecured personal loans, according to TransUnion. This growth rate is expected to rise from 3.87% forecast for the end of 2024 to 4% by the end of 2025. This will represent a small increase — 13 basis points — which TransUnion believes will result from lenders taking advantage of a stabilizing economy to lend to riskier borrowers.

Notably, a major use of unsecured personal loans is to consolidate credit card debt at a lower interest rate.

LendingClub, which began as a personal finance company but which became bank via acquisition, was recently advertising debt consolidation loans of as much as $40,000, with the option to borrow beyond debt consolidation to obtain immediate cash. The company both portfolios consumer loans and sells them to investors, including banks.

During third-quarter earnings, in October, Scott Sanborn, CEO, said that the “value of refinancing credit card debt through a personal loan is the most compelling it has ever been.” He noted that at that point the gap between average card and personal loan rates stood at a record 750 basis points, according to dv01, part of FitchSolutions.

Digging Deeper into Credit Card Trends

Credit card debt has been through its paces, according to Michele Raneri, vice president and head of U.S. research and consulting at TransUnion.

“At the very beginning of the pandemic, there was the lockdown and people couldn’t go out to buy anything and we started getting stimulus money that helped people to be able to pay down their debt and they weren’t running up credit,” says Raneri in an interview with The Financial Brand. “And so we saw a decrease in balances and a decrease in delinquencies.”

This was followed by “revenge travel” and “revenge spending,” Raneri recalls, as well as rising inflation.

Raneri says that this eroded many consumers’ savings, including accumulated stimulus payments, at the same time that they were racking up higher card balances.

“So that started resulting in higher delinquencies, and in the past couple of years we’ve been reporting on increased delinquencies, sometimes in the double digits in some of the products,” says Raneri. “But this year we’re seeing a slowdown in that.”

Raneri says TransUnion expects total credit card balances to continue growing as prices continue to rise, though more gradually, and as personal savings growth slows. However, card debt will grow more gradually, returning to patterns seen pre-pandemic, according to Raneri.

“This slowing growth and the overall stabilization of the economy offers optimism that we may be nearing a tipping point when it comes to the increases in serious delinquency rates over the past several years,” she adds.

Read more: Young Professionals Lead Consumer Spending Shifts While Middle-Income Households Face Pressure

Looking at Credit Scores in the Post-Pandemic, Lower-Inflation Economy

During the pandemic, a number of factors, including stimulus programs and various loan payment moratoria, had a temporary effect of making some consumers’ look financially healthier than they might otherwise have been seen. This led to some observers speaking of “credit score grade inflation.”

Now that the economy seems to be past most of the influence of that period, how have credit scores been shaking out?

Paul Siegfried, senior vice president and credit card business leader at TransUnion, says there’s been a continuing “barbell effect” in credit scores.

“We’re actually seeing about the highest level of super-prime scoring that we’ve ever seen, among the credit card population,” says Siegfried. “But the whole non-prime group — both near-prime and subprime — is starting to grow again as well.”

Siegfried notes that the credit-using population has evolved, as the consumer borrowing base isn’t static. While some consumers’ scores improve and they rise through the tiers, credit newcomers also join the borrower base.

“We have about 5 million consumers in this population that weren’t there five years ago,” says Siegfried. He said that sometimes the median or mean view of a credit population can obscure the extremes seen in a barbell distribution.

Credit newcomers don’t start out as subprime borrowers, Siegfried stresses. “You typically enter the credit world with a moderate score, and you have to become subprime,” he explains. “You actually have to have an issue — you have to stumble into subprime.”

Siegfried also says that in the wake of the last few years there’s a population of card users who worked their way out of being credit revolvers to become transactors — paying off their card bills in full each month.

“And we haven’t seen them come back in yet,” says Siegfried.

Read more:

- Why Cardholders Are Ditching Miles and Points in Favor of Cashback

- Must Banks Kick Their Plastic Addiction to Get New Payments Channels Off the Ground?

- Surging Credit Card Surcharges May Push More Consumers to Cash, Debit

Points for Lenders to Ponder as Trends Stabilize

Siegfried says this is a good time to be a super-prime lender, with borrowers in that category both interested in higher credit limits and able to handle them. That’s a strong source of industry growth right now.

“It’s about smart growth,” says Siegfried. “It’s about leveraging the data that you have to make sure you’re making the best possible offer to the right consumer at the right time.”

Raneri says the tools for finely parsing card bases is stronger than ever, both in terms of data for measuring and projecting performance and the computing power to do so. She says this is leading to many lender-level overlays being made on basic credit scores to detect targeted market opportunities among sub-segments among the credit tiers.

Growth in recent years of credit-builder card products among both fintech lenders as well as banks and credit unions has led to questions about individuals’ scores relying in part on such products for improvement.

Siegfried says “there’s always two sides to every theory,” but it’s something lenders have been mulling. He notes that this fall TransUnion introduced a credit report code that identifies credit-builder type products for lenders that want to analyze their ongoing influence on their borrowers’ scores and performance.