Subprime Auto Loan Delinquencies Boom, Spurred by Rates and Car Prices

As delinquencies rise among below-prime customers, many auto lenders are emphasizing loans to superprime borrowers. But yesterday's loans are still out there.

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Higher interest rates, higher monthly payments, and increasing stress on many consumers’ wallets are combining to push up overall auto loan delinquency rates—especially among subprime borrowers. However, the delinquency trend has multiple aspects and its severity varies considerably among among the slices of the industry.

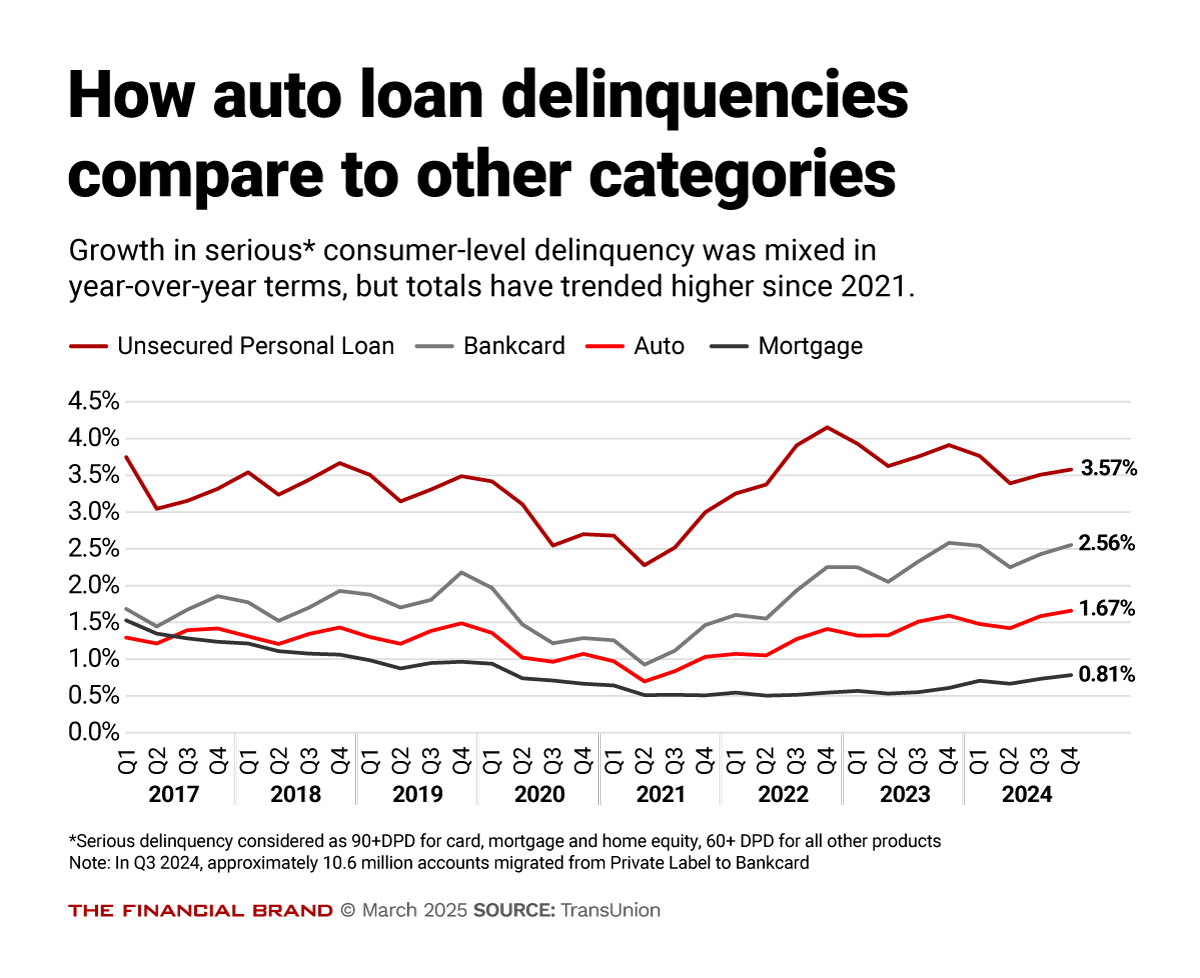

Serious delinquency rates are up for four key consumer credit categories, as shown in the TransUnion chart below that shows quarterly trends through yearend 2024. These credit categories include auto loans, bank cards, mortgages and unsecured personal loans. “Serious delinquency” is defined as 60+ days past due for auto and unsecured loans and as 90+ days past due for cards and home loans.

TransUnion notes that the current upward trend has been underway since about the midpoint of 2021. In general, lenders have responded by emphasizing more lending to super prime borrowers and pulling back from non-prime applicants.

This correlates with trends in a number that the company calls “AEP” — “aggregate excess payment.” This means the payment amount beyond the minimum due on all of a consumer’s debt. TransUnion considers this a good proxy for consumer financial health.

In the fourth quarter, the company computes, 73.9% of borrowers could afford to pay beyond the minimum required level. This is the lowest level since the fourth quarter of 2020.

“We’ve seen every risk tier showing a downward trend in aggregate excess payment over the last two years,” according to Dan Simmons, senior director, financial services research and consulting. “But it’s definitely been more pronounced among near prime and subprime people, where we’ve seen a substantial decline over the last two years.” At the end of 2024, 63.3% of near prime borrowers could pay beyond minimum required levels — and only 23.7% of subprime borrowers could do so.

The company’s analysis finds that while the average monthly payment on a new vehicle fell slightly in the fourth quarter, at $749 per month, it is quite steep compared to $655 a month in the last quarter of 2021 — over a 14% increase. For used cars, the average at yearend was $523, up from $494 per month at yearend 2021 — up nearly 6%.

On the rate side, the mid-March Cox Automotive market report indicates that auto loan rates are up year over year. New auto loans average 9.68% and used auto loans average 14.72%. TransUnion finds that consumer leasing has settled in at about a quarter of the new car financing market, in part over affordability issues.

Average credit account balances increased in January by over $1,000 compared to December 2024, Vantage Score reports. “This increase is the most significant month-over-month growth in nearly three years, bringing balances to a five-year high,” the company notes.

Bear all this in mind when considering the auto delinquency picture. In addition, the Trump administration’s tariffs will have an undetermined impact on the supply of new vehicles at a time when that has still not completely returned to normal after the disruptions of the pandemic period. The supply and price level of new autos influences the supply and pricing of used ones, which feeds into affordability issues. The Federal Reserve’s March 19 decision to leave rates as they are for now will also be a factor, and all with the backdrop of potential stagflation.

Digging into the Auto Delinquency Trend

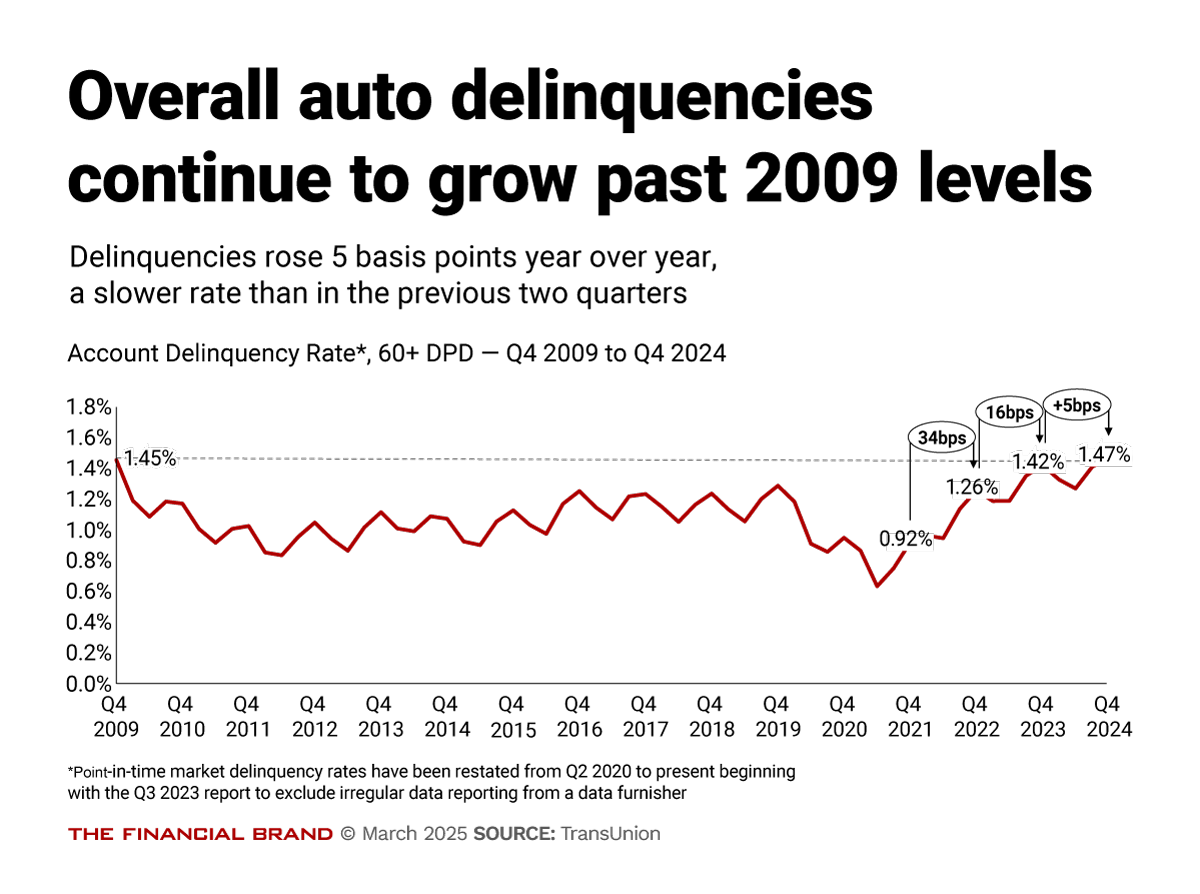

The overall delinquency rate on auto loans — 60+ days past due — increased five basis points in the fourth quarter, to 1.47%. As shown in the TransUnion chart below, the measure moved a tick above the high in the fourth quarter of 2009 — 15 years previously — when such delinquencies came to 1.45%. That was shortly after the end of the Great Recession, which ran from late 2007 to mid-2009. TransUnion notes that most of the deterioration has been among used vehicle borrowers, though the rate of rise in the overall delinquency figures has slowed somewhat.

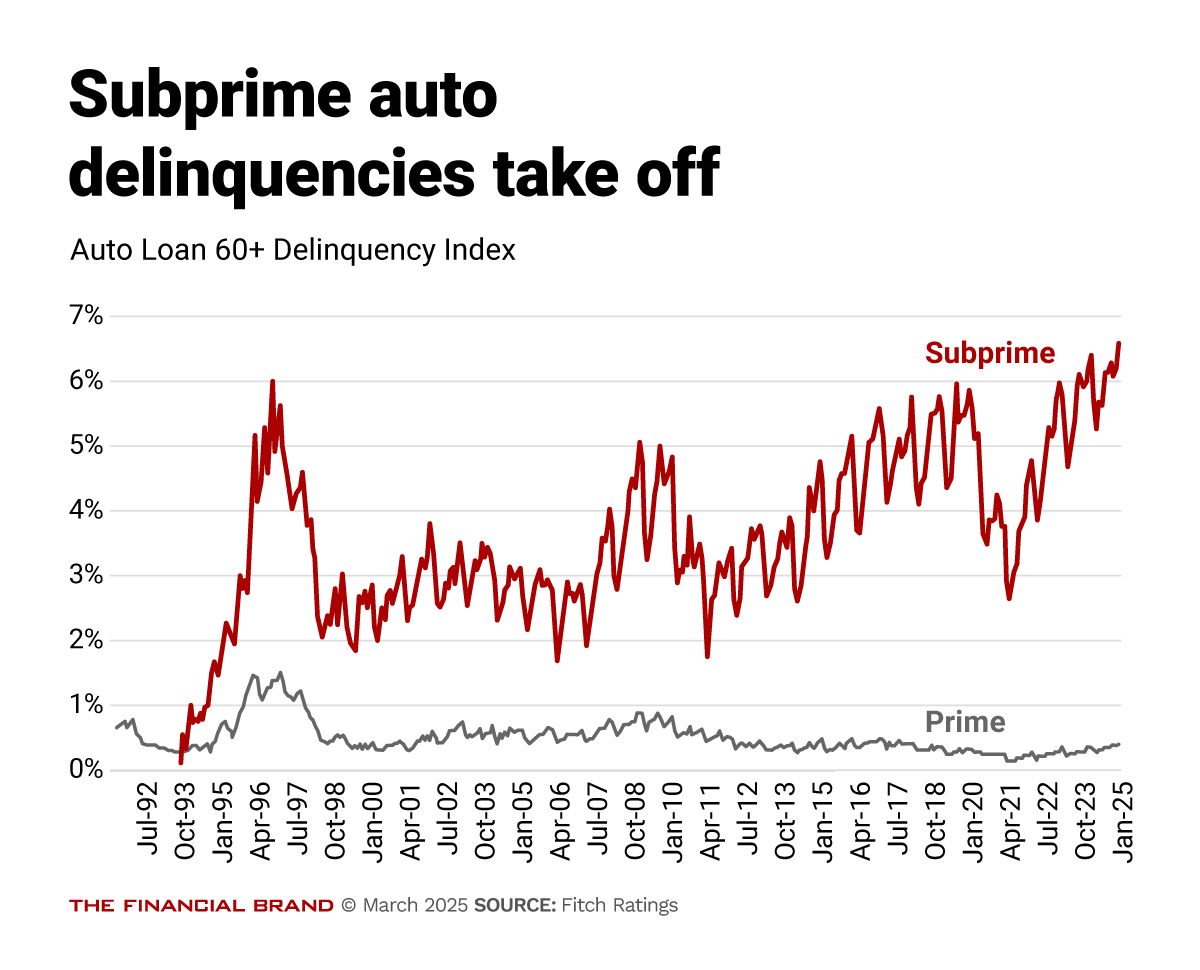

A different take on the numbers can be seen in figures from Fitch Ratings that split out auto loan delinquencies among subprime borrowers and those among prime borrowers. This data has driven some strong headlines given the drama of the curve tracking the rise in subprime borrowers’ delinquencies.

In January, delinquencies hit 6.56% in this credit tier, according to Fitch, compared to a trough in May 2021 of 2.58%. By contrast, the Fitch figures show that the delinquencies among prime borrowers came to 0.39% in January. This is up, but as the chart shows, nowhere near the levels seen among subprime borrowers.

TransUnion figures compare the performance across lender categories. At the end of the fourth quarter, among 60+ days-past due delinquencies, the highest delinquency rate among lender categories was 3.36% among independent lenders, which finance many of the below-prime borrowers. The rate among bank lenders was exactly half that, 1.68%. Credit unions came in at 0.93% and captive finance companies (those owned by automakers) at 0.89%). Banks have come back strongly into the market, now representing about a third of volume in both the new and used vehicle markets.

TransUnion figures do indicate that subprime originations have been falling in recent quarters. (The company tracks these one quarter in arrears, so that is through the third quarter of 2024.)

“Super prime was the underlying driver of auto originations growth in Q4 2024, and will likely continue in 2025,” says Satyan Merchant, senior vice president, automotive and mortgage business leader at TransUnion. “Affordability continues to be an issue for the used vehicle market and for below-prime consumers, impacted by higher rates and cross-wallet inflation. This is unlikely to materially improve until we have more certainty around used vehicle inventory and interest rates.”

Read more:

- Capital One Deploys Agentic AI to Support Stressed Auto Dealers (and Finance More Cars)

- How This Community Bank Tripled Loan Volume Using Smart Automation

- Lending Will Accelerate in 2025 As Consumers Get Used to Today’s Interest Rates

Lender Viewpoint: What Ally is Thinking about Auto Lending

In a fireside chat in early March during the RBC Capital Markets Financial Institutions Conference, Russell Hutchinson, Ally Financial CFO, said that over the last 18 months the major auto lender had been taking on more “S-tier” credits, the highest-quality borrowers in its base.

“We’re probably underwriting below our risk appetite,” said Hutchinson. (In a rating announcement made around the same time, Fitch said: “Although Ally’s net charge-offs have reached 10-year highs, its asset quality remains solid for its rating category given the secured nature of most of its loans.”)

“We still have a watch item out for elevated delinquency levels. That’s something that we’re still paying a lot of attention to,” added Hutchinson.

The impact of tariffs will differ in the short and long terms, particularly with the ripple effects on used-car prices. But Hutchinson said they will influence car buyers, including how they view new versus used cars and the types of cars they choose.

“There’s an affordability impact,” he said. “The consumer is already dealing with affordability. It’s eased somewhat since the pandemic, but there is still an affordability issue out there.”