Are Consumers Buried Under Too Much Debt? A New Report Says Maybe Not

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Executive Summary

- Total consumer debt has skyrocketed in recent years, but only in nominal terms. Adjusting for inflation produces a very different picture, according to TransUnion.

- In nominal terms, consumer debt ballooned 28% since 2020. But adjusted for inflation, the increase is much lower — closer to 3%.

- In light of the inflation adjustment, TransUnion believes that many consumers could safely take on additional borrowing, opening up opportunity for hungry lenders.

Have you ever read about some new box-office favorite’s opening weekend receipts surpassing an older record, and thought, “But wait — that flick came out 20 years ago. They’re not accounting for inflation”?

As it turns out, there’s been a bit of that going on as growth in consumer debt has been ramping up.

In a recent report, TransUnion says that in spite of the apparent growth in consumer debt, its calculations indicate “a more complex reality.”

TransUnion says that total balances across all types of consumer debt in terms of nominal dollars — not adjusted for inflation — rose to $18 trillion in the first quarter, up 28% from $14.1 trillion in the first quarter of 2020.

However, the company’s analysts applied the cumulative inflation rate — the Consumer Price Index increase for the same five-year period — to the totals. Turns out that the total increase in prices over that period came to nearly 24%.

“When adjusted for inflation, total balance growth in real dollar terms is more modest, amounting to $0.5 trillion over the five-year period, an increase of closer to 3%,” according to TransUnion.

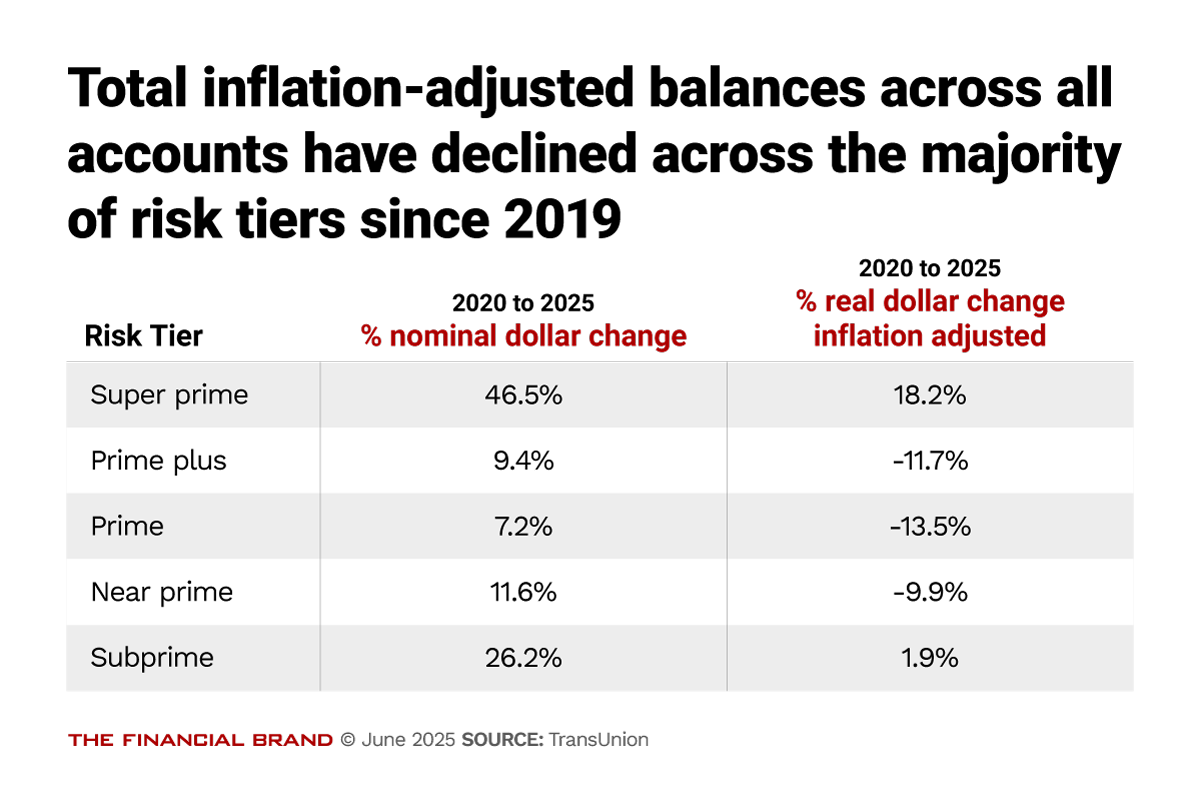

The company also found that balances declined in real dollar terms for most credit risk tiers over the same time. The table below shows the impact of this calculation for the five usual credit tiers.

All five credit risk categories saw increases on a nominal basis. However, adjusting for inflation, only super prime customers and subprime customers saw an increase in balances, 18.2% and 1.9%, respectively.

TransUnion offers these findings for the sake of perspective. The company suggests that consumers in most risk tiers are not overextended, and that many could potentially borrow more.

At the same time, wages have been rising for many consumers, points out Charlie Wise, senior vice president, research and consulting, in an interview with The Financial Brand. He says this suggests that concerns over people being in over their heads may be overstated.

In discussing these findings with lenders, he says, the concept of the inflation adjustment “really helps make them more comfortable with the idea that consumers still have a lot of borrowing capacity. The consumer still has gas left in the tank.” During its recent investor day, JPMorgan Chase’s Marianne Lake, CEO, consumer & community banking, noted that the bank was not seeing signs of distress among consumer borrowers.

Viewing Consumer Credit Through an Inflationary Lens

Of course, inflation hasn’t hit all consumers the same way, Wise points out.

“The lower-income consumer feels the effects of inflation more than a high-wage earner because so much of the low-wage earner’s income goes to rent, groceries, gas and other items that have seen very high rates of inflation,” says Wise.

So, extending more credit still has to occur at the individual customer level, and in the context of their total debt, not just with the lender. For example, delinquency trends are still a significant factor.

“Our goal is not to say, ‘Ignore the data, everything’s fine’,” says Wise. “We’re not saying, ‘They’re fine, just give them another card.’ Lenders know where they are seeing weakness in their books. They know where there are consumers who have high utilization and that are close to maxing out on their credit cards.”

The inflation lens, ultimately, gives a “more nuanced picture” of credit usage in context, according to Wise.

Wise points out that individual card issuers often don’t serve the whole spectrum of consumers, tending to focus on specific segments and risk tiers. A bank that tends to offer cards for people with higher credit scores may react to inflation trends differently from one who serves other tiers.

Read more: Rising Student Loan Delinquencies May Offer Renewed Refi Opportunities for Banks

Delinquency Trends Add Another Element to Credit Mix

Overall, Wise believes that consumer lenders have been returning to credit basics, paying more attention to individual borrowers’ ability to handle debt and their resiliency, or lack thereof, to take on more credit.

Wise explains that when the pandemic slowed the economy down, circa 2021-2022, many lenders loosened the credit reins to stimulate usage, especially in cards and unsecured personal loans. He says that lenders issued a significantly higher number of new cards to below-prime consumers, with fairly liberal credit lines. This trend contributed to rising delinquencies in some areas.

“It appears that we may be past the peak, and that lenders have gotten their hands around the current credit environment and consumers are starting to figure out how to make ends meet in this world of now persistently higher prices,” says Wise.

The 90+ days past due delinquency rate for credit cards for the first quarter of 2025 — 2.43% — was down from the 2.55% seen in the year earlier quarter. It was also down from the 2.56% rate seen in the fourth quarter of 2024, which was up from the 2.43% seen in the third quarter of 2024.

Wise noted that total credit card balances fell in the first quarter ($1.07 trillion) versus the fourth quarter ($1.1 trillion). Average card debt per borrower also fell, coming to $6,371 in the first quarter versus $6,580 in the fourth quarter. (Both the total and average debt figures for the first quarter were up from the year-earlier numbers. Note that these figures are not inflation-adjusted.)

There’s been a change in issuer behavior, according to Wise. Rather than grant the credit lines they might have a few years ago, they have been starting at lower levels, and ratcheting them up where borrower behavior supports that move.

Wise adds that customers with the best credit, the super primes, typically still get more liberal treatment. In part this is because even with higher limits they are frequently “transactors” — customers who pay off their balances at the end of the month. That makes the size of their lines moot.

“But for riskier borrowers, issuers are being a little bit more prudent about managing the early months on book of new products, letting out the reel for those who are proving themselves, and limiting their exposure to those who are struggling,” says Wise.

Read more: How a California Credit Union is Growing HELOCs with a Fintech Partnership

Unsecured Lending Took a Different Path

Conservatism kicked in sooner among unsecured personal loan lenders, Wise points out.

After delinquencies began to trend up in the wake of liberal originations, there was a broad tightening on the low end, and more concentration on lending to consumers at the high end. In the first quarter, unsecured personal loan balances grew only among above-prime tiers (prime plus and super prime). Average new account balances fell for the fifth consecutive quarter, as lenders tightened the amount of credit granted to individual borrowers.

However, some key tallies were up overall, including the number of unsecured loan borrowers, the number of loans, and total balances.

Wise notes that with unsecured personal loans, the entire loan is out the door from day one, versus credit cards, which are a credit line that fluctuates in drawdown.

“With the unsecured personal loans, there’s no risk management strategy other than, ‘Please pay me my money back’,” Wise says.

Something to watch: While overall delinquency levels (60+ days past due) in this area declined, in part reflecting a decline in subprime delinquencies, other risk categories showed increases.