Should Lenders Recalibrate as Super Prime and Subprime Segments Grow Simultaneously?

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Executive Summary

- Consumer lenders are watching a “barbell” effect developing in credit scores. The percentage of consumers who are super prime, the best risks, has been rising. But the percentage of people slipping into the subprime category is also growing, according to TransUnion.

- Demand for new credit cards for subprime borrowers is rising, but cautious lenders are starting those with smaller credit limits.

- Meanwhile, the meaning of other economic data is ambiguous, as major corporations begin white-collar layoffs and the period of “no hire, no fire” seems to be over.

Evidence of a credit score gap is emerging as some consumers rise from the middle tiers of the credit score spectrum toward the highest level — or fall toward the lowest. Lenders, especially credit card issuers, are already reacting to the trend, and may adjust further depending on what they see in their own portfolios in the months ahead.

So far, the double-barreled trend has favored the high end — the super prime tier — but movement into the subprime tier is worrisome, based on new research from TransUnion, released with its quarterly Credit Industry Insights Report.

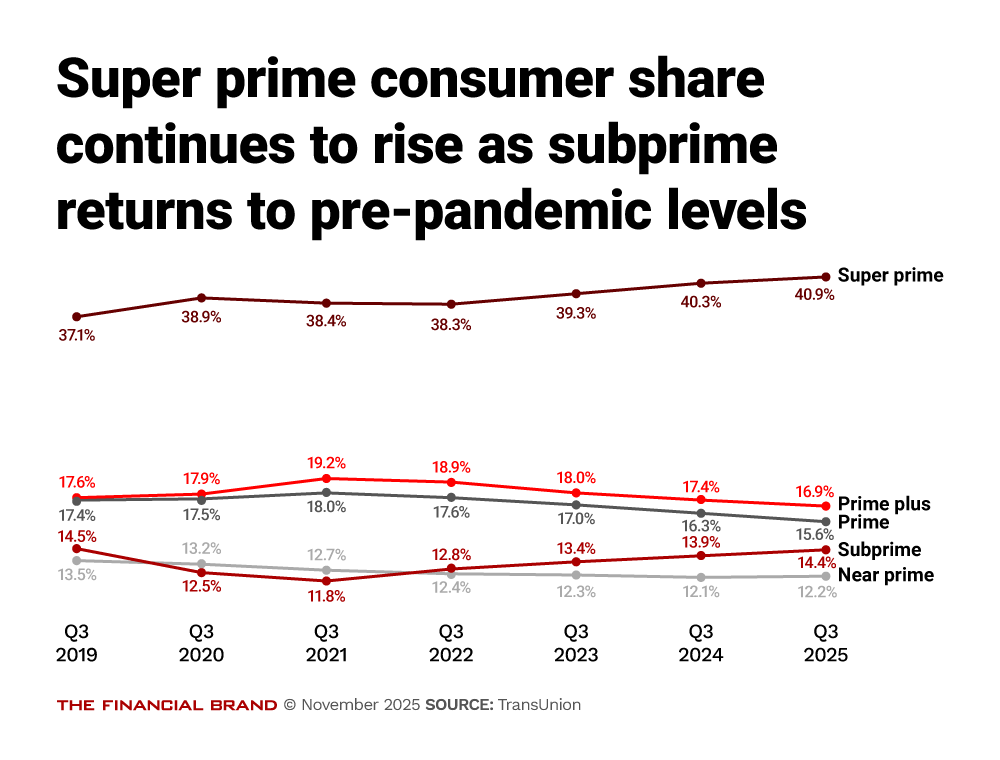

As shown in the chart below, the share of the consumer credit market that is rated super prime has grown from 37.1% in the third quarter of 2019 to 40.9% in the third quarter of this year. TransUnion says the population of super prime borrowers has grown by 16 million since 2019. Overall, TransUnion believes this reflects increased financial stability among these consumers.

At the other end of the spectrum, however, the share of the market that is rated subprime has steadily returned to pre-pandemic levels, hitting 14.4% in the third quarter. In the 2019-2025 period, the subprime segment fell to 11.8% in the third quarter of 2021 before beginning to climb. In part, the decrease resulted from pandemic-era debt relief and government payments, as well as reduced expenses that helped consumers pay off debt. At the time, some lenders worried about credit score inflation.

Meanwhile, the middle tiers — prime plus, prime and near prime — grew thinner.

Michele Raneri, vice-president and head of U.S. research and consulting at TransUnion, says that the company has seen the dual trend develop over several quarters. It has now become significant enough that it was time to flag it for lenders.

On one hand, the rise in super prime consumers opens up additional opportunities for making loans. “There are groups of people in our economy who are doing very well compared to the historical averages,” says Raneri.

However, the slower but steady growth in the subprime segment indicates that lenders must monitor those borrowers and prospects to see if they are getting into trouble. Raneri says TransUnion plans a deeper analysis in the months ahead to probe the trend further.

TransUnion has seen credit card issuers react to the rise in subprime by tweaking their offers when these consumers apply for new cards.

Lenders are still providing access to credit at the lower end, but they’re giving smaller credit limits for the initial line on new cards, says Raneri. She says this allows the lenders to see how subprime card holders handle the limits they have been granted.

“If they’re doing well, they can bump them up and bump them up again,” she says. However, if the subprime holders immediately run their cards up to the limit, that would be cause for lenders’ concern.

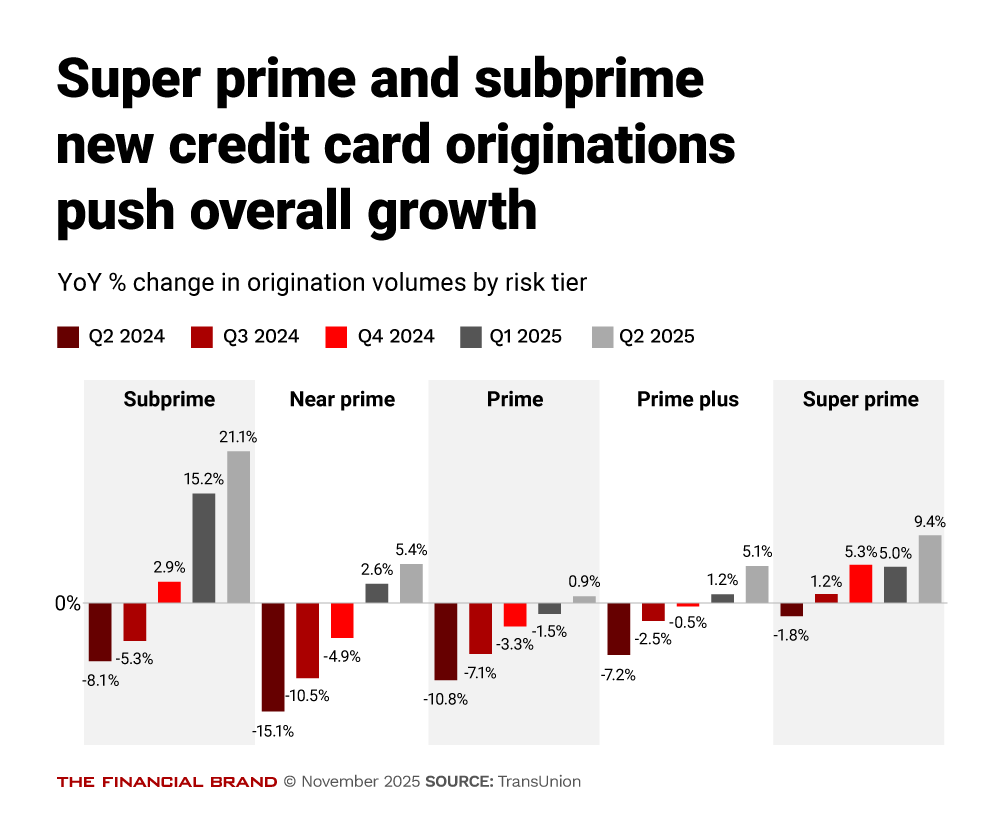

Originations in credit cards have been strongest among the subprime segment in the most recent quarter, as shown below, with originations in this tier growing 21.1% year over year. Super prime originations showed the second-largest increase, 9.4%. (TransUnion reports originations one quarter in arrears, to account for reporting lags.)

Raneri says she has so far not heard of wholesale credit line decreases , which would impact existing card holders. During the Great Recession, card issuers were trimming back limits of existing card holders, but TransUnion has not been getting questions about that practice.

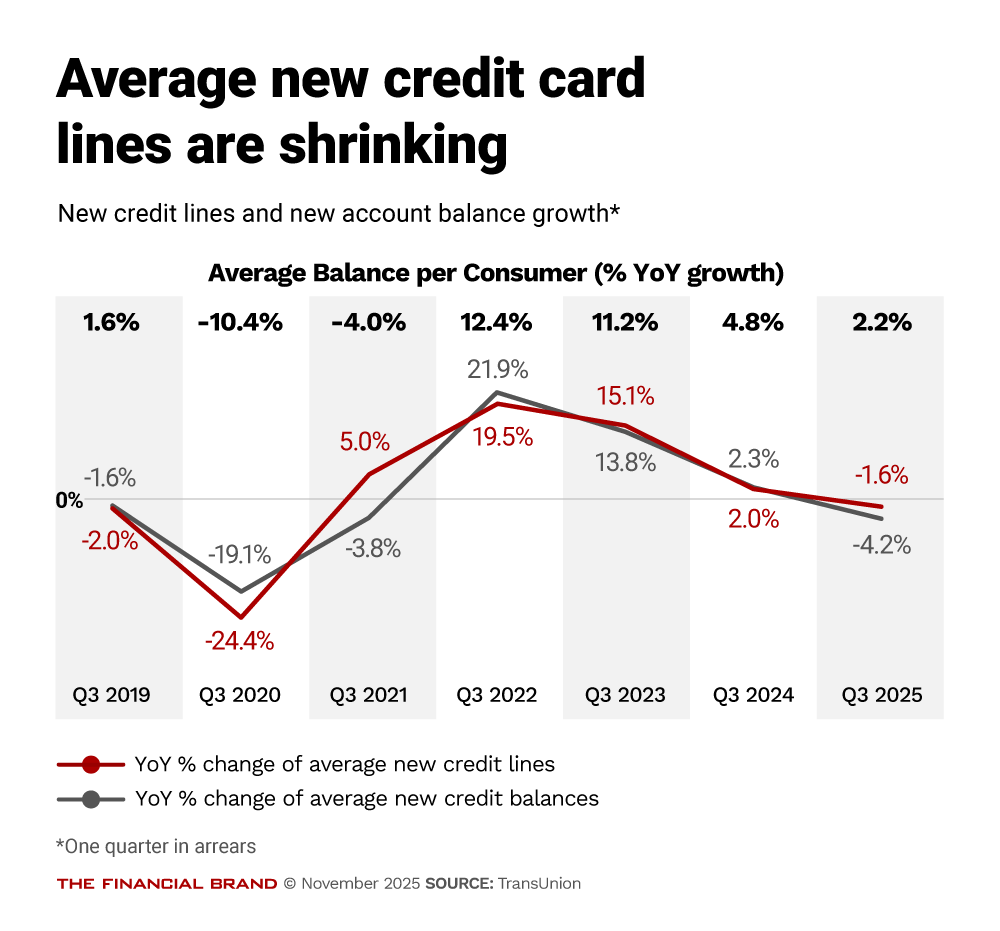

The trimming of new credit lines follows a trend that TransUnion has been tracking over multiple years, with both growth in credit limits and in new account balance growth slipping into negative territory.

Read more:

The Credit Mood: Lenders Are Betwixt and Between

In speaking to lender groups, Raneri says she’s not hearing major concern at this point. On the other hand, she is not picking up much optimism either.

“Everybody’s in this kind of wait-and-see period, recognizing this polarization,” says Raneri. “There are people who are sliding down from the middle and the lenders recognize it.”

Raneri says lenders still see remaining effects from the pandemic period, even though major institutions have been talking about a return to “normalization” for some time. She says it’s a matter of consumer psychology.

She explains that many people, especially subprime customers, grew accustomed to a level of spending that can no longer be sustained. Some won’t make the adjustment before it impacts their credit significantly. Another factor is the resumption of federal student loan repayments and collections, which can drive borrowers into serious delinquency quickly. (Asked about the impact of buy now, pay later financing, Raneri says the picture isn’t clear on that yet, as a good deal of data has yet to be gathered from those lenders.)

Read more: As BNPL Giants Push Debit Cards, Credit Unions Counter with Pay Later Offerings

How Credit Polarization is Impacting Specific Products

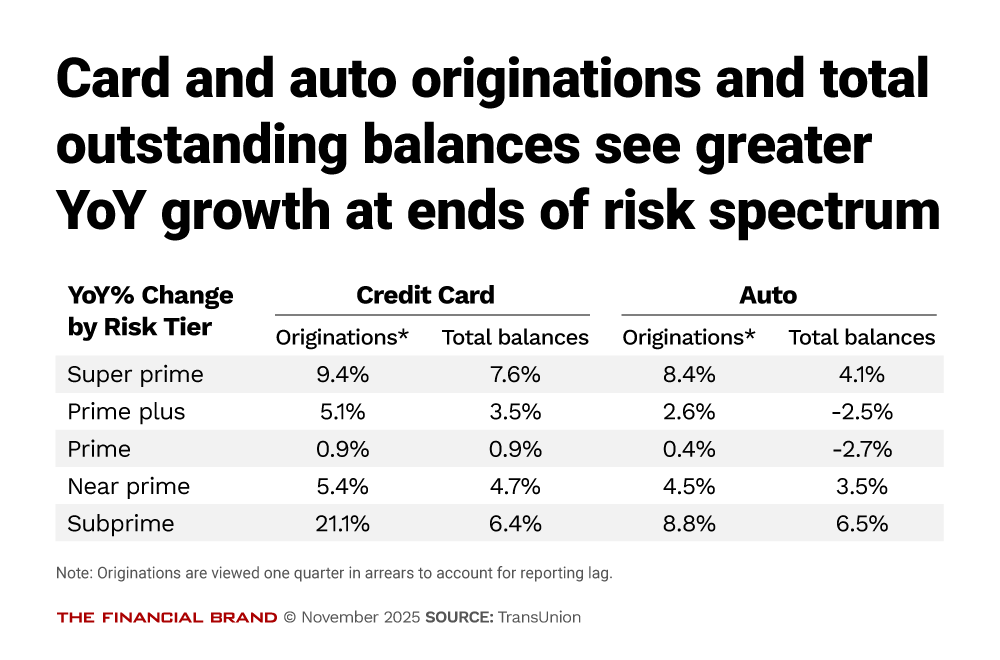

The two types of credit most affected by the polarization are credit cards and auto loans, shown side by side in the table below.

Credit card origination volumes rose for the third consecutive quarter, 9% year over year, reflecting the rising demand among super prime and subprime borrowers. An encouraging sign: Improvement in three tiers of delinquency — 30, 60 and 90 days past due. Average debt per borrower hit $6,523 in the third quarter, a 2.2% increase over the third quarter of 2024. The number of consumers carrying a card balance rose by about 2% over the same period.

Raneri says the delinquency trend is helpful, possibly signaling that subprime borrowers are getting a better handle on spending.

Auto lending continued an expansion in the third quarter, which TransUnion attributes to rate cuts and stable auto inventories. Here, too, the company sees a return to pre-pandemic norms. As shown in the table above, the greatest growth in both originations and balances has been seen among super prime and subprime borrowers.

“Despite rising costs, the mix of vehicles financed in the second quarter of 2025 — 43% new and 57% used — closely mirrors pre-pandemic 2019 levels,” according to the company’s report.

Recently Caribou, an online auto loan refinancing platform, reported that 84-month refinance terms have become the leading choice among borrowers for the first time. The company reported that borrowers are using extended loan terms in order to bring down monthly payments and that the seven-year refis pulled to the front as of September.

Raneri says this tracks with what TransUnion is seeing. Both companies note the increasing lives of cars. In May, S&P Global Mobility reported that passenger cars now average 14.5 years in service. “They’re more technical and more expensive, but they’re also more durable,” says Raneri.

As shown in the table above, the two leading groups for auto loan originations are subprime, at 8.8% in the second quarter, and super prime, at 8.4%.

Meanwhile, unsecured personal loans, frequently used to consolidate credit card and other personal debt, hit a record mark for outstanding balances in the third quarter.

Balances rose to $269 billion, compared to $1.11 trillion in credit card balances and $12.7 trillion in mortgage balances.

Originations for the third quarter notched a 26% year-over-year increase. Growth was strongest among subprime borrowers, up 35%, and near prime borrowers, up 26%. The two tiers now account for two thirds of outstanding unsecured personal loan debt. Fintech lenders have been regaining share, representing about 41% of originations in the third quarter, up from about 32% a year earlier, according to TransUnion.

The fintechs now hold more than half of unsecured personal loan balances — 53% — with banks in second place at 21%.

Balances for all credit tiers were up in the third quarter, with super prime borrowers’ balances rising the most, at 11%.

Behind these increases, Raneri points out, many lenders are taking a similar tack as credit card lenders. They’re doing a lot of originations, she says, but the loans are smaller. In part this reflects caution based on higher delinquencies seen a few years ago in unsecured personal loans, according to Raneri.

Read more: Want to Lend to Low-Income, High-Risk Borrowers? See What This Fintech Does

Steps Lenders Can Take Towards Growth with Safety

In the interview with The Financial Brand, Raneri outlined multiple actions lenders can take as the subprime population grows. An overall proviso is to look beyond the raw credit score. Raneri says some lenders still regard the score as their main touchstone.

For example, she says, a lender should dig deeper into the applicant’s utilization of available credit. Someone who is maxing out their credit lines may be a higher risk, possibly warranting a lower credit limit.

Another factor is recent delinquencies that may not be reflected in the individual’s score yet. “If there’s been something in the last few months, that’s going to be an indicator that the person’s got a bigger problem,” says Raneri.

Raneri also suggests looking at how much borrowers are paying on debt beyond the required minimum payment.

Such filters address trending in credit performance.

“It gives you an idea of the direction they’re going in,” says Raneri. “Are they laddering up and doing better than their score represents, because they had a problem but they fixed it? Or are they in the middle of the problem, and sliding down?”

Read this next: The Credit Confidence Gap and What It Means for the Next Generation of Cardholders