How Gen Z and Millennials are Converging into a Single, Digitally Native Market

By Michelle Gauchat and Nick Cowell of Deloitte Consulting LLP

Simple Subscribe

Subscribe Now!

For years, banks have treated Gen Z and millennials as two separate plays, with different campaigns, and sometimes different messaging.

Gen Z has often been portrayed as distrustful of financial institutions and drawn to alternatives. Millennials, on the other hand, have been depicted as financially cautious, shaped by prior crises and more deliberate in managing money. The premise was simple: these are distinct customer segments that require differentiated strategies.

But banking behaviors tell a different story.

Recent Deloitte research suggests Gen Z and millennials function more like a single digitally native group than two fundamentally different banking markets. The real distinction isn’t generational, but between digital natives and everyone else.

Start With Loyalty

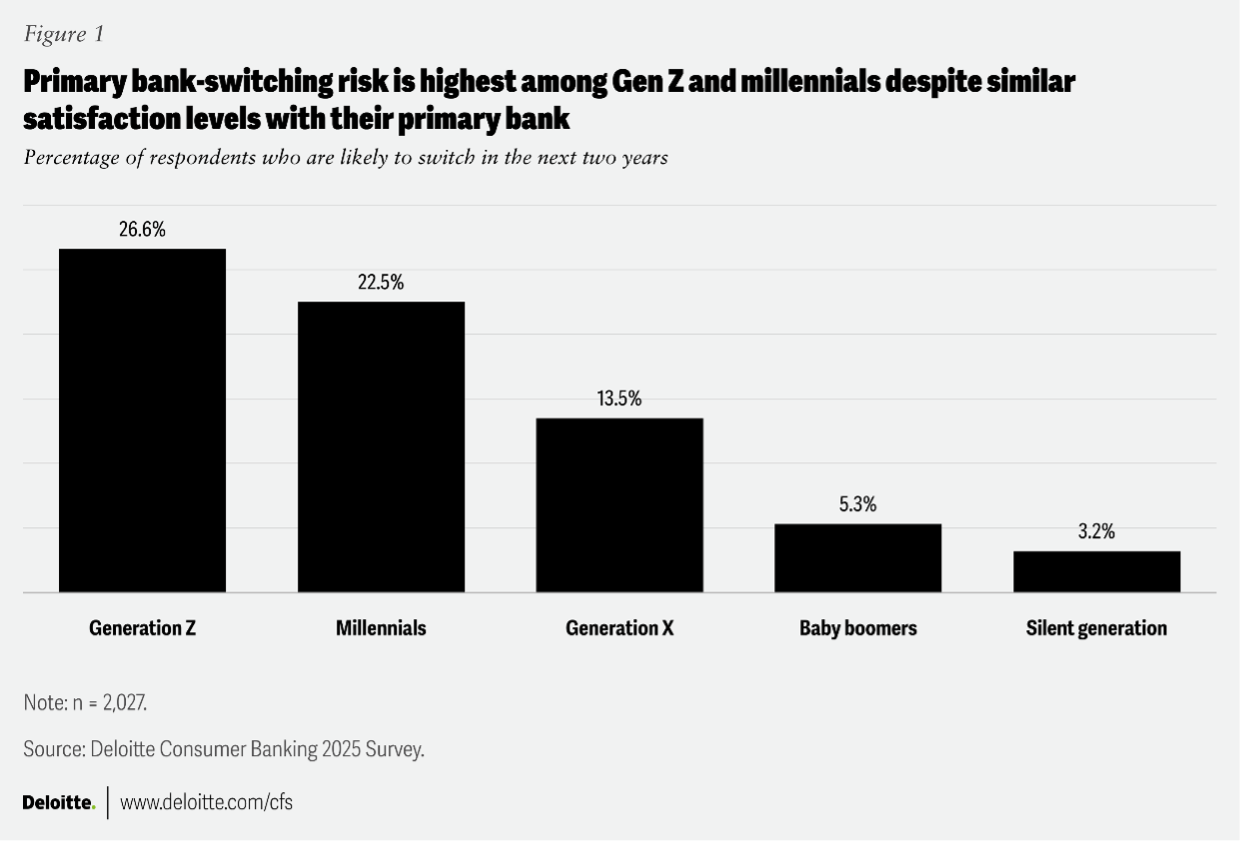

Across generations, satisfaction with primary banks remains high among those surveyed. Yet satisfaction no longer guarantees retention. That dynamic isn’t new. Academic research has long questioned the tight link between satisfaction and loyalty. What’s new is how visible that gap has become among younger banking customers.

In Deloitte’s survey on banking behaviors among different generations, Gen Z and millennials report satisfaction levels similar to older segments (Gen X baby boomers and the silent generation). But they show the highest likelihood of switching providers (see below). Respondents are comfortable moving accounts. They are open to trying new platforms. They do not see a long-standing relationship as a reason to stay.

That aligns with broader generational research. Analysts have noted that Gen Z respondents tend to approach banks with skepticism and lower institutional trust. Meanwhile, earlier reporting on millennials shows a group that learned to manage risk and diversify relationships after living through economic disruption. Together, those experiences reinforce a practical mindset: stay if it works. Leave if it doesn’t.

Switching is increasingly a pragmatic consideration.

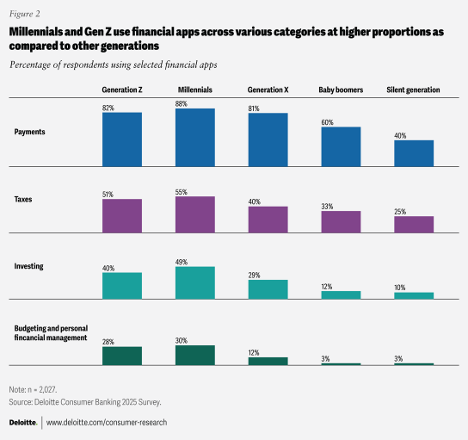

The second structural shift is app behavior.

According to the Deloitte survey, millennials and Gen Z use financial apps at similar rates across payments, investing, budgeting and planning tools (see below). External research supports that convergence, with some data on U.S. banking habits showing younger generations clustering closely in digital usage patterns.

Financial life for these customers is often modular. One app for payments. Another for savings. A different platform for investing. Maybe a fintech for short-term credit or buy now, pay later.

This mosaic approach reflects comfort with digital ecosystems. Deloitte’s own work on digital banking maturity underscores how quickly platform expectations are evolving. And globally, the rise of neobanks shows how digital-first providers have capitalized on that expectation.

Banks once competed to be the center of a customer’s financial world. Increasingly, they are competing to be one trusted node in a broader network.

Data Sharing Adds Another Layer

Younger consumers are often portrayed as privacy anxious. Yet research shows generational differences in how data control is perceived. Gen Z and millennials are more accustomed to managing permissions and toggling access. They are more likely to link accounts if they see value.

External research on open banking sentiment shows growing acceptance of data sharing when it improves functionality. Deloitte’s survey echoes that pattern. Younger customers report higher comfort with data sharing and a stronger sense of control when doing so.

That comfort does not mean indifference. It means conditional trust. Share data, get value.

Banks that resist interoperability risk appearing closed. Banks that design transparent, user-controlled data frameworks often reinforce credibility.

Generational Differences Still Exist

Gen Z shows greater influence from social media in financial decision-making, consistent with broader marketing research on generational behavior. Millennials, by contrast, often report stronger financial confidence shaped by lived economic experience.

But these are life-stage nuances, not structural digital divides.

Both groups generally expect seamless onboarding. Both can assume mobile-first functionality. Both often want integration across platforms. Both will likely test alternatives if the experience falters.

Industry commentary has increasingly pointed in this direction. Some have argued that another generational banking shift is underway. Analysts also note that banks should rethink relationship models as life-stage expectations evolve.

The strategic takeaway is straightforward.

Why continue designing fundamentally different digital strategies for Gen Z and millennials? The behavioral data does not support it

Instead, consider designing for digitally fluent customers whose expectations center on speed, flexibility and relevance.

Redefine loyalty around experience quality, not tenure. Revisit platform architecture with openness in mind. Treat data transparency as a competitive advantage, not a compliance exercise.

Banks often ask how to win Gen Z. Or how to deepen millennial relationships.

The better question might be how to serve a unified digital group that sees financial relationships as configurable and fluid.

Gen Z and millennials are not two puzzles.

They should be treated as one force accelerating the shift toward platform-based, experience-driven banking.