The Wealth Transfer Problem No One Talks About — And the Community Banks Solving It

By Matt Doffing, Senior Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Executive Summary

- A massive generational wealth transfer is underway, with heirs moving inherited assets away from community banks 70% of the time — threatening deposit stability as over $30 trillion changes hands by 2030.

- Community banks are adopting digital estate planning tools — like Thomaston Savings Bank’s partnership with Paige — to help families prepare proactively and help banks retain relationships with the next generation.

- Investing in technology at “the edge of money” is becoming a strategic necessity as community banks look to foster brand connection that transcends products and pricing.

Community institutions face a wealth transfer problem: When a spouse, parent, or grandparent passes away, community institutions aren’t the most common home for those deposits afterwards. It’s becoming the single most significant threat to community institution deposits of this decade.

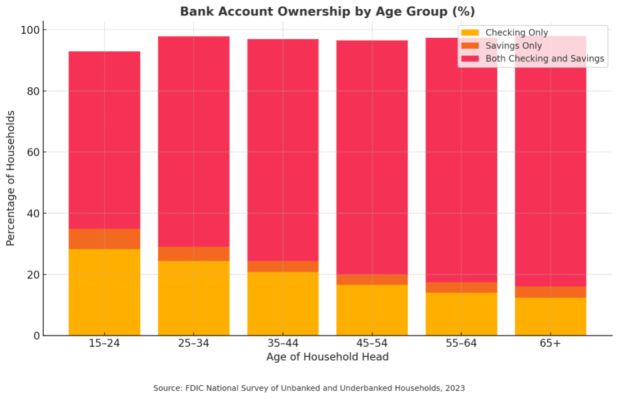

A study of 40 community institutions from markets across the country by Alloy Labs Alliance found that the average depositor age was over 60 years old. Looking at community banks as a group, approximately 57% of depositors are over the age of 50, compared to only 35% at the top 50 banks.

What’s more, younger generations are less likely to have a well-established banking relationship, according to the FDIC’s underbanked survey.

The best-case scenario for community institutions after a customer passes away is that the heir has not decided to move their inheritance elsewhere — yet.

Unfortunately, that best-case scenario is not the most common. Just the opposite.

By 2030, American baby boomer women will control most of $30 trillion in financial assets of their generation, having inherited it from parents or taken over family finances after the death of a spouse. A wealth transfer of that magnitude “approaches the annual GDP of the United States,” according to recent McKinsey research. The firm says some 70% of those women will move to a new financial institution after taking over or inheriting wealth.

Getting Ahead of the Ball

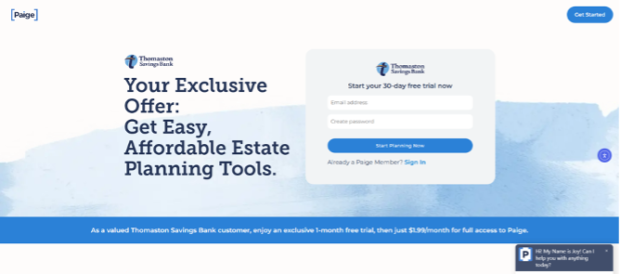

Community institutions, however, are not sitting idly in the face of this demographic reality. Some, such as Thomaston Savings Bank, a $1.8 billion mutual savings bank based in Thomaston, Conn., are investing in a more favorable set of options: Using technology to guide and assist parents and grandparents in creating wills, organizing and storing critical documents, and preparing for password sharing. The service is made possible through a partnership with a platform called Paige.

For Thomaston Savings, which announced the new service in May, helping customers prepare their estate plans digitally was about expanded access to service. If people had questions or needed help, they had to come into the branches for face-to-face interactions. Adding Paige allowed the bank to scale estate planning services and make guidance more accessible.

“You need service to stand out as a community bank,” says Jonathan Gilbode, SVP, chief digital and product officer at Thomaston Savings. “We were looking for services that were usually in-person conversations, and we wanted to bring self-serve online through our digital environment.

“Our mission is to be our clients ‘ trusted advisor…but it could be that our client has passed away and the person contacting us has no relationship with us yet,” Gilbode explains. “We want to shift the client experience to be more centered around proactive care rather than reactive service. Then, for whoever we’re engaging, we’ve already provided clear proactive value in helping their family.”

Preventing a Poor Experience

Now, the higher the parents’ wealth, the more likely they are to have help with estate planning. However, about 63% of people who make more than $80,000 per year – these are above-average earners compared to the national average salary of $66,622 – say they have not “gotten around to it” when asked their primary reason for putting off estate planning. People with discretionary savings are delaying basic estate planning steps.

Approximately 52% of people are unaware of where their parents store their estate planning documents, according to Cambridge Trust. And, only 40% of the nation’s 250 million adults are adequately prepared for transferring their assets at the time of their passing. Often, when a parent passes away without documents transferring accounts to their new owner, the first stop for heirs is the bank.

Community banks often help with those questions, but they are also usually stuck delivering bad news: We can’t help you because you have no legal access to these accounts. The next stop for the family, then, may be probate court.

If you’re the eldest daughter, the most common person in the family to be named executor, and your first interaction with your parents’ bank is “we’re sorry we can’t help you,” are you more likely to move funds to your current bank or keep the deposits in your parents’ bank? Even if the bank followed regulations and did its best, we already know that women tend to transfer inherited deposits to a new institution.

When community institutions help parents plan, and since they have the largest share of that age group, removing bad experiences enables banks to transition from a reactive to a supportive role in the estate for the next generation.

Through its Paige partnership, Thomaston Savings is also doing more than covering the practicalities of estate planning; they’re reaching deeper into the relationship to establish a brand connection.

Dig deeper:

- The Great Wealth Transfer: How Banks Win the Next Generation of Business Owners

- Don’t Wait for the ‘Great Wealth Transfer’ – Help Younger Customers Reach Goals Now

- Navigating Millennials in Banking: Capturing the Impending Generational Wealth Transfer

Flipping the Script on Branding

Dad’s old community bank may not have the same technology as the nationwide bank where his daughter keeps her accounts. Now, those community banks can have meaningful digital advantages that larger banks do not.

Customers of Thomaston Savings can get a head start on gathering and storing family videos and photos. They can even schedule a calendar of messages for loved ones to receive in the years after they are gone. (All of these services are offered through one discounted subscription to depositors and provided via a cobranded portal from the bank’s website.)

Paige Founder & CEO Emily Cisek shares the story of Emma, the daughter of a now-deceased depositor and her mother, who banked with a community bank in the Midwest. Emma still receives birthday emails – written by her mother before she passed away – through her bank’s technology partner, the same bank where her mother had deposited her life’s savings.

“We have moms using that messages feature to write a future birthday for each of their children,” Cisek says. “And these emails share different memories from their kids’ childhood, some of which are saved in pictures or videos on the platform as well.”

If your mom sets up messages for you and your siblings for years into the future, not many people cancel the account. The practicality of that emotional tie to their parents’ community bank keeps that brand adding positive value in their lives.

Innovation at the Edge of Money

It’s not a deposit service, but community institutions are turning to partners for differentiation – especially when up against the largest nationwide banks – in services at “the edge on money,” as Alloy Labs Alliance CEO Jason Henrichs describes it.

It’s about deposit effects created “looking beyond the account and the transactions for new ways to create value for the customer,” he says. “That can require partnering with technology companies that didn’t start out pursuing bank partnerships. They’ve built valuable services that created new value for customers and the banks.”

Since it launched, Paige has also partnered with the $1.4 billion American State Bank, based in Sioux Center, Iowa, as well as the $575 million Claremont Savings Bank, based in Claremont, N.H.

These technology companies “give the service to the banks for free,” says Josh Seigel, Chairman and CEO of StoneCastle Partners, and also an investor in Paige. “There’s really no process other than vendor due diligence for banks. Customers can use this service and pay a monthly fee of approximately $2; it’s intended for individuals who don’t have an estate attorney.

“Millions of community bank customers have no will, or their family doesn’t know the location of necessary documents,” Seigel explains, “even healthcare proxies for children at college. If they were ever hospitalized, are the right permissions in place? Where are they stored?”

Community banks need strategic and brand advantages for use cases that provide unique value, Seigel says. “It connects customers to the bank for a purpose much deeper than the rate on a deposit account.”