Fintechs Grab A Bigger Share of Churning Accounts. How Can Banks Respond?

Moving accounts is faster and easier than ever. So far, fintechs have been picking up more paycheck-to-paycheck consumers and national banks more affluents and "HENRYs." But fintech momentum is growing.

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Fintechs gained a greater share of consumers who changed their primary financial provider and consumers who opened their first accounts in 2024, according to research from Curinos.

Depending on the economy ahead, fintechs could maintain the same pace for 2025 — or circumstances could support more dramatic changes: A temporary lull or dip in movement to fintechs, followed by a further significant jump.

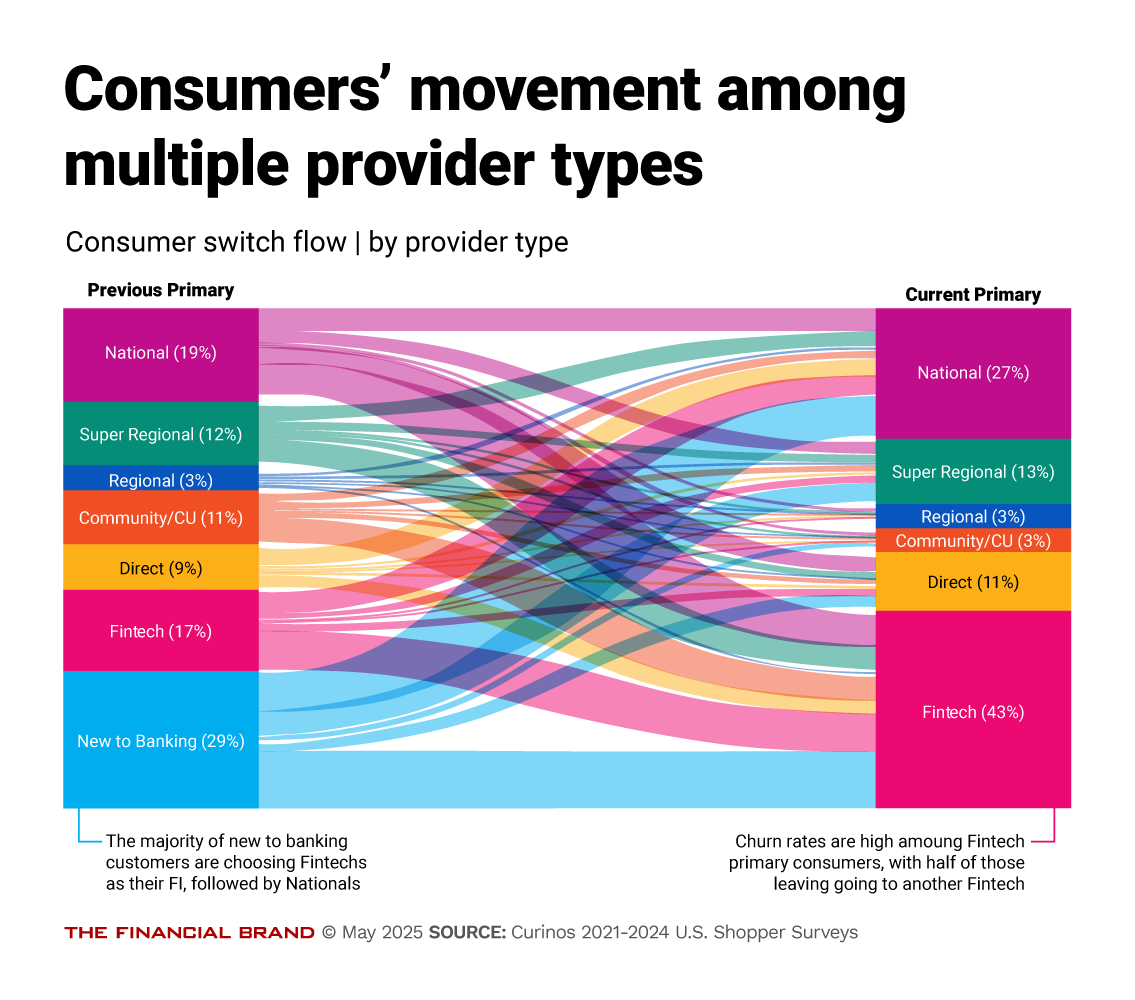

The broadening of fintechs’ offerings is supporting some of the growth in interest and share, Curinos notes. The company also sees a high rate of movement from fintech to fintech. About half of the people leaving fintechs in 2024 moved to other fintechs, rather than to a bank or credit union, as shown in the chart below.

Curinos’ study, which it has conducted for a decade, looks not at the overall share of market among banks and credit unions versus fintechs, but instead at the movement of people who switch accounts, or open accounts for the first time. Respondents aren’t necessarily closing their accounts with their original providers —but they did tell Curinos which provider they see as their primary source of service.

“This is the ‘churning’ population, which looks much different from the average consumer population,” says Andrew Hovet, managing director.

What the ‘Churners’ Look Like, and Why

This population comprises the following mix:

• Paycheck-to-paycheck consumers, 59%, people with less than a month of income in liquidity.

• Stable mass market customers, 26%, people with income of under $100,000.

• “HENRYs” — “high earning, not rich yet” — 5%, consumers under age 35, with income of $100,000 or more.

• Affluent customers, 9%, people 35 or older, with incomes of $100,000 or more.

Hovet explains the mix this way. Paycheck-to-paycheck consumers are frequently looking for a better deal from a financial provider, so they are often open to switching. They also tend to overdraw. Hovet notes that while there’s been some movement on overdraft fees and policies among banks and credit unions, these consumers frequently face such charges. Fintechs often offer a cheaper alternative that many banks and credit unions aren’t matching. Fintechs got aboard the movement to early wage access, as well, “which is really appealing to the needs of this segment,” he explains.

Many players, especially banks, are after affluent customers, Hovet says, but the firm has found that the affluent accounts are stickier. They are much less likely to move to new providers.

On the other hand, HENRYs “are kind of like tomorrow’s affluent,” he says. So, many banks are working to attract HENRYs. But they are also fair game for fintechs because they are younger and face life events that could lead them to seek another financial provider, according to Hovet.

Hovet says that most banks make the greatest portion of their consumer banking income among affluent customers and the high end of the stable mass market. Yet, in principle, they can’t afford to ignore the rest of the market.

“If I’m going to grow my core customer base, I’ve got to be paying attention to the retention of people I already have. But I’ve also got to be paying attention to the customers who are in motion,” says Hovet.

A key factor is that movement among institutions has become much easier, especially compared to the days when changing primary providers meant visiting two institutions’ branches to make the changeover. And with the low friction associated with fintechs, hopping from one to another can be pretty quick, says Hovet.

Read more: Fintech Banking Suddenly Advances on Multiple Fronts

Fintechs Gain Share of Primary Relationships

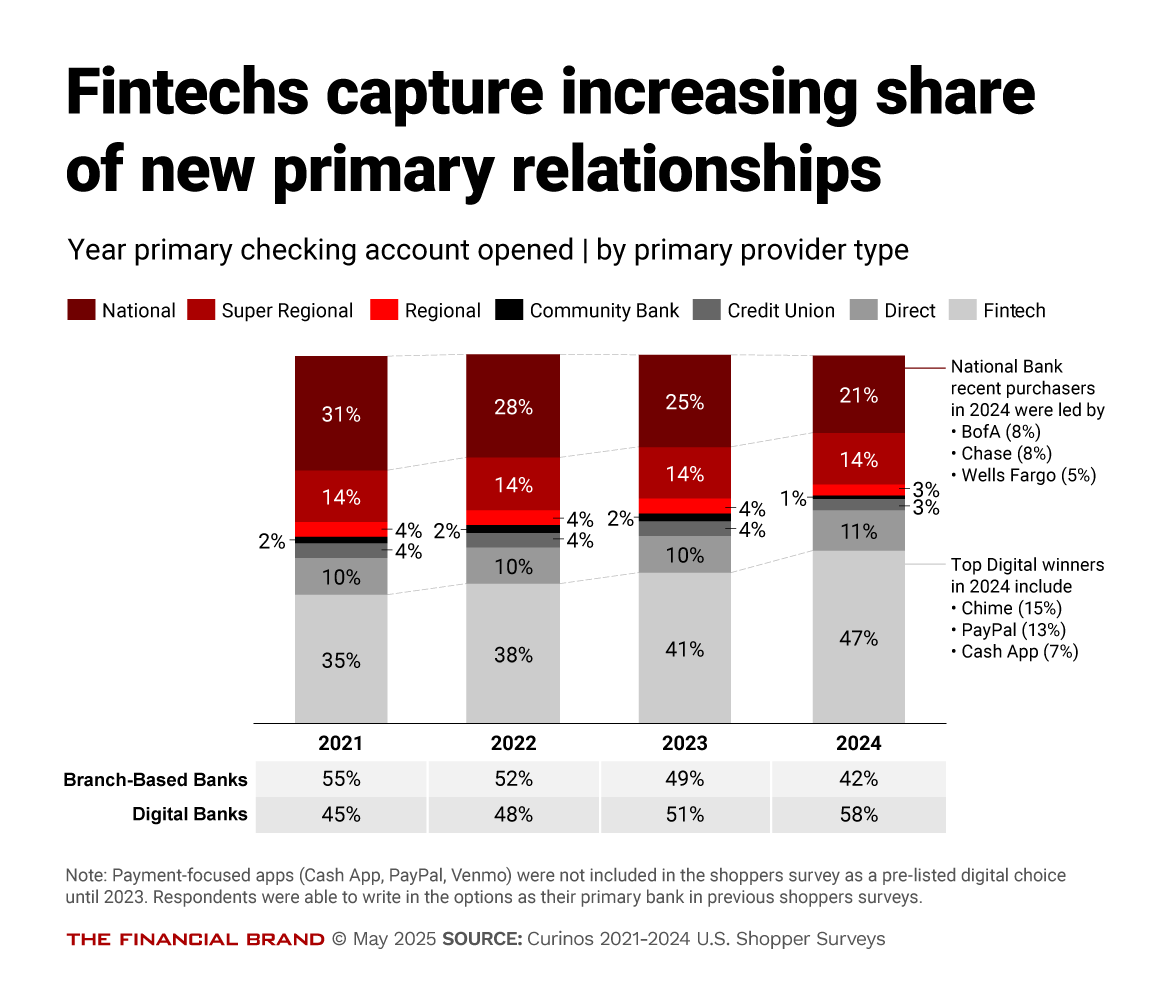

As shown in the chart below, fintechs’ share of checking account openings grew by three percentage points from 2021 to 2022 and again from 2022 to 2023. Hovet says that he expected growth to level out last year, but instead, the growth from 2023 to 2024 came in higher, at six percentage points.

“So, where I thought we might be reaching a cap, instead there was an acceleration,” says Hovet.

Another trend is the flip, beginning in 2003 and continuing into 2024, where digital banks picked up share of switchers and new-to-banking accounts more often than branch-based banks. Still, Bank of America and Chase, which still lean into branches, were leaders among national banks in picking up new accounts.

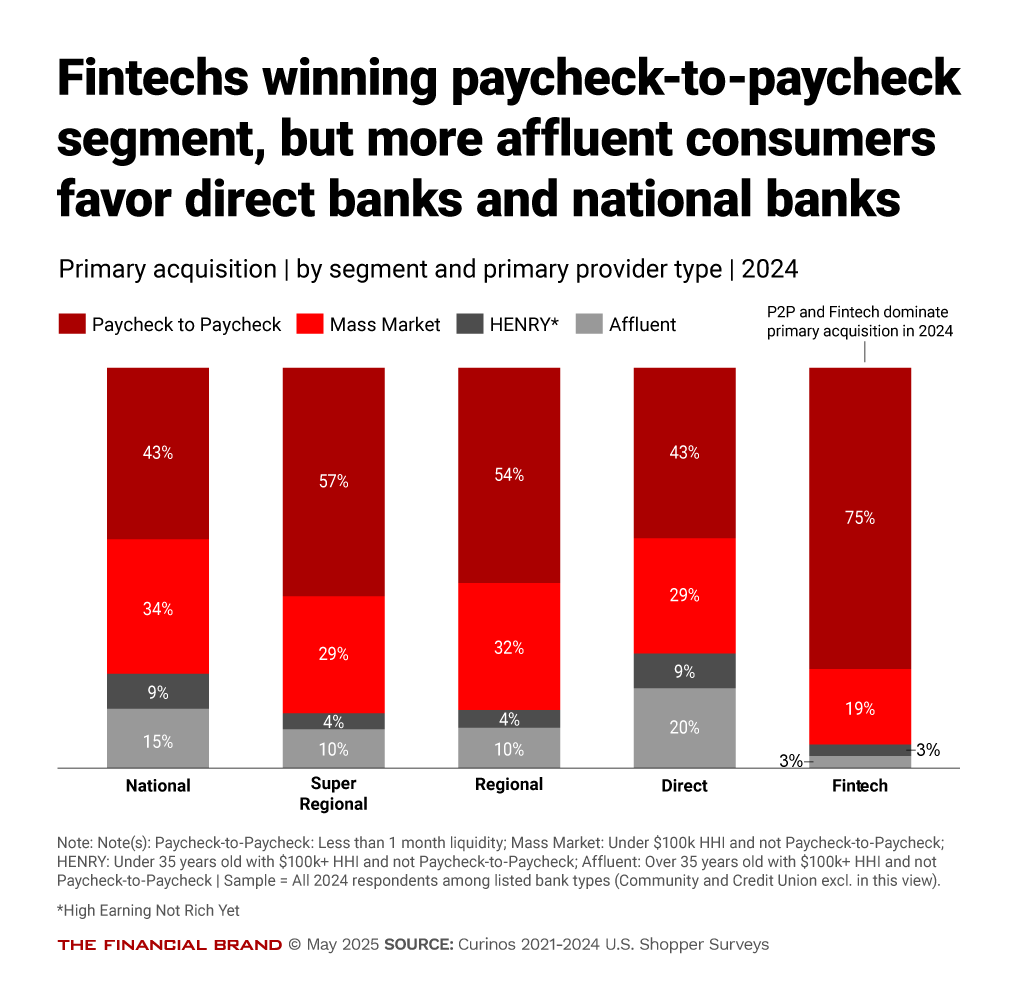

Looked at in another way, by customer segment, the Curinos research found that fintechs dominated the paycheck-to-paycheck segment, while direct banks and national banks had greater success among the smaller pool of affluent customers and HENRYs.

Hovet says further evolution is underway among fintechs that could widen their appeal both among their more traditional base as well as more affluent consumers.

“While fintechs are not yet winning with the affluent, they’ve been focused on a particular segment with a particular set of needs, and they’ve been able to deliver against those needs and win,” says Hovet. This should be taken as a warning among traditional players.

“You’re already seeing some of the fintechs start to get into offering credit, which is important even for a paycheck-to-paycheck consumer,” says Hovet. This builds out the fintechs’ value proposition, he continues, and can broaden the base they appeal to, especially in a period when more consumers seem to need more credit.

A taste of the future is SoFi, Hovet suggested. The company started as a fintech but picked up a bank charter via acquisition, and Curinos considers the branchless organization a direct bank, rather than a fintech. Yet Hovet says SoFi has a broad product base, including various forms of credit, and has been doing well attracting both affluent consumers and HENRYs.

As payment-based fintechs begin to move beyond that narrow product approach, he says, they’ll likely pick up more appeal.

Read more: They Said It Couldn’t Be Done: Fintechs Gaining in the Race for Primacy

The Economic Wild-Card Looming Over Account Movement

Hovet believes that fintechs will maintain at least the same range of growth through 2025. However, there is one scenario in which things could go differently.

If the country tips into a recession, Hovet says, fintech growth could be interrupted. In the event of the Covid recession, “the switching rate slowed because there was a lot of uncertainty, and so many people stuck with their existing providers. However, as we came out of the depths of the pandemic, we saw an acceleration of switching,” says Hovet. Some of this appeared to be the result of fintechs adding extra features at that time.

“Too much bad news actually slows switching,” says Hovet. But banking institutions have to watch out for the potential fintech rebound that could follow, if history is a guide.

Hovet anticipates that some fintechs might experiment with adding physical locations, in a limited way, to their mix. However, he doesn’t see that step as a make-or-break for their growth.

Read more: Credit Unions May Have Problems Brewing Among Millennials and Generation Z

How Banks and Credit Unions Can Counter Fintechs’ Rising Tide

Competing against fintechs demands that banking institutions sharpen their understanding of what their own business plan is, according to Hovet.

• Be really clear about who your target segment is.

“You might be happy to open accounts from all takers,” says Hovet, “but who are you designing products for?”

Many institutions still seem to want to be all things to all people, Hovet observes, but their focus has to be tighter to win key segments.

• Understand what your institution’s value proposition is.

What is the reason people should want to bank with your organization? “You need to get really crisp around that,” says Hovet, because it leads into his third point.

• Don’t spread your investments too thinly.

“Many financial institutions spread their investments like peanut butter over too much bread,” says Hovet. They don’t necessarily differentiate when spending on marketing, branching and more, to adapt to the segments they say they are aiming to win.

Read more: 4 Key Takeaways from Chime’s IPO Filing That Signal Bank-Like Ambitions