Get Ready for the Next Banking Generational Shake-up

Multiple generational cohorts will hit key financial milestones between 2025 and 2030, creating many opportunities for financial institutions. But sorting, prioritizing and orchestrating the divergent strategies appropriate to so many groups will be challenging.

By David Evans, Chief Content Officer at The Financial Brand

Simple Subscribe

Subscribe Now!

The report: Generation Next: Key Generational Insights for Retail Banking

Source: Experian

Why we picked this report: As noted in the report, several key demographic groups will all hit critical inflection points in the next five years — whether it’s expanded access to credit, or the transitions to homeownership and retirement. Banks and other financial institutions need to prepare their products and platforms now to capture new customers in these moments of truth.

Executive Summary

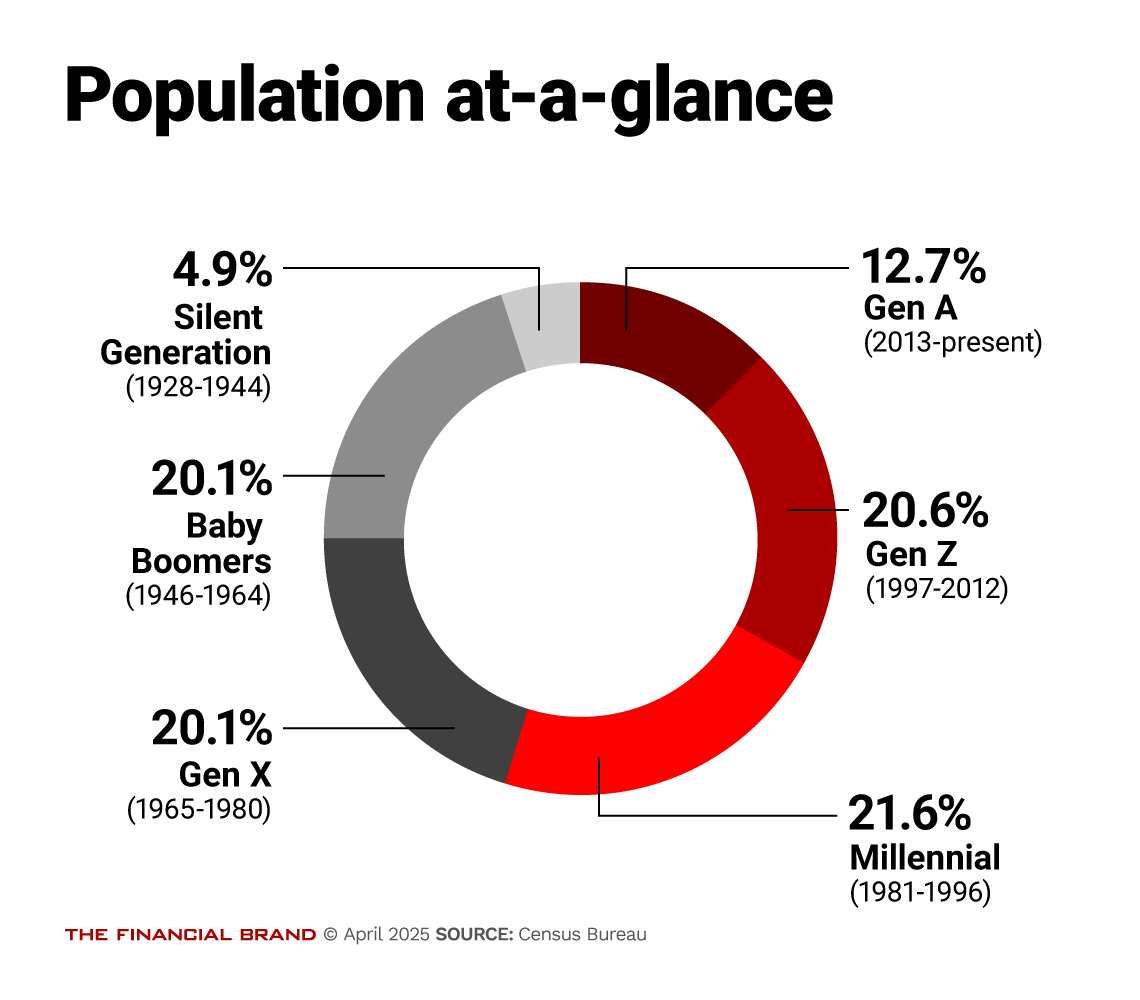

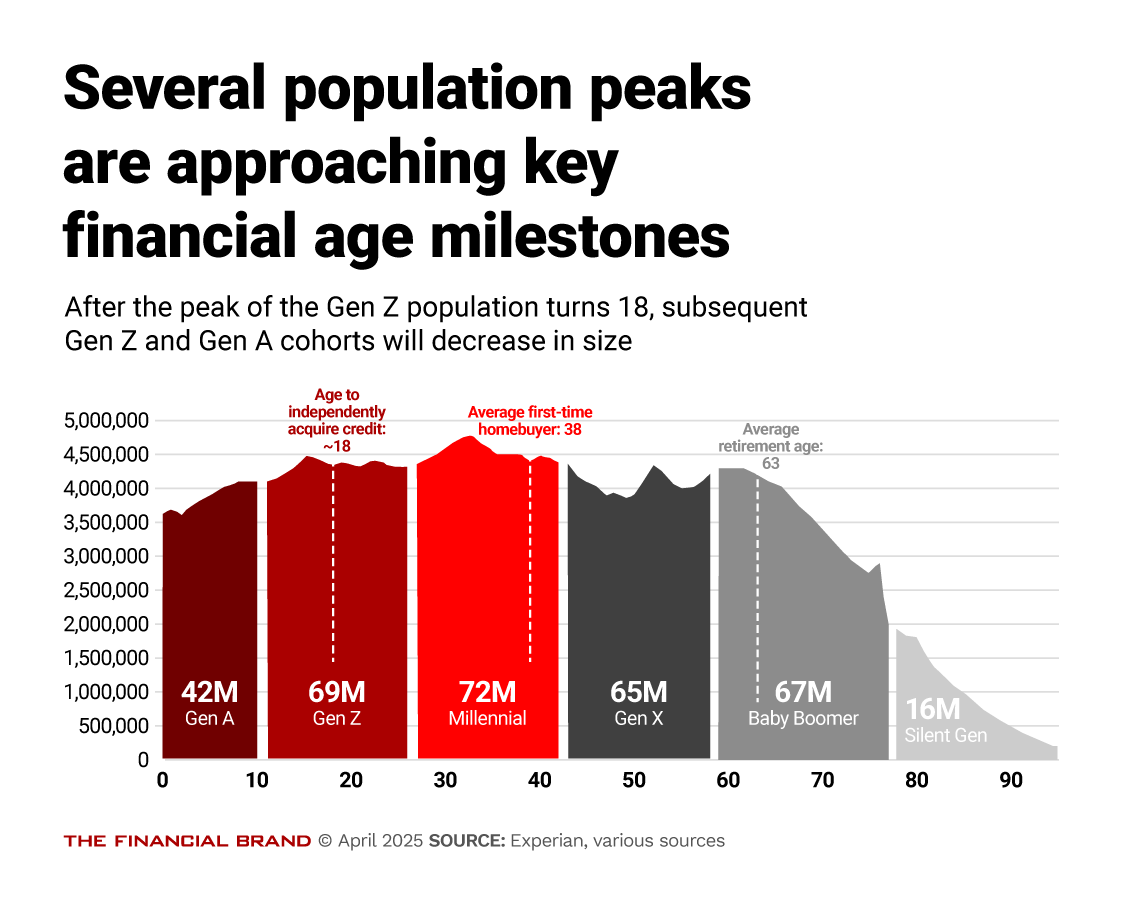

As declining birth rates continue to limit natural population growth, retail banks face a demographic landscape that will soon rely entirely on net immigration for expansion. Meanwhile, the next five years represent a critical window for several key financial milestones: the largest Gen Z cohorts will turn 18 and become eligible for independent credit acquisition; the most populous millennial groups will reach average first-time homebuying age (38); and significant Baby Boomer and oldest Gen X segments will approach average retirement age (63).

Each generation exhibits distinct financial behaviors and preferences, with digitalization preference decreasing with age while credit utilization peaks with Gen X. To capitalize on these shifts, retail banks must develop generation-specific strategies that address unique preferences in product offerings, marketing channels, and service delivery models.

Key Takeaways

- Net immigration will become the sole source of population growth by 2033, making immigrant consumers increasingly important to retail banking strategy.

- Gen Z shows strong digital banking preference but surprisingly values ATM availability highly when choosing banking relationships and is more likely to lose track of financial products due to engagement with multiple institutions.

- Millennials’ assets are growing at the fastest rate among all generations, driven by real estate acquisition as they reach peak home-buying age, despite challenging market conditions.

- Gen X, who spend more than any other generation, also lead in credit utilization and hold the greatest credit card balances, representing a prime target for lending products.

- Baby Boomers, now at retirement age, increasingly value human interaction in banking, with 64.4% rating it “extremely” or “very” important, compared to only 47.1% of Gen Z.

Key Data Points

- Over 21 million people will turn 18 in the next five years (2025-2030), creating a significant wave of new potential banking customers.

- Nearly 11 million non-homeowners will reach the average first-time homebuying age over the next five years.

- Almost 21 million people will reach average retirement age (63) in the next five years, requiring specific financial services.

- Credit cards are increasingly the first credit product acquired (46% of new borrowers), with retail cards continuing to decline in popularity.

- The percentage of unbanked households has decreased across all age groups since the pandemic, creating opportunities for financial inclusion.

What we liked about this report: It’s a comprehensive, data-driven examination of the evolving needs and priorities of key demographic markets. It is also one of the few reports we have seen that looks squarely at the implications of overall future population growth — or more precisely, the lack thereof.

What we didn’t: The sheer volume of individual data points sometimes hides surprising insights (Gen Z likes ATMs!) among a thicket of more obvious observations (baby boomers are spending more on healthcare than younger generations). The point-by-point presentation may also encourage readers to pick and choose data that aligns with their own preconceptions, while ignoring others.

How Population Trends Will Reshape Banking Priorities

Current demographic projections indicate U.S. population growth will steadily decline for the foreseeable future, with deaths expected to exceed births by 2033. This fundamental shift means net immigration will become the sole driver of population growth — a trend that has significant implications for retail banking strategies.

The imminent demographic transitions create both challenges and opportunities. The largest cohorts of Gen Z will reach credit eligibility age (18) over the next 1-2 years, representing a substantial influx of potential new banking customers. However, due to declining birth rates, subsequent Gen Z cohorts will be progressively smaller, meaning this wave of new customers will peak before tapering off.

Simultaneously, the most populous millennial cohorts will approach the average first-time homebuying age of 38 within the next five years. This presents a substantial opportunity for mortgage lending, despite the challenging housing market conditions that make homeownership particularly difficult for first-time buyers.

For Baby Boomers and older Gen X, the next five years will see the largest cohorts reaching average retirement age (63). This transition is happening earlier than in previous generations, with labor force participation rates for those 55+ declining notably since the pandemic and fewer workers expecting to remain employed past age 62.

Dig deeper:

- Why Banks Should Stop Chasing Youth and Target Aging Americans Instead

- Young Americans Have Never Been Wealthier — Or More Stressed. Can Banks Help?

- 5 Key Demographic Trends for Bank Marketers to Watch in 2025

Generation-Specific Financial Behaviors Will Drive Service Needs

Each generation exhibits distinct financial behaviors that should inform banking strategies. Gen Z demonstrates strong preferences for digital banking options, particularly mobile banking and contactless payments. However, they paradoxically rate ATM availability as their top factor when choosing a new bank, indicating that access to cash remains important despite digital preferences. Gen Z is also more likely to lose track of financial products and services due to interactions with multiple financial institutions.

Millennials are entering their prime asset-accumulation phase, with their financial assets growing at the fastest rate of any generation. This growth is particularly pronounced in real estate assets as they reach peak homebuying years. With millennials comprising the largest generation by population (21.6%), their financial behavior will significantly impact banking trends. They lead in first-time home buying, while also showing strong preference for digital banking options, especially among younger cohorts.

Gen X expenditures exceed other generations annually, and they demonstrate the greatest credit utilization. They hold the highest average credit card balances ($9,951) and direct a greater share of their spending toward personal insurance and pensions than other age groups. Their approach to banking blends digital preferences with traditional services.

Baby Boomers, with significant cohorts at or near retirement age, show greater preference for human interaction in banking. They’re more likely to value physical bank branches for learning about new products and services, and they allocate a greater share of expenditures to healthcare than younger generations.

Digital Transformation Powered by Generation-Specific Strategies

From digital-first to balanced channel strategies Banking preferences vary significantly across generations, requiring retail banks to develop nuanced, multi-channel approaches. While mobile banking has become the predominant account access method across all age groups, the margin of preference diminishes with age.

For Gen Z (15-24 years), mobile banking dominates at 76% preference, with all other channels falling below 10%. This generation researches financial products primarily through internet searches (55.8%), word-of-mouth (54.7%), and bank websites (52.3%). They show strong affinity for digital tools, with credit cards increasingly becoming their first credit product (replacing retail cards), and they demonstrate the highest usage rates of Buy Now, Pay Later services.

Millennials (25-44 years) show a similar preference for mobile banking, but at slightly lower rates than Gen Z. Their research behavior differs, with bank websites (69%) taking precedence over internet searches (60%). Younger millennials closely mirror Gen Z’s digital preferences, while older millennials show more balanced channel usage.

Gen X (45-54 years) maintains strong mobile banking preference (54%) but uses other channels more substantially than younger generations. This generation bridges the gap between digital-first approaches and traditional banking methods, with bank websites (67.2%) as their primary research method.

Baby Boomers (55+ years) demonstrate the most balanced channel preferences. While mobile banking still leads (40%), online banking (26%) and ATM/kiosk usage (16%) represent significant portions of their banking interactions. They strongly prefer bank websites and physical branches for learning about new products and services, with 64.4% rating human interaction as “extremely” or “very” important in their banking experience.

Building generation-specific engagement strategies To effectively serve this diverse generational landscape, retail banks should develop tailored approaches that align with each cohort’s unique preferences.

For Gen Z, banks should emphasize mobile-first experiences with seamless integration across digital touchpoints. Educational resources around credit building are particularly valuable as this generation begins their financial journey, with special attention to helping them manage multiple financial relationships. Marketing efforts should span digital channels while recognizing ATM availability remains surprisingly important to this generation.

With millennials entering prime asset accumulation years, banks should focus on mortgage products that address first-time homebuyer challenges, including innovative financing options that make homeownership more accessible despite market conditions. Digital tools that support financial goal setting and tracking will resonate with this generation, which is increasingly focused on building wealth through both real estate and other financial assets.

Gen X represents a prime opportunity for lending products and insurance services. As the generation with the highest expenditures and credit utilization, they value efficiency and convenience across both digital and traditional channels. Comprehensive financial planning tools that address their dual concerns of supporting children and preparing for retirement are particularly valuable.

For Baby Boomers, banks should maintain a strong human element in their service model while providing digital options. This generation values the availability of in-person assistance, particularly for complex financial decisions related to retirement. Marketing efforts should include traditional channels like physical branches and direct mail alongside digital touchpoints.

By recognizing and addressing these generation-specific preferences, retail banks can position themselves to capture key demographic opportunities during this period of significant transition, driving growth despite the challenging demographic landscape ahead.

Editor’s note: This article was prepared with AI language software and edited for clarity and accuracy by The Financial Brand editorial team.