How Consumer-Permissioned Data Must Anchor Banking Strategy in 2026

By Jessica Kendall, Senior Director, Content, MX

Simple Subscribe

Subscribe Now!

Need to Know:

- Data inertia is widespread. More than 60% of financial services organizations say they still use data the same way they always have, while 39% say data usage hasn’t been a top priority.

- Poor data practices are costing customers. 44% of industry leaders report losing customers due to poor data usage, and 45% have lost customers due to weak personalization.

- Consumers expect to be known. 61% of consumers expect their financial provider to understand them—not just show transaction history and account balances.

Every financial provider’s strategic plan for 2026 ultimately hinges on one thing: data. More specifically, financial providers need to take the consumer-permissioned data available to them and use it. When used effectively, data becomes the multi-tool that fuels every part of a modern strategy. It can power product innovation, enable personalized insights, uncover new growth opportunities, and strengthen outcomes for both consumers and the businesses.

This isn’t a new concept. But, the power of consumer-permissioned data remains largely untapped. Last year, a Forrester Consulting report commissioned by MX found that more than 60% of respondents say their organization largely still uses data the same way they always have. At the same time, 39% say that the way they use consumer financial data has not been a top priority for their firm.

And, leaving consumer-permissioned data untapped isn’t just a missed opportunity. It can lead to lost customers and lost revenue. The Forrester research found that 44% of financial services industry leaders and decision makers in the U.S. and Canada say they have lost customers due to poor data usage. And, 45% say they have lost customers due to poor personalization.

Here’s 3 reasons why consumer-permissioned data needs to be at the center of your 2026 strategic plans:

Want more insights like these? Check out MX’s content hub: Data in Action

1. Data Powers New Innovations

Key insight: If data is siloed, inaccurate, confusing, or outdated, financial providers cannot capitalize on emerging technologies to drive new innovations or deliver the experiences that customers expect and demand. Take artificial intelligence (AI) for example. Huble’s AI Data Readiness research found 69% of companies say poor data limits their ability to make informed decisions — and 45% report that unstructured, fragmented data is the biggest barrier to AI success.

Data in determines the quality of data out. Financial institutions need to have a strong data foundation to enable AI use cases — and prevent use cases that could cause inadvertent harm. Done right, AI can fuel the next wave of intelligent, automated services and products to meet customer expectations and business needs. So, if AI is a destination on your organization’s 2026 roadmap, recognize that the road to AI is paved with data.

2. Consumer-Permissioned Data Unlocks New Growth Opportunities

Don’t ignore the consumers: By tapping into consumer-permissioned data, financial providers can gain a more accurate and dynamic understanding of customer needs. This understanding can enable them to drive measurable results for both their customers and businesses.

This includes everything from acquiring new customers and driving engagement to uncovering new growth opportunities. Data-driven insights enable financial providers to:

- Better identify and acquire new customers

- Deliver hyper-personalized experiences that resonate with each customer

- Predict and prevent customer churn

- Improve customer satisfaction and deepen loyalty

3. Consumers Want Data-Driven Experiences

The writing on the wall: Most importantly, consumers want a provider that understands how to help them. MX research found that 61% of consumers expect their financial provider to know them. It’s no longer enough to give them basic information about transaction history and account balances. They want someone who understands their unique financial life, goals, and struggles.

Other research shows a majority of younger generations expect this level of personalization. Seventy-two percent of Gen Z expect banking tailored to their goals, while 55% of Millennials want a more personalized digital banking experience.

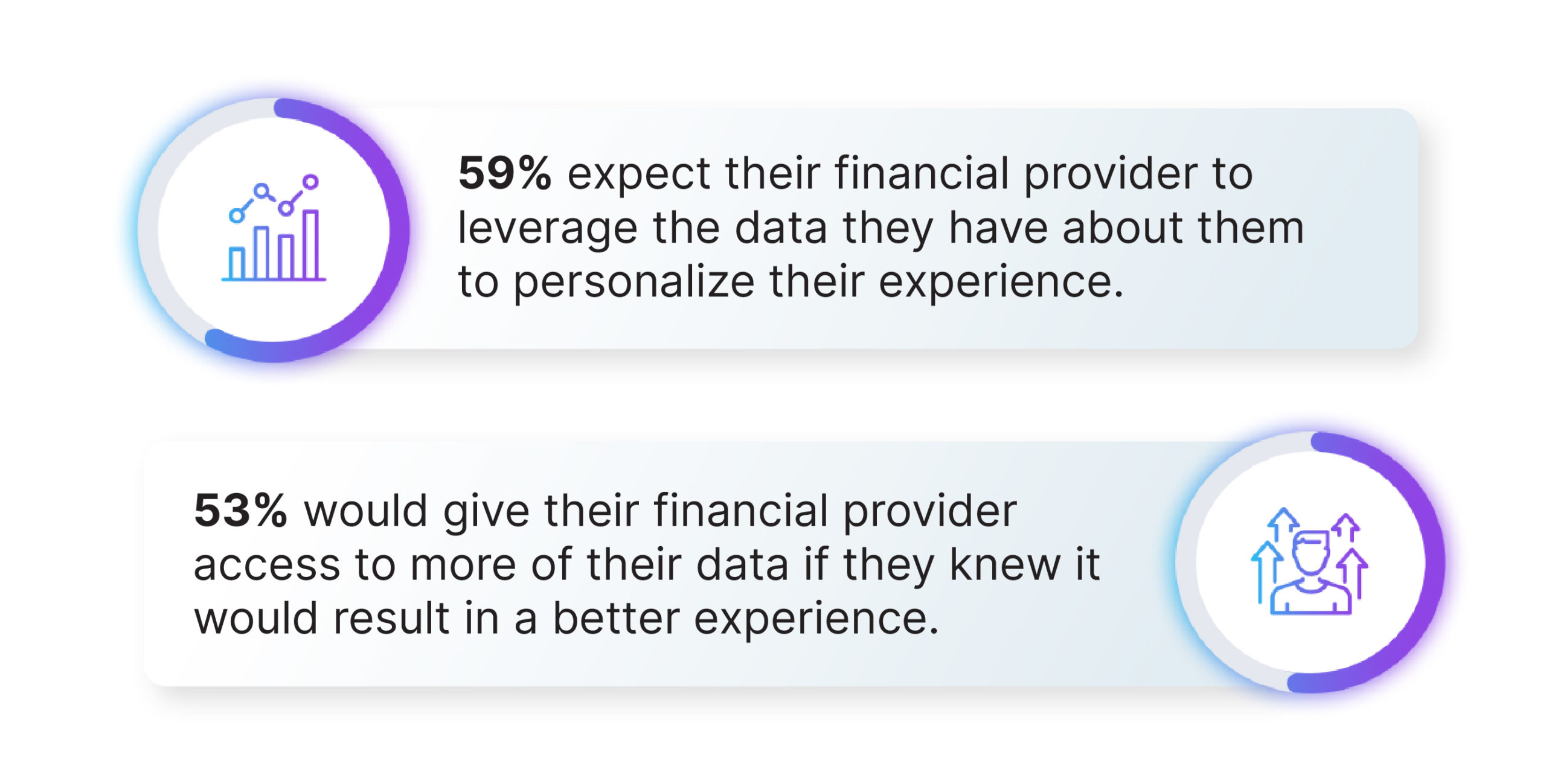

What’s more, consumers will give financial providers even more of their data if they believe it will result in these better experiences. MX research shows 53% of consumers say they would give their institution access to even more data if it delivered better experiences, stronger insights, or more relevant guidance.

In 2026, financial providers who prioritize data will win the loyalty of their customers and drive meaningful growth for their business. And, those that don’t risk falling behind and losing customers along the way.