What’s Collapsing Banking M&A Deal Value? One Word: Data

By James White, Vice President of Growth and Market Strategy at Engage FI

Simple Subscribe

Subscribe Now!

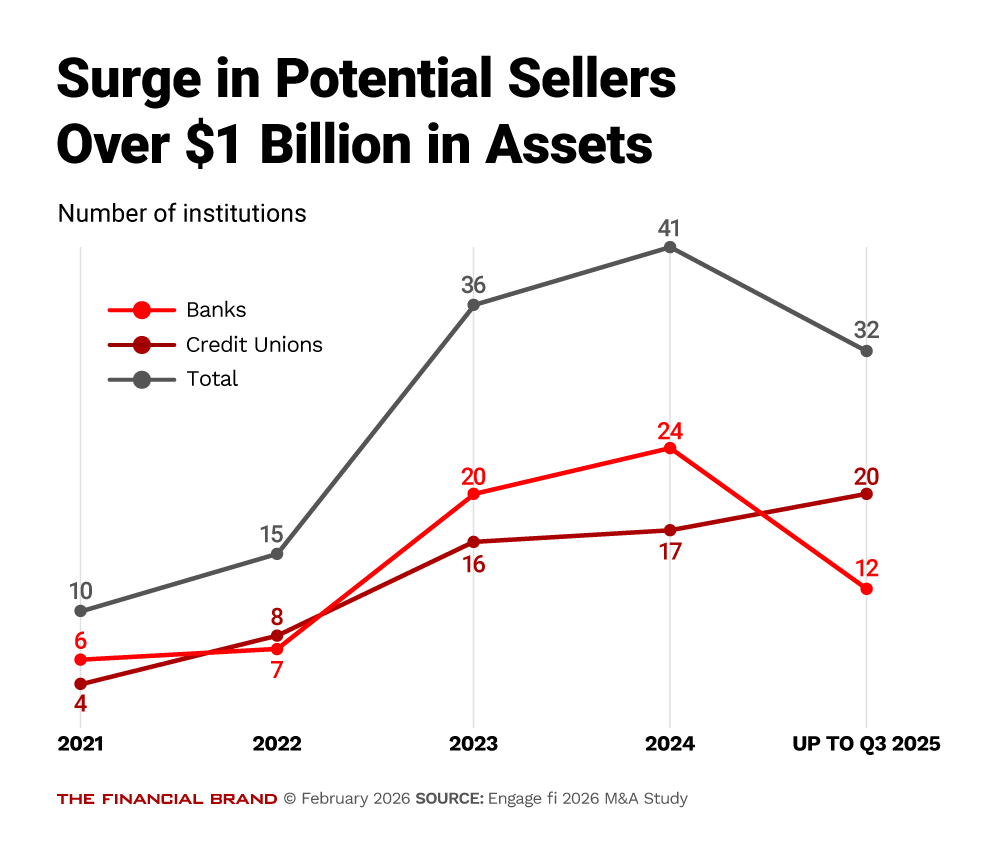

The number of large community banks and credit unions with high-pressure-to-sell indicators has ballooned over the last five years, from just 10 to over 30 institutions. What’s more, nearly 10% of all banks and credit unions now have financials consistent with being acquired within 18 to 36 months.

But does that mean the M&A market is a major opportunity in 2026? Not necessarily.

Reality check: According to a new study published by Engage fi, the current pressure-to-sell atmosphere does offer a larger pool of targets, some of them quite large in asset size. But financial stress has also put these institutions in a “running out of oxygen” scenario in which they cannot invest in growth and technology. The larger the sellers are, the larger the challenges they can pose for post-merger success, especially in terms of technology.

Success in today’s target-rich environment won’t be about finding targets; there are many. It will be about what happens afterwards, especially when it comes to data, core data in particular.

Here’s why.

A Target-Rich Environment?

The number of institutions with $1 billion or more in assets that show high pressure to sell has grown steadily over the past five years, including those with $10 billion or more in assets, and even one with more than $20 billion in assets.

This group of high-pressure-to-sell institutions, now numbering 32 banks and credit unions as of the latest available regulatory data, has financials consistent with being acquired within 18 to 36 months.

They are flanked by a broader group of institutions with assets below $1 billion that face high pressure to sell. That segment has also ballooned in population over the past five years.

Of the 8,837 banks and credit unions studied, 865 had high pressure to sell. Some 651 are credit unions (14.7% of the 4,417 credit unions analyzed), and 214 are banks (4.8% of the 4,420 banks analyzed).

The study defined ‘pressure to sell’ using five years of trended FDIC or NCUA (2021 – Q3 2025) data back tested against 74 mergers announced in 2025. The model correctly identified stress signals in acquired institutions months before deals were announced.

Engage fi found two types of pressure to sell. There were 764 institutions on the ‘watchlist,’ meaning they may not have the financial wherewithal to spend on growth and on the investments (particularly in technology) at the same time. They are succumbing to the scenario in which independence becomes less appealing to boards.

Another 101 banks and credit unions are nearly out of oxygen, defined as “highly likely” to sell. They have so much strain that a sale or merger is increasingly no longer optional. Technology cannot be maintained at these institutions, even though it holds the data that underpins their franchise value.

Sellers’ troubles today are technology troubles. And those are expensive to deal with. Buyers are also likely to face competition and upward price pressure on the deals they close.

Heavy Buyer Competition

While 865 institutions face seller pressure, 1,736 qualify as buyer candidates based on size and financial strength, according to Engage fi’s analysis. These represent institutions with balance sheet capacity and strategic positioning to pursue acquisitions.

Some 806 credit unions are buyer candidates. Within this pool, 81 institutions rank in the top decile for buyer readiness, based on profitability, efficiency, net worth ratios, and growth momentum.

Some 930 banks are buyer candidates as well, with 93 institutions scoring in the top decile on buyer readiness. Their median assets are $2.23 billion, and they show greater capacity to acquire larger target institutions.

Given these dynamics, the ratio of seller-pressure organizations to buyer candidates suggests an active M&A market with two buyers for every seller. Sellers should easily find two buyers willing to compete. Depending on the market, they could find more.

Risks to Successful Acquisitions

With so many potential sellers that may not have invested in technology for years, post-merger migrations become a significant risk to a successful acquisition. As an acquirer, if you can’t preserve the seller’s data when moving it onto your systems, what did you buy? It can become like buying a car and never receiving the keys.

Every depositor or borrower, every staff member, and even the board and ownership depend on the organization’s data as its record of all its relationships. It literally determines an acquirer’s ability to benefit from all the seller’s data across its payment processing, accounts payable, digital and mobile banking, and transactions.

Executives know the value of their data well. If high-pressure-to-sell organizations are struggling with technology and data, they also know what that means for post-merger projects. An acquirer cannot afford to get a data migration wrong. But can it afford the cost of getting it right? Perhaps not without sacrificing the economies of scale that made the acquisition appealing in the first place.

Many data migration projects “fail to meet their timelines or are entirely aborted, often exceeding budgets by an average of $0.3 million per data set,” according to KPMG.

That last part is important: per data set. “Given that a typical M&A deal can involve dozens of data sets, these costs can quickly add up, making data migration a significant financial concern,” the firm reports. “Over 40% of these projects encounter such issues.”

The larger the target institutions, the more systems, silos, and data an acquirer must ingest, and this math can get brutal when it comes to a transaction’s benefits.

How to Preserve Franchise Value

Buyer competition pushes valuations up. But large volumes of tech-troubled institutions may push it too high for the economics to work.

If an institution goes over budget by $0.3 million per data set, the cost of acquiring an institution with “dozens” of data sets compounds. Miss targets on just 10 data sets, and an acquirer is already staring at about $3 million in budget overrun – if costs follow the average.

That’s before you account for productivity taxes on teams stuck reconciling data, and it assumes there are only 10 data sets.

What it means: That math of data migrations can either evaporate deal economics, thus requiring acquirers to incorporate the cost into their bids. Or they must find a way to avoid spending so much on migrating data and systems. The former option may make the institutions less competitive in a market where every seller potentially has two buyers. The economics and practicality of bank-buying point in one direction:

Acumen in data migration is becoming the best way for buyers to win deals that realize their full value after all the cost, effort, and disruption are accounted for. It is how institutions use M&A now to grow and become better organizations in the process.