Banks Are Swimming in Data But Starving for Insights. AI Will Make Things Worse

As AI reshapes every industry, what was once just embarrassing inefficiency for banks is fast becoming a critical failing. Data-blind institutions won't just fall behind; they'll fall off the map. The countdown has started.

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Many gurus have highlighted the opportunities for banks that figure out how to tap the value of their data. But new research indicates that many institutions are only halfway — or less — to where they should be. Worse, the same report suggests that the price of a bank not getting its data act together will soon become prohibitive.

A new study by Cornerstone Advisors asked bank and credit union respondents to rate themselves on 50 factors spanning five categories — customer data, market data, operational data, transaction data and data governance — to produce a “Data IQ.” The results are sobering. After years of banks paying lip service to the potential of data analytics, the institutions in the sample, on average, scored only 50 out of a possible 100.

Shortcomings are rife. For example, only 42% of the sample felt that their organizations treat information as a strategic asset. Only 29% said that key business decisions are made in conjunction with “accurate, timely and actionable data.”

Only 17% said that real-time data is “clean, structured and scalable.” And less than one in five indicated that staff have the skills to make data-driven decisions.

And 23% of the sample were unhappy with their institution’s data governance approach.

What makes all this critically important now is the importance of clean, accessible data to keep up with large language models and artificial intelligence generally.

“The banking industry stands at a critical inflection point as artificial intelligence transforms core banking operations, customer experiences, and risk management frameworks,” says Cornerstone in a new report. “Although AI promises unprecedented efficiency gains and competitive advantages, many banking institutions are struggling to bridge the gap between their current data infrastructure and the sophisticated requirements of modern AI systems.”

Ron Shevlin, chief research officer at Cornerstone, says he’s tired of the mantras that have been worn out over data — “data is the new oil,” etc. Many institutions already fall short of what’s needed to make good business use of their data, he says. If they fail to invest now, they will only have to do so down the road. In the meantime, they will miss opportunities, ceding them to competitors who did make the investment.

“It’s a ‘you pay me now or you pay me later’ situation,” says Shevlin. “Do some of the payment now so you can make it easier 12, 24, 36 months from now.”

The report, “Improving Your Financial Institution’s Data IQ,” sponsored by Apiture, estimates that $1 million to $2 million must be spent annually for every $1 billion in assets that the institution has.

Some of this money will go to efforts to push the institution forward, but some of it will also be devoted to paying for catch-up.

Paying the Price for Past Neglect

Dan Haisley, chief product officer at Apiture, says that over time, in many banks and credit unions, various data “fiefdoms” evolve. Essential standardization doesn’t happen when data evolves this way, and that gets in the way of interoperability now, and will have even greater effect when AI attempts to access and use data.

“Every department believes they are good stewards of their data, but that the other departments aren’t,” says Haisley. This leads to mistrust of other functions’ data.

Each function often maintains its own approach to organizing and administering data, to the point where the functions don’t share a common “data dictionary” — a technical term for the institution’s approach to content, format and structure of a database and the relationship between its holdings.

Shevlin says this problem goes beyond internal practices. As mainstream core vendors, for example, have expanded through acquisitions of specialized software companies, he says, “they’re not even pulling together common data dictionaries and standards and naming conventions themselves.”

It’s a tech Tower of Babel — yet one that could be fixed.

“It’s more than 20 years ago that Jeff Bezos issued a famous edict at Amazon that every department, division, line of business, etc., had to make its data available through APIs,” says Shevlin. “Can you imagine if banks had done that 20, 25 years ago? We wouldn’t be in this situation.”

In banking, too often such challenges were ignored because top management felt it had checked the box on data. “Yeah, we’ve got the data thing going, we’ve got a data warehouse, and maybe we can pull some reports from it,” they thought, according to Haisley. End of story, and the beginning of today’s undesirable situation.

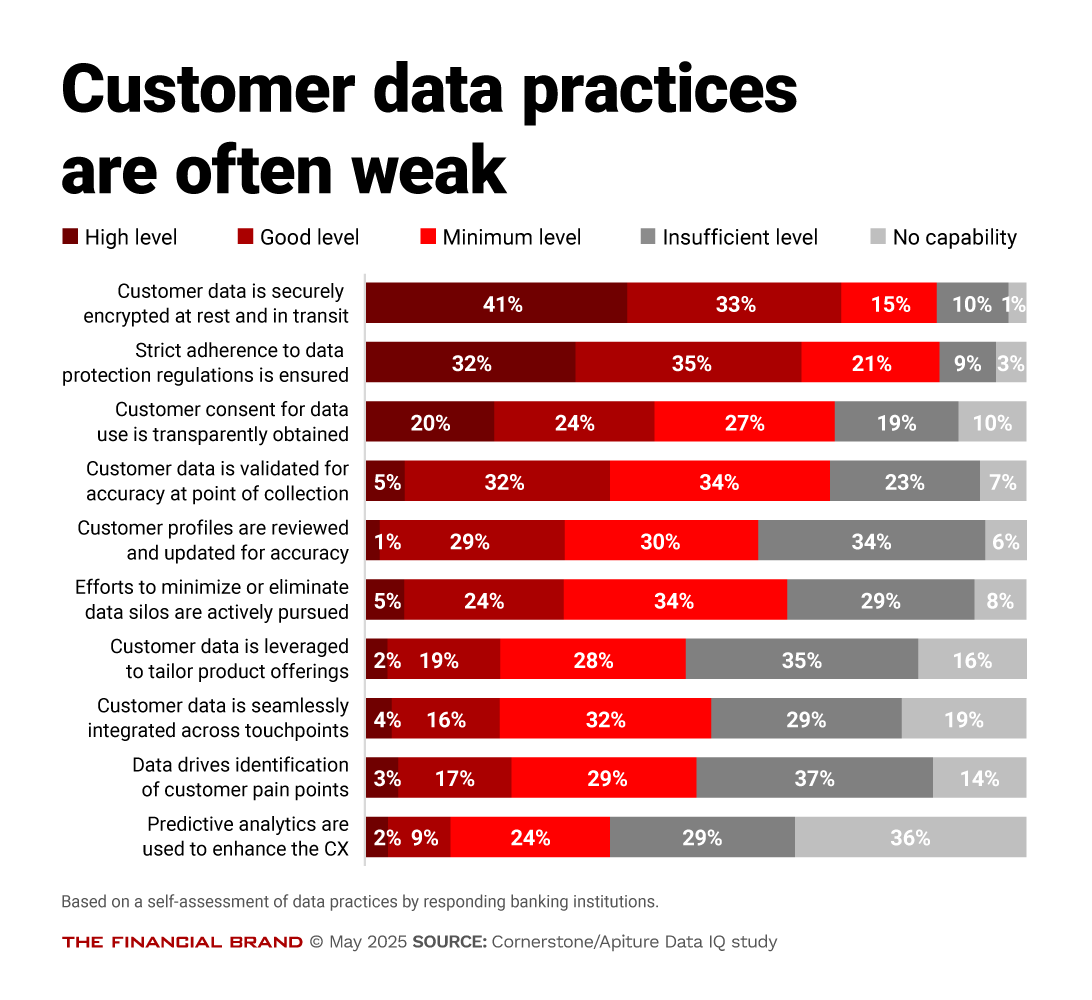

The chart below, from the study, demonstrates an ongoing problem. The first few factors listed are covered by regulations, and, as Shevlin points out, noncompliance isn’t an option. But other practices that could be paying dividends are implemented much less frequently.

Take two factors toward the bottom: “Customer data is leveraged to tailor product offerings” and “Data drives identification of customer pain points.” In both cases, only about one out of five institutions rated themselves as performing at a high or good level. Both functions are typically considered a “good to have” for a bank, yet the execution is lacking.

Similarly, a key aspect of bank and credit union of data practices concerns use of market data — external data that provides context for the institution’s own as well as a view of the world, including competitor information. On the whole, respondents scored themselves lowest in this category.

![]()

“Roughly 4 in 10 execs consider their firms to have at least a good level of capability in benchmarking their performance metrics against market data,” says the report, adding, “Many of us at Cornerstone would dispute that.”

About half of those surveyed lack even minimal capability to analyze customer behavior patterns versus the market. Likewise, they can’t produce market reports that guide the institution’s actions and lack the ability to relay market data to stakeholders.

Read more:

How Low Data IQ Impedes an Ostensible Banking Goal: Personalization

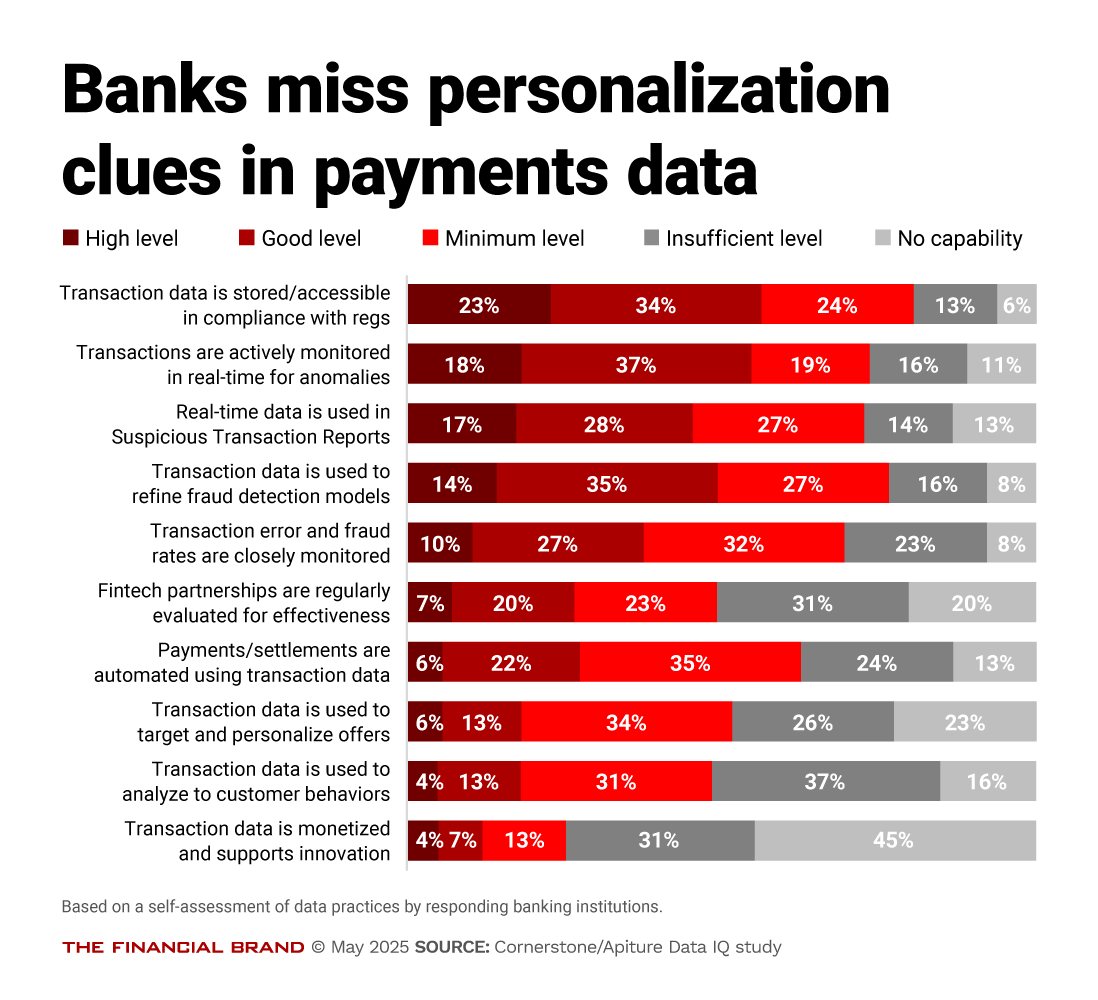

A key goal — or at least one that many in the industry aspire to — is personalization of banking services. Yet when it comes to payments data, which can be a powerful source of customer profiling, few institutions are really doing that.

This doesn’t surprise Haisley and Shevlin. Shevlin adds that most personalization focuses on choosing which existing offers to present to customers. He doesn’t think this is really what personalization in banking should be about.

Instead, Shevlin thinks data should guide communication between the banking institution and the customer.

“The best salespeople can personalize because they are listening to what customer needs are and they customize based on what they hear,” says Shevlin. “We’ve never gotten there in the digital banking world. We are only starting to see the tools become available to do that.”

Haisley says the digital equivalent of that sales approach to personalization will come in the form of applying agentic AI to financial services.

This underscores the urgency for getting an institution’s data in order. That will require concentrated action — ultimately, making it happen has to become somebody’s job.

“From an organizational perspective, many banks and credit unions need to create a position for two or three years to get things moving,” says Shevlin. “The business units will not fix things. They’ll just continue doing what they’ve been doing.”