Modernize Ruthlessly or Surrender the Customer Relationship

By Jessica Kendall, , Contributor at The Financial Brand

Simple Subscribe

Subscribe Now!

Retail banking is at an inflection point, according to Finastra’s Financial Services State of the Nation 2026 report. Artificial intelligence has reached near-universal adoption and modernization investment is accelerating. Payments and lending have become the primary proving grounds for innovation, while personalization has shifted from competitive advantage to baseline expectation.

The report argues that these technology initiatives can no longer operate as parallel workstreams. AI, modernization, and customer experience must converge into a cohesive operating model built on resilience, governance, and execution discipline.

Need to Know:

- AI adoption is effectively universal, but value now depends on governance, explainability, and enterprise-wide integration.

- Modernization spending is widespread, yet talent shortages (43%) and budget constraints (41%) continue to slow execution.

- Payments and lending are the battlegrounds for differentiation, with AI embedded across fraud, underwriting, and workflow automation.

- Personalization is evolving into hyper-personalization, with significant growth in CX budgets and heightened scrutiny around privacy and consent.

AI and Modernization Converge

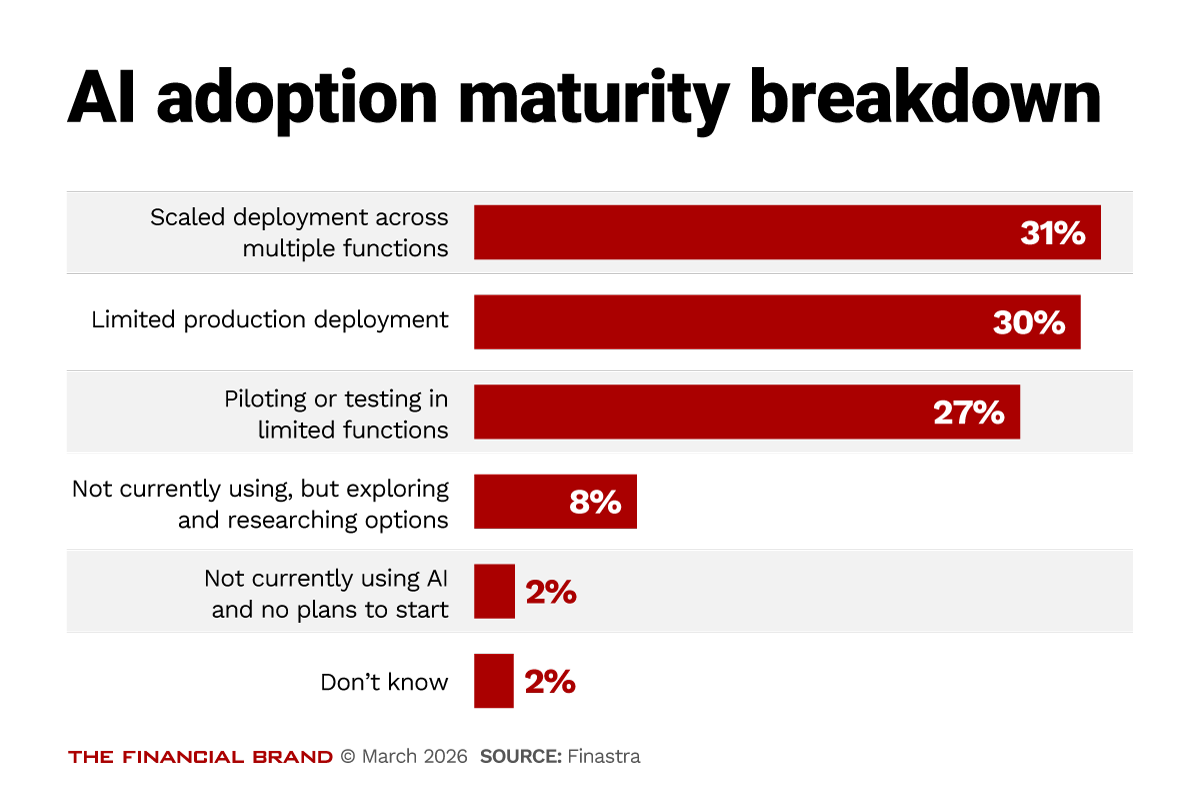

AI has moved from pilot to production at remarkable speed for financial services. According to Finastra’s research, 43% of institutions cite AI as their top innovation lever. The report also shows near-universal adoption of AI in various parts of organizations.

Today, 31% of institutions report scaled deployment across multiple functions, with another 30% in limited production. Only 2% remain firmly on the sidelines with no use of AI and no plans to start. The conversation has shifted from “Should we adopt AI?” to “Where does AI create measurable impact?”

Retail banks are applying AI across fraud detection, underwriting, compliance, workflow automation, and personalization. In different regions, the focus varies based on unique competitive pressures, customer expectations, and operational realities. Regardless, the variation underscores an important point: adoption speed may differ, but strategic intent does not.

However, AI’s effectiveness depends on modern foundations. The report frames modernization across four domains:

- digital transformation,

- cloud adoption,

- data platform modernization, and

- core modernization.

Eighty-four percent of institutions are already using some form of cloud, and nearly nine in ten plan modernization investment in the coming year.

For marketing and business leaders, this convergence matters. Personalized campaigns, real-time offers, and contextual engagement all require clean data, interoperable APIs, and scalable infrastructure. AI layered on fragmented systems produces friction; AI layered on modern platforms produces growth.

Payments and Lending Define Experience

Payments and lending have become the most tangible expressions of innovation, according to the report. AI use cases, real-time payment capabilities, and alternative payment methods are driving the next wave.

In payments, 38% of institutions report improved or deployed AI use cases in the past year, and 35% advanced real-time payments capabilities. That said, the next largest area of payment technologies improvement and deployment was operational resilience improvements (34%) — signaling that speed must coexist with reliability.

In lending, 36% adopted AI assistants or chatbots for training and troubleshooting in the past year, and 35% strengthened fraud, Know Your Business (KYB), and Know Your Customer (KYC) capabilities. Looking ahead to the next 12 months, other priorities include technologies that can accelerate the customer journey: embedded blockchain technology for lending decisioning and approval (29%), integrating workflow automation tools (29%), and automated loan applications (29%).

For retail banking executives, this is where strategy meets customer perception. A personalized marketing message means little if credit decisions stall or payments fail. The front office promise must be matched by back-office performance.

What to do differently:

- Treat payments and lending metrics as customer experience indicators, not purely operational KPIs.

- Integrate fraud and compliance messaging into customer communications to reinforce trust.

- Prioritize real-time visibility across the lending funnel to reduce abandonment and improve conversion.

The institutions pulling ahead are those embedding intelligence directly into transactional journeys, not just surrounding them with digital wrappers.

Modernization: Momentum Meets Friction

While innovation is at the forefront, modernization efforts remain fundamental to success. Eighty-seven percent of institutions expect to invest in modernization over the next 12 months.

Confidence is high — 72% of institutions believe they are ahead of competitors on modernization. But, if most institutions believe they are ahead, competitive advantage may be narrower than leaders assume. And obstacles remain.

Talent and skills gaps are cited by 43% as the primary barrier, followed closely by budget constraints. Regulatory complexity further complicates execution, particularly for mid-to-large institutions operating under heightened scrutiny.

More than half (54%) are leaning on fintech partnerships to accelerate progress. Partnerships provide access to specialized AI, cloud, and security expertise while mitigating hiring challenges. At the same time, data sovereignty concerns — especially pronounced in the U.S. — are pushing some institutions toward selective in-house builds.

It’s clear that modernization is no longer an IT initiative. It is an enterprise capability requiring coordinated governance across marketing, operations, risk, and technology.

Action steps:

- Build cross-functional modernization steering committees that include revenue leaders.

- Establish clear ROI frameworks linking infrastructure upgrades to customer growth metrics.

- Blend partnerships and internal builds based on risk profile and strategic control requirements.

- Modernization succeeds when it is treated as a growth engine, not a cost center.

Personalization Becomes Strategic

According to the report, personalization is now the primary customer expectation. Thirty-eight percent of institutions report that improved service and personalized experiences are their customers’ top demand. The good news is institutions are already meeting some of these expectations. Forty-two percent already provide values-aligned banking and chatbots for instant support. Only 4% offer none of the listed personalization services.

Investment patterns confirm the shift: 30% plan to increase customer experience (CX) and personalization spend by 25% to 49%, while nearly a quarter (24%) anticipate 50% to 74% growth in CX and personalization spend.

Yet concerns over privacy, consent management, and regulations loom large, especially for larger institutions. Nearly half of very large organizations (45%) cite this as their biggest barrier to delivering greater personalization.

What to prioritize:

● Strengthen consent management before expanding personalization breadth.

● Position data stewardship as a core brand attribute in marketing narratives.

● Integrate compliance teams early into CX innovation cycles. Hyper-personalization without governance creates reputational exposure. Hyper-personalization with transparent data practices builds loyalty.

Bottom Line

Retail banking leaders who integrate AI into real operations, modernize with clear growth outcomes, embed security into brand strategy, and personalize within transparent governance frameworks will shape the next competitive cycle.

In this environment, Finastra argues, dependability carries more weight than novelty. And the institutions that operationalize that insight will earn both trust and growth.