Competitive Pressures Are Scrambling Retail Banks’ Priorities in 2025

The 2025 Retail Banking Trends and Priorities Report reveals an industry rebalancing digital transformation with traditional banking. While 51% of institutions implement digital initiatives, 35% plan branch expansion. Key focuses include data analytics, customer acquisition, real-time payments, and AI adoption, with ongoing disconnects between recognized trends and strategic priorities.

By Jim Marous, Co-Publisher of The Financial Brand, CEO of the Digital Banking Report, and host of the Banking Transformed podcast

Simple Subscribe

Subscribe Now!

Financial institutions find themselves at a fascinating junction in 2025, where the paths of digital innovation and traditional banking converge. The latest Retail Banking Trends and Priorities Report unveils a sector navigating complex currents of change, with just over half of institutions actively pursuing digital transformation initiatives.

Yet beneath this headline figure lies a more nuanced reality: while enhancing digital experiences tops the agenda for 52% of organizations, a mere quarter are prioritizing the modernization of legacy systems and back-office operations that make such experiences possible.

This paradox surprisingly extends to the physical domain. Despite digital acceleration, 35% of financial institutions plan to expand their branch networks in 2025 — a figure that rises to an eyebrow-raising 61% among credit unions. Far from contradicting digital ambitions, this hybrid approach appears to be a calculated move to differentiate from digital-only competitors, albeit one that carries significant operational costs.

Download Report: 2025 Retail Banking Trends and Priorities

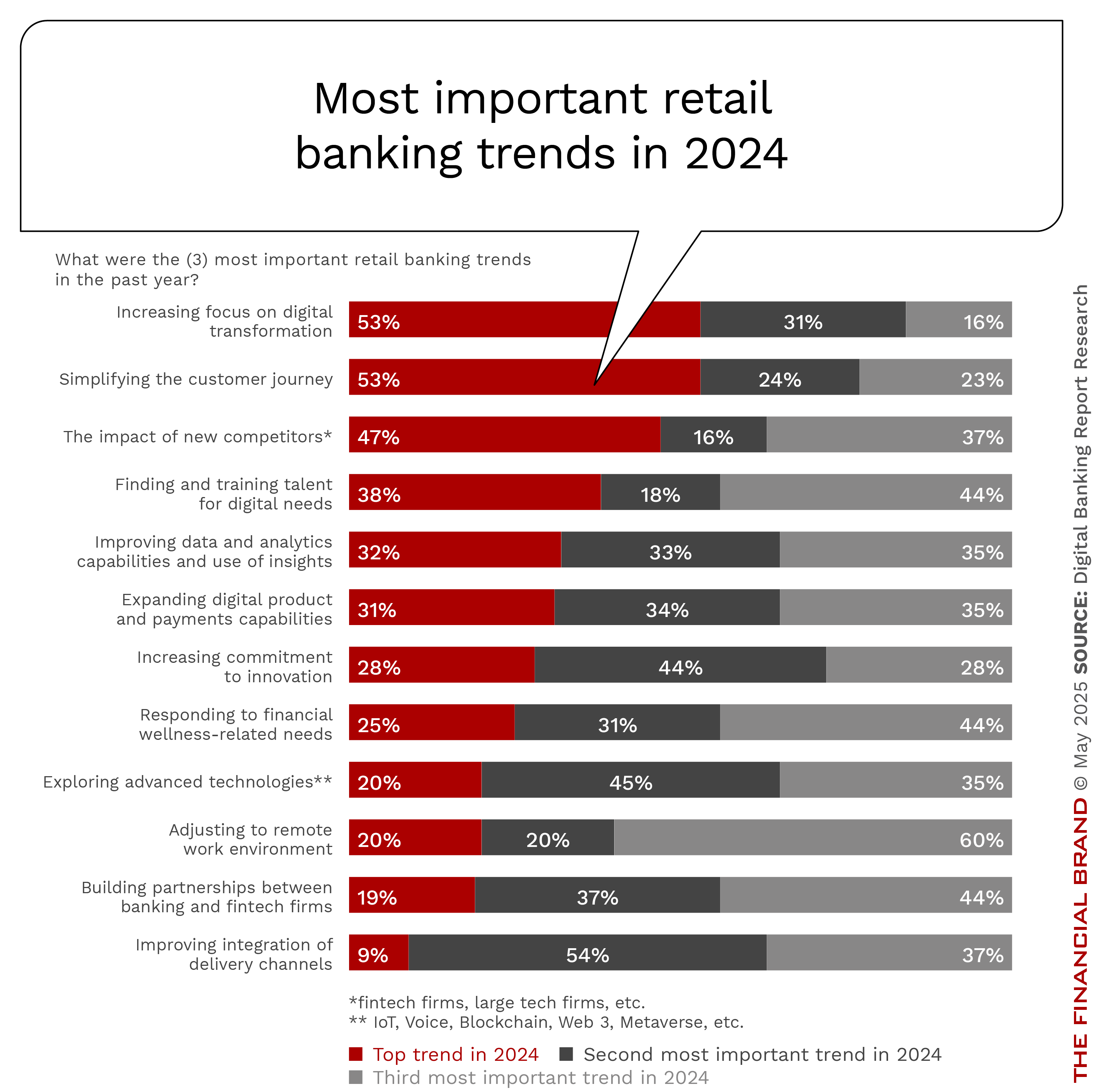

Yesterday’s Predictions, Today’s Reality

The financial services industry’s journey through 2024 reveals how quickly priorities can shift. What began as a year with data analytics at the forefront (predicted by 52% of executives) evolved into one dominated by customer journey simplification and digital transformation, both claiming 53% of executive attention by year’s end.

This dramatic pivot toward customer experience improvements reflects a sector responding to competitive pressures from fintech innovators and rapidly evolving consumer expectations. Banking executives, initially focused on data-driven capabilities, found themselves redirecting resources to streamline customer journeys and accelerate digital transformation timelines as market realities demanded immediate action.

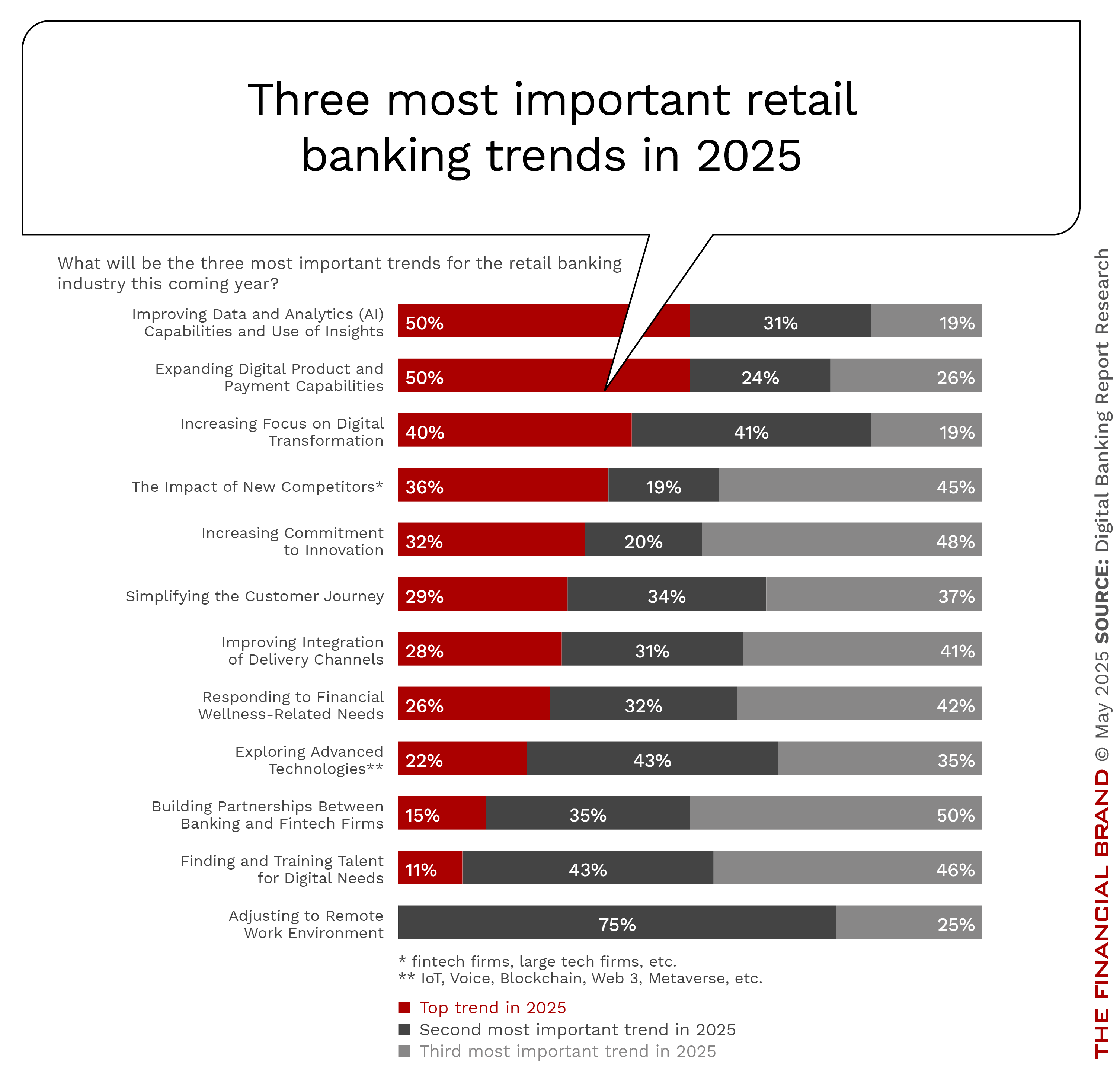

Crystal Ball: The 2025 Banking Horizon

Looking ahead, the industry appears poised for yet another strategic realignment. Data analytics reclaims its throne in 2025 projections, with digital payment capabilities surging alongside it. Digital transformation, while still essential, slips to third place with 40% of institutions naming it their primary focus.

Perhaps most revealing is the precipitous decline in customer journey simplification, dropping from a leading concern to just 29% priority — suggesting a shift from foundational experience improvements toward more sophisticated capabilities. Meanwhile, remote work considerations have vanished entirely from top priorities, indicating a stabilization of work arrangements that dominated pandemic-era planning.

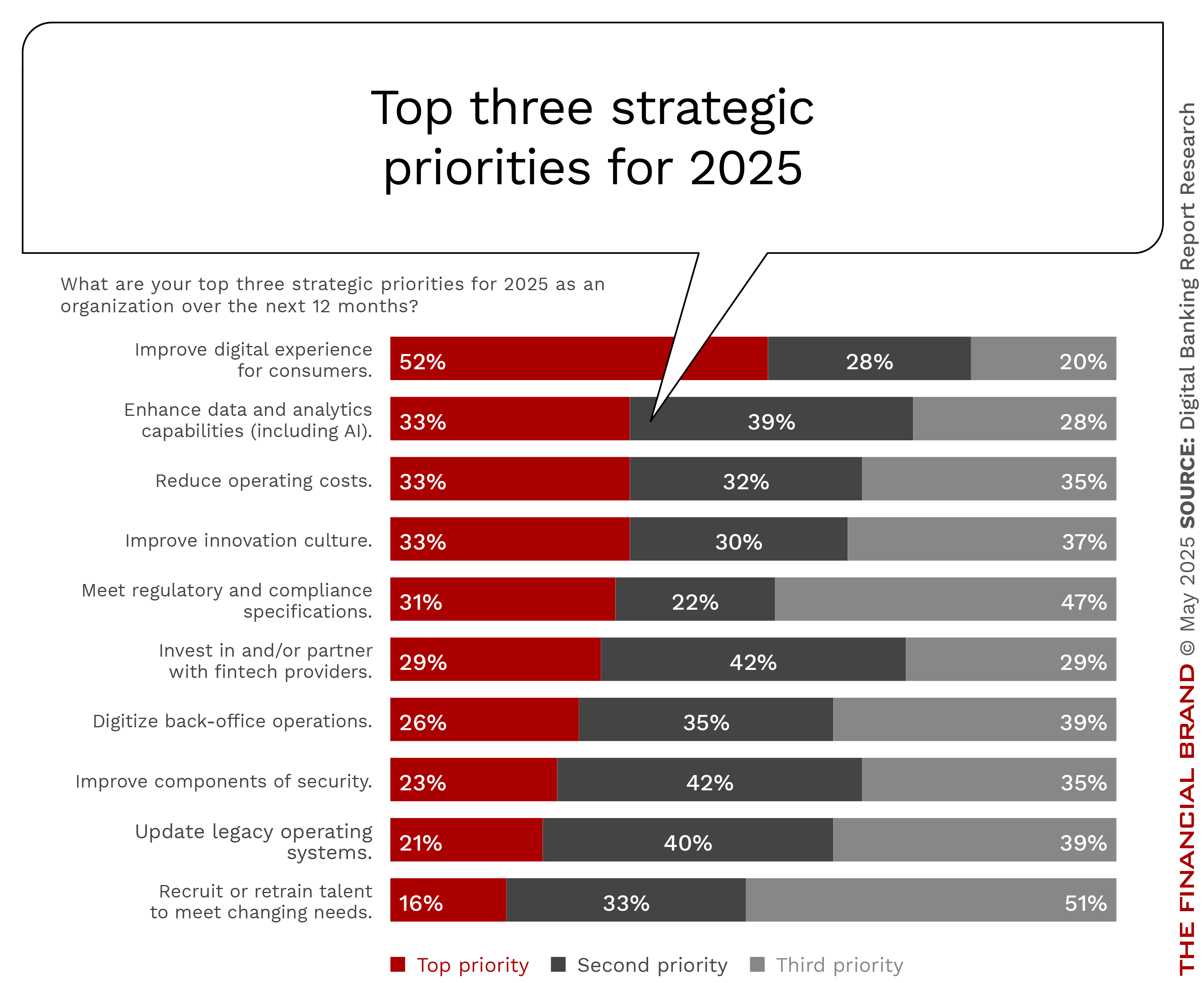

Strategic Disconnects: What Banking Leaders Say vs. What They Do

A persistent and intriguing gap exists between what banking executives identify as industry trends and where they actually allocate resources. While improving digital customer experiences commands the highest strategic priority at 52%, executives rank the broader digital transformation trend significantly lower at 40%.

Similarly, despite acknowledging data analytics as 2025’s most important trend, only 33% of institutions prioritize enhancing these capabilities in their strategic plans. This misalignment between recognized industry direction and resource allocation creates potential vulnerabilities as more agile competitors align their strategies more coherently.

The fintech partnership landscape reveals another curious disconnect—ranking low as an anticipated trend (15%) but receiving notably higher strategic investment priority (29%). These contradictions suggest either strategic hedging or a fundamental difficulty in translating industry awareness into actionable priorities.

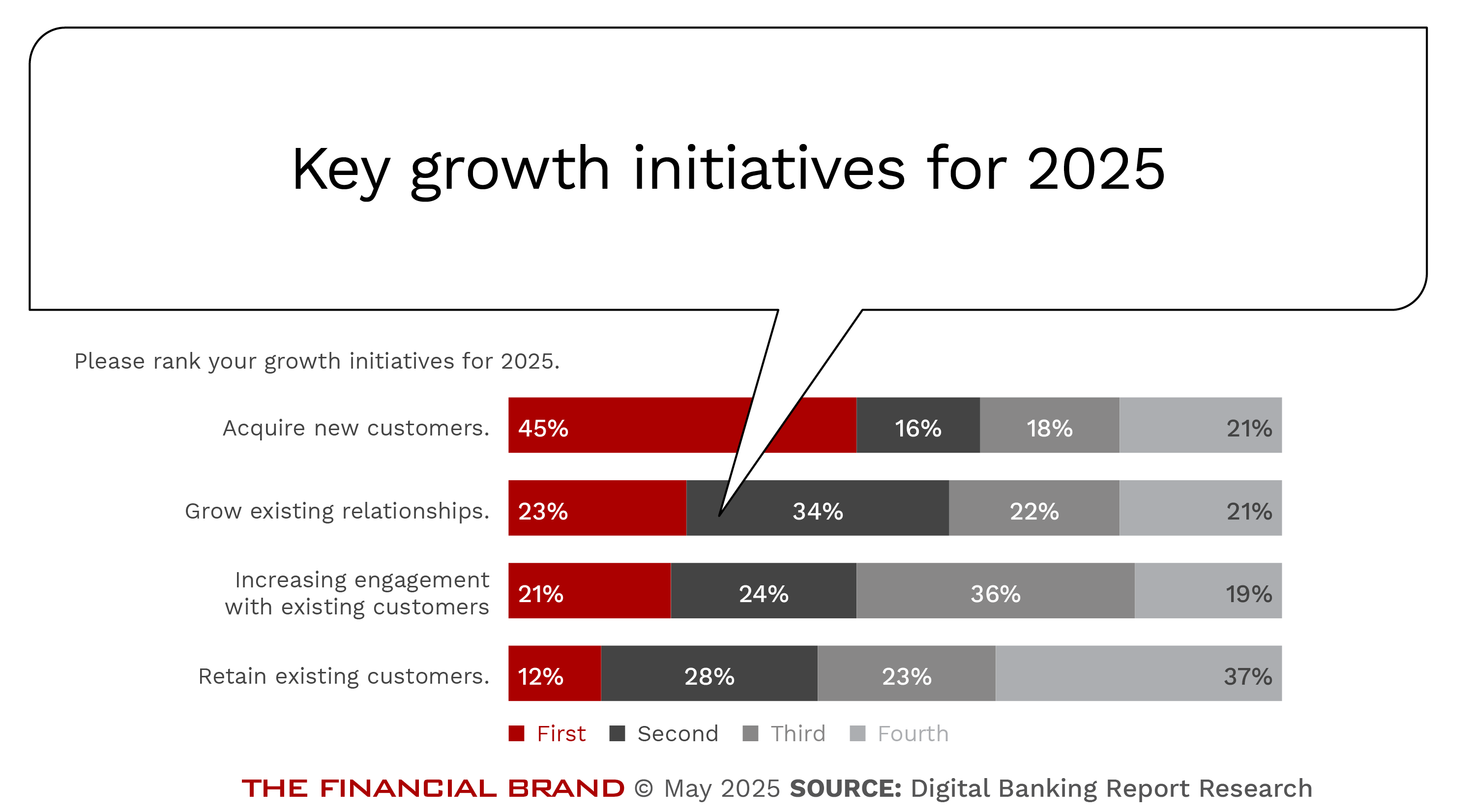

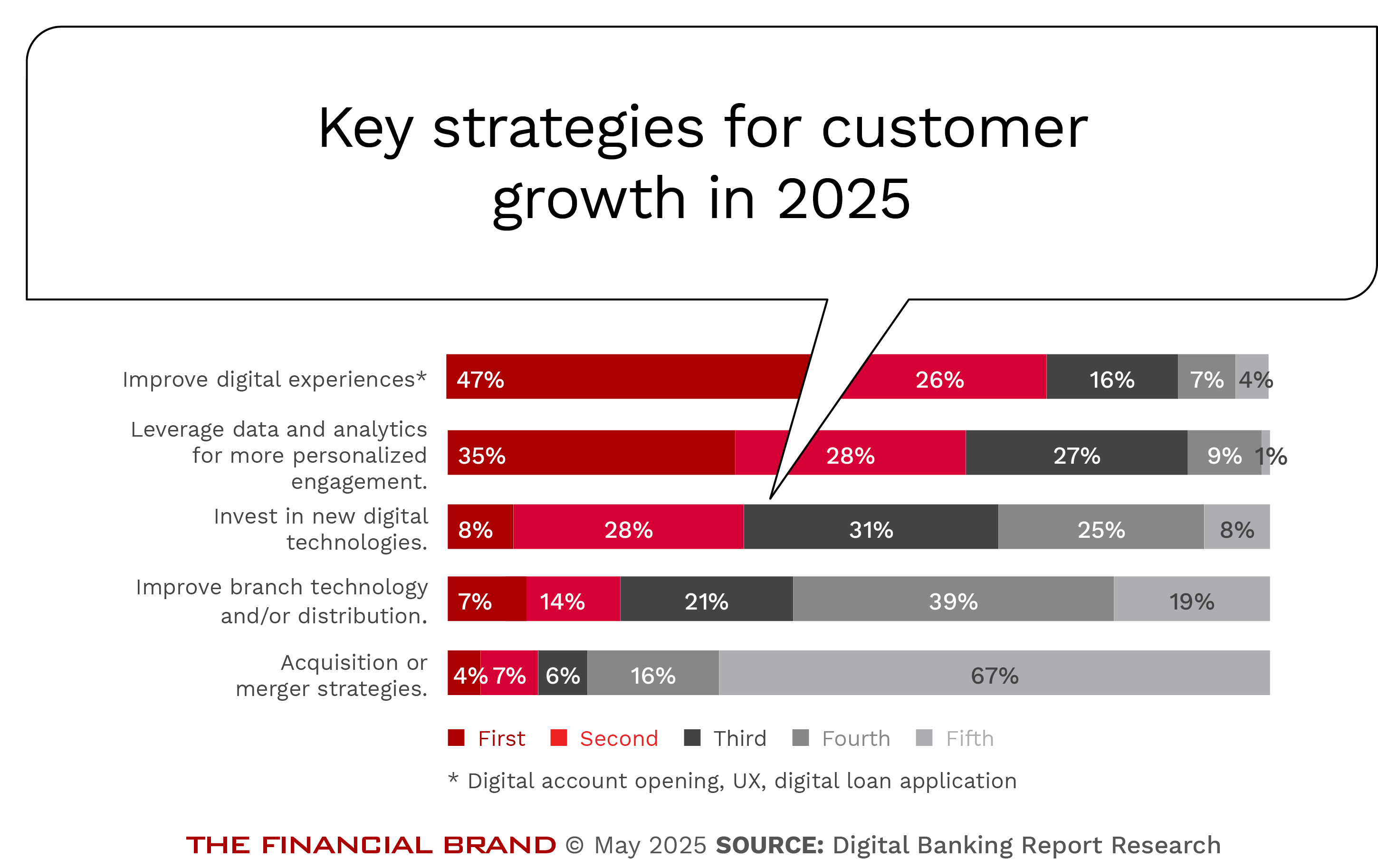

Growth Playbooks: Offense and Defense in a Changing Game

In 2025’s competitive landscape, banking leaders are simultaneously advancing offensive growth strategies while fortifying against disintermediation threats. With nearly a third of executives anticipating significant market disruption from non-traditional players, institutions are refining their approach to customer acquisition and relationship development.

New customer acquisition remains the dominant growth strategy, increasing from 43% to 45% year-over-year. However, a subtle but significant shift is occurring in relationship development, which maintains its 23% primary priority ranking but shows a marked increase as a secondary focus (from 29% to 34%).

Customer engagement strategies are gaining prominence, rising from 17% to 21% as a top priority. Interestingly, explicit retention efforts have declined from 18% to 12%, suggesting that institutions increasingly view retention not as a standalone initiative, but as the natural outcome of superior engagement and deeper relationships.

The digital experience enhancement mandate remains relatively consistent year over year, at approximately 47%. The most dramatic strategic pivot appears in data analytics for personalization, surging from 27% to 35% as a top priority—an 8-point jump that signals growing recognition of data’s role in driving meaningful customer relationships.

Perhaps counterintuitively, investment in new digital technologies has declined as a top priority from 13% to 8%, though combined first and second-tier priorities remain stable. This may indicate a more mature approach to technology investments, with institutions becoming more selective and strategic, rather than pursuing technology for its own sake.

Download Report: 2025 Retail Banking Trends and Priorities

Deposit Strategy Evolution: From Rate Wars to Relationship Focus

The battle for deposits continues in 2025, but the weapons of choice are evolving away from interest rate competition toward data-driven targeting. Analytics applications for existing customers have increased from 52% to 57%, while prospect targeting has slightly decreased — suggesting a strategic pivot toward deepening established relationships.

The creation of short-term deposit products has declined significantly as a priority, from 53% to 43%, and so has the willingness to pay premium rates across portfolios, from 34% to 20%. This retreat from rate-based competition signals a more sophisticated approach to deposit gathering that emphasizes relationship value over transactional incentives.

Real-Time Payments: The New Table Stakes

The payments landscape is undergoing a rapid transformation, with institutions accelerating the adoption of real-time payments. Organizations without real-time payment capabilities have decreased substantially, from 51% to 38% in just one year — a 13-point improvement that reflects the growing recognition of immediate payment capabilities as competitive necessities.

Financial institutions offering comprehensive real-time payment options have increased from 35% to 46% year-over-year. By 2025, 62% of institutions are projected to offer some form of real-time payment capability, compared to 49% in 2024 — a remarkable acceleration driven by customer expectations and competitive pressures.

However, a capability gap persists between institution types, with 62% of banks offering real-time payments compared to just 40% of credit unions. This disparity highlights the ongoing challenges smaller institutions face in deploying advanced technologies while maintaining service parity.

Download Report: 2025 Retail Banking Trends and Priorities

Small Business Banking: Mining the Opportunity Gap

Financial institutions are increasingly recognizing small businesses as an underserved segment requiring specialized attention. The priority given to small business mobile banking platforms has increased from 43% to 45% year-over-year, while expanded service offerings like payroll and cash management have risen from 39% to 41% as primary focuses.

The most significant shift appears in financial visibility tools, with efforts to help businesses gain accurate financial pictures jumping from 23% to 33% as a top priority. This 10-point increase reflects growing recognition of small businesses’ need for actionable financial insights beyond basic transaction services.

Branch Strategy Reimagined: From Liability to Strategic Asset

Despite digital advancement, physical branches remain central to acquisition strategies for many institutions. Organizations planning branch network expansion have increased from 29% to 35% year-over-year, while those intending to “rethink” existing branches have slightly decreased from 28% to 27%.

Perhaps most surprising is the sharp decline in branch reduction plans, falling from 13% to just 8% between 2024 and 2025. This 5-point reduction, combined with expansion plans, suggests a potential reversal of the consolidation trend that has characterized banking for years.

These shifts indicate an evolving perspective on physical locations — from cost centers to strategic assets that complement digital capabilities. Rather than viewing branches as legacy liabilities, forward-thinking institutions are reimagining them as differentiation points in an increasingly digital-first competitive landscape.

Charting the Course: Integration as Competitive Advantage

As financial institutions navigate the complex currents of 2025, success increasingly depends on strategic integration rather than making binary choices. The most successful organizations are those that craft coherent strategies that leverage technology while preserving fundamental relationships.

The future belongs not to institutions that choose between digital and physical, but to those that create seamless experiences spanning both domains. By combining technological sophistication with human connection, financial institutions can forge customer relationships that transcend transactional interactions and resist disintermediation threats.

Organizations that embrace this integrated approach — investing strategically in technology, personalization, and targeted physical presence — will discover competitive advantages that purely digital or traditional models cannot replicate. In this environment, the winners won’t be those with the most advanced technology or the most extensive branch networks, but those who most effectively blend these elements into compelling customer value propositions.

Download Report: 2025 Retail Banking Trends and Priorities