Banks and Credit Unions Rethinking Priorities Amid Economic Uncertainty

New digital banking platforms, the rise of embedded finance, the advent of composable solutions and the expansion of third-party collaborations are creating new horizons for growth, while the current economy is posing significant challenges for customer acquisition, asset liability management, brand differentiation and profitability.

By Jim Marous, Co-Publisher of The Financial Brand, CEO of the Digital Banking Report, and host of the Banking Transformed podcast

Simple Subscribe

Subscribe Now!

As we progress through 2023, the financial services industry finds itself on the cusp of a new era of digital banking transformation. It is being powered by rapid technological innovation, evolving customer expectations, a shifting economic landscape and the emergence of new business models.

The digitalization of finance has created opportunities for banks and credit unions to scale their operations and reach a wider customer base almost instantly. The emergence of new artificial intelligence tools has accelerated these trends.

The path ahead is not without challenges, however. Increasing interest rates and recent financial institution failures continue to pressure both the ability to generate loans and retain customer deposits.

With growth and revenues both at risk, organizations must prioritize the following needs: to improve back-office efficiency, to enhance the personalization of customer experiences, and to focus on the increasing threat of cyber-attacks and data breaches.

To better identify the top strategic priorities for bank and credit union CEOs for 2023 and 2024, Jack Henry conducted its fifth annual survey of clients across the U.S. with assets ranging from $500 million to more than $10 billion.

Seven key findings emerged:

- Top priorities at all financial institutions are growing deposits and improving operational efficiency.

- The major concerns for banks and credit unions are the economy, talent acquisition, deposit growth and interest rate margin compression.

- The biggest competitive threats are considered to be fintech firms, other traditional financial institutions and challenger banks.

- Technology spending is projected to increase over the next two years.

- Financial institutions will embed fintech solutions, while also embedding banking solutions into third-party platforms.

- New payment innovations will be the focus of almost all financial institutions over the next two years.

- Cybersecurity and fraud mitigation will be a top tech spending priority for banks and credit unions in 2023 and beyond.

Economic Uncertainty Upends ‘Business as Usual’

Amid economic uncertainties, financial institutions have needed to prioritize both financial resilience and operational resilience. With rapidly increasing interest rates and the recent closures of Silicon Valley Bank and other organizations, banks and credit unions needed to evaluate their deposit and loan portfolios, recalibrate risk appetites and rethink legacy business models.

At the same time, financial institutions of all sizes needed to improve operational resilience by rethinking back-office operations and investing in modern technology infrastructures that would ensure efficient delivery of services under a wide range of scenarios. Top priorities now include creating seamless digital experiences, personalizing customer interactions by investing in technologies like AI and machine learning, automating processes, and building new decision-making structures.

Even as it has challenged institutions, economic uncertainty has also acted as a catalyst for change. It has been pushing financial institutions to prioritize resilience, digitization, security, compliance and talent management. While creating challenges, this period is also one of unequaled opportunity for those financial institutions that can embrace change, take risks and disrupt the status quo.

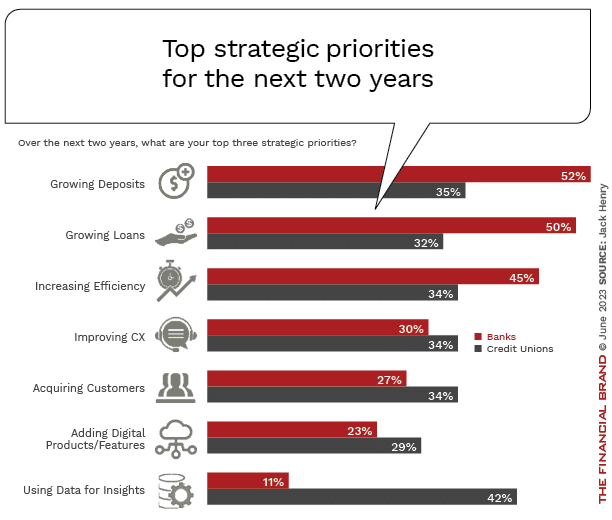

Top Priorities for Banking in 2023 and 2024

Jack Henry’s benchmarke study found that growing deposits, growing loans and increasing operational efficiency are the top overall strategic priorities over the next two years. Major variances in the degree of prioritization between banks and credit unions exist, with the largest variance being the focus on using data to improve insights by credit unions (42% vs 11% for banks).

It is important to note that growing deposits is considered the most difficult priority to achieve, with many organizations not having had a need to work to generate deposits for almost two decades. In addition, CEOs reported accountholder acquisition as the second most difficult priority to achieve, with smaller institutions thought to face the greatest uphill climb.

Top Concerns for Financial Institutions

Banks and credit unions differ on several top concerns, with 53% of credit unions reporting the economic slowdown as their top concern, while 57% of banks report talent acquisition/retention and net interest margin compression as their top concerns. For both banks and credit unions, deposit acquisition and displacement was the second most mentioned concern, with regulatory uncertainties ranking third.

“In 2022 and 2023, the top concern for financial institutions were talent acquisition and retention, that is, having the people necessary to drive digital transformation in all its forms.”

— Jack Henry research

By contrast, in 2021, CEOs’ main concerns focused on fraud and security and failure to innovate.

Read More:

- Digital Banking Transformation Trends for 2023

- Top 5 Customer Experience Trends for 2023 and Beyond

- Top Retail Banking Innovation Trends for 2023

- 5 Payment Trends to Watch in 2023

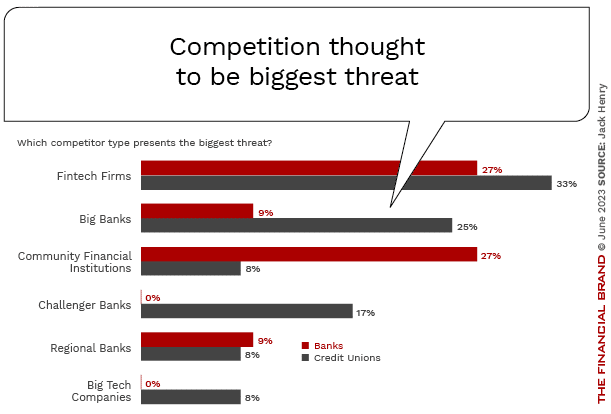

Fintech Firms Still Perceived as Top Competitive Threat

The competitive landscape for retail financial services remains dynamic despite changes that have dramatically impacted many sectors. The Jack Henry research found that fintech firms and digital banks still represent a profound challenge, despite radical drops in venture capital funding and increased focus on ongoing financial viability.

With their agile operating models and tech-forward approach, these disruptors have positioned themselves as attractive alternatives to traditional banks for a vast sector of consumers and small businesses. They leverage technology to provide a seamless and personalized customer experience, offer competitive rates, and create innovative financial products and services that have caused “silent attrition” at the majority of traditional banks and credit unions.

“This was the first year in which big tech companies were not considered a top competitive threat.”

— Jack Henry research

Despite still being considered the top threat, the fear of fintechs has diminished significantly since 2021, according to the research. In more and more instances, fintech firms are being considered potential partners for innovation. Interestingly, banks consider “other community financial institutions” as the second biggest threat, while credit unions considered “big banks” as their second biggest threat.

Vast Majority of Banking Players Will Increase Tech Spending

The Jack Henry research found that 79% of financial institutions plan to increase their tech spending over the next two years. “Of those planning to increase their technology spend, the biggest segment (35%) plans to increase investment between 6% and 10%,” the study reports. Jack Henry also found that larger institutions plan to increase investments by greater percentages than those in smaller asset tiers.

When asked about the areas of technology that are of greatest priority, credit unions were more focused on data analytics while banks reported higher interest in digital banking and fraud and security. Another key finding was that credit unions were much more focused on AI (37%) compared to banks, which reported higher interest in core system upgrades (22%).

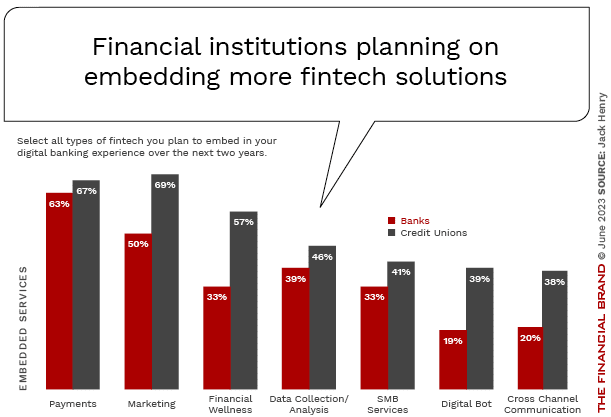

Composable and Embedded Solutions Rise in Importance

In response to marketplace challenges, such as the need for innovation and growth, banks and credit unions are increasingly leveraging composable fintech solutions and third-party embedded banking partnerships with profound implications on operational agility, customer experiences, competitive positioning and growth opportunities.

Composable solutions, where fintech or third party technology is leveraged, enable financial institutions to rapidly develop and adapt their offerings, innovating at speed, tailoring services to customer needs and scaling operations rapidly in response to market demands. By building smaller solutions, banks and credit unions improve the most important areas of digital transformation need without impacting the entire core system.

Almost all financial institutions (90%) plan to embed fintechs into their digital banking experiences over the next two years, with two-thirds planning to embed fintech payment solutions. In general, credit unions are much more focused on solutions that enhance their member experiences with digital marketing (69%), consumer financial health (57%), digital banking bots (39%) and cross-channel communication (38%).

With embedded banking solutions, financial institutions can reach new customers in their existing digital environments, enhancing accessibility and convenience, and opening up new revenue streams. When asked about embedding financial solutions into non-financial, third-party offerings, CEOs were about 50/50 for the concept in the next two years. This was a higher percentage than in previous reports.

Not surprisingly, payments solutions were the most mentioned type of service organizations were planning to embed.

Read More: The Future of Banking Requires ‘Composable’ Solutions

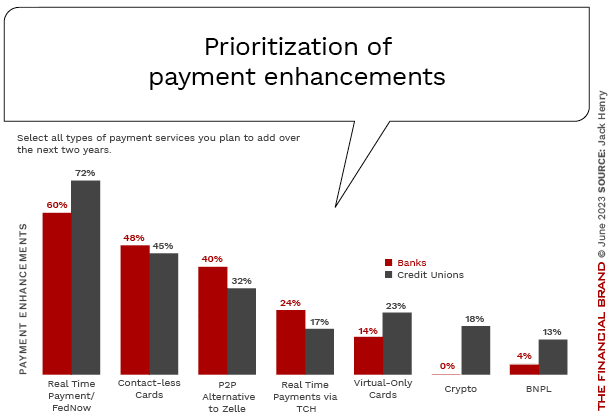

Banks Focused on Simplifying Payments Process

Despite an economic slowdown and increased credit risk, financial institutions are focusing on building robust, secure, and user-friendly digital payment platforms that offer seamless experiences to customers.Enabled by advanced technologies and driven by customer demand for immediacy, real-time payment solutions are a top priority for most financial institutions.

“As momentum builds for simpler, faster, cheaper ways to pay, the challenge for banks and credit unions will be developing a payments strategy for the near- and long-term that keeps pace with innovation and evolving user expectations, especially around digital wallets.”

— Jack Henry research

Nine out of ten of all financial institutions plan to add new payments services over the next two years, with FedNow service topping the list followed by contactless cards and a P2P alternative to Zelle. In fact, faster payments factor into the top four payment services banks and credit unions plan to add during this period.

Real-Time Payments Require Real-Time Fraud and Risk Mitigation

While real-time payments provide greater convenience and efficiency, they also give banks a very small window to detect and prevent fraudulent transactions. This necessitates more advanced, real-time fraud monitoring solutions.

The rise of advanced data and analytic capabilities presents both opportunities and challenges for risk mitigation. On one hand, the vast amounts of data generated through digital banking channels can be analyzed to identify unusual patterns and detect fraud early. On the other hand, the storage and processing of this data can create privacy and security risks. Financial institutions must therefore strike a balance between leveraging data for fraud prevention and ensuring robust data protection.

Phishing attacks (70%) and real-time payments fraud (54%) are the most concerning fraud and security threats, states the Jack Henry report. Data breaches (49%) come in a close third as far as concerns of bank and credit union CEOs.

Preparing Banking for the Near-Term Future

Preparing for the next two years, financial organizations must leverage technological advancements, operational improvements and third-party collaborations to provide the flexibility and composable solutions that can meet market demands at speed and scale. With growing economic uncertainty, banks and credit unions must improve financial and operational resilience with real-time insights into market shifts.

Embracing AI and machine learning for decision-making and can enhance the ability to predict consumer preferences while also mitigating risks. Lastly, banks must be proactive in regulatory compliance, particularly with increased scrutiny on data security and privacy, which will help maintain customer trust and avoid reputational damage.