AI-First Nubank is Seeking a U.S. Charter, and Domestic Players Should be Worried

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Need to Know:

- Brazilian fintech-turned-bank Nubank is a huge, profitable, digital-only player — and now it’s eyeing the U.S.

- Nubank puts most U.S. banks to shame in its deployment of AI, in both customer service and product development.

- Its immediate challenge: In its existing markets, Nubank banks on primacy, but in the U.S. consumers typically spread their financial affairs among many players.

Digital-only pioneer Nubank is a success story, powered by a combination of fintech innovation and regulated banking. It’s a true “neobank.”

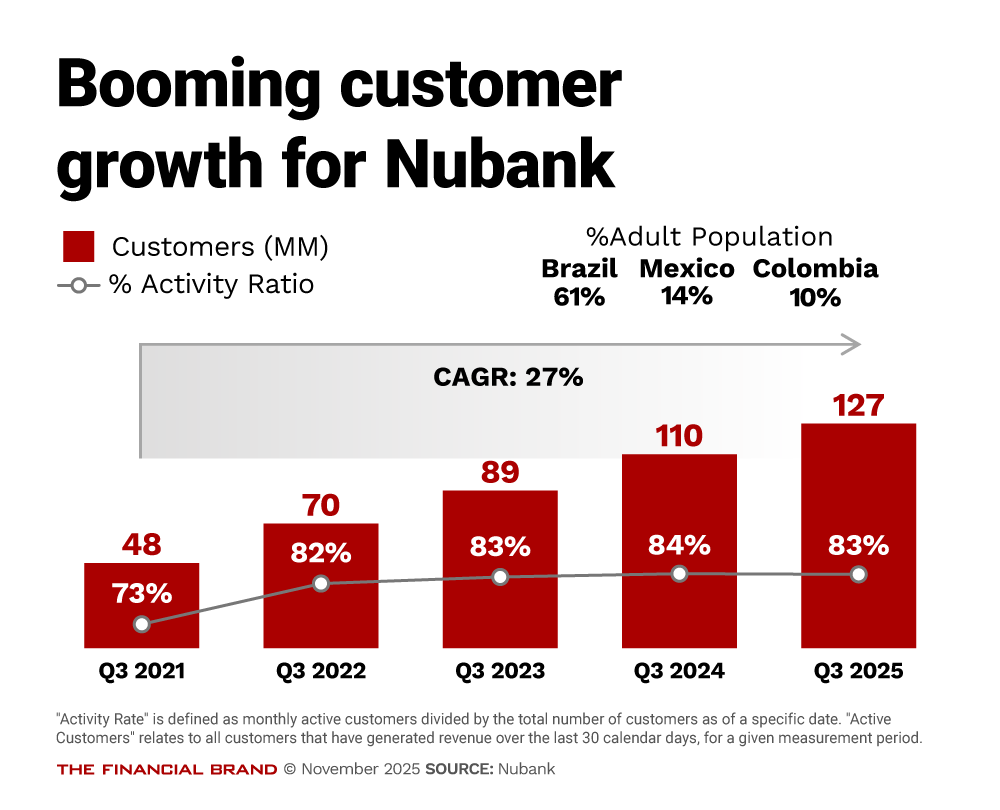

Since its founding in 2013, it has become the third-largest financial institution in Brazil, serving 127 million customers. including millions of expatriates in other countries.

In September, Nubank filed for a U.S. national bank charter. Give the bank’s history of digital innovation and its avowed goal of being an “AI-first” company, it could enter the U.S. fray with more experience with AI than many domestic players

According to the public portions of its application with the Comptroller of the Currency, in the first three years of its anticipated rollout, Nubank, N.A., would focus on checking accounts, credit cards, unsecured personal loans, and digital asset custody and related services.

In its home country, Nubank serves a startling 60% of the adult population. It is now rapidly expanding into financial products for teens and tweens, the customers of the future — including a credit card program designed specifically for Brazil’s older teenagers, aimed at teaching responsible use of credit. (For comparison, JPMorgan Chase reaches 68% of the U.S. population in some product relationship.)

The company still sees a great deal of room available for growth in Brazil, but it has also been expanding to other parts of South America. In Mexico, which it entered in 2019, Nubank has already been granted a banking license management expects to put in motion in 2026. Today it serves 13 million customers, about 14% of the country’s adults — and 25% of its banked population. In Colombia, which it entered in late 2020, it is approaching 4 million customers. (In Brazil, Nubank operates as a “credit, financing, and investment entity.” There, Nubank operates under extensive Brazilian regulation through multiple specialized licenses, notably a payment institution and a credit/financing institution.)

The typical strategy for Nubank is to begin simply and narrowly, with digital-only products that stress convenience and low-cost/no-cost service. It then expands the range of products offered as the institution establishes itself.

The company — officially Nu Holdings Ltd. — reported a compound annual growth rate of 70% in gross profits from the third quarter of 2021 to the third quarter of this year.

Nigel Morris, co-founder and managing partner at QED Investors, says he admires the company’s ability to innovate and grow in a regulated form. A bit over a decade ago, it didn’t exist, and now it is a major factor in one of the world’s largest economies.

“We were lucky enough to invest in it very, very early,” says Morris, a co-founder of Capital One Bank, “and we remain close to the founding team there.” He admires the company’s ability to find ways to operate in each country it expands into, with a stated goal of moving from a strong regional player to a global challenger.

What It Means to Be an AI-First Organization

During its latest earnings briefing, Nubank’s David Vélez, co-founder, chairman and CEO, spoke in broad terms about the company’s embrace of artificial intelligence. Typically, implementation starts in Brazil and spreads to other markets the company covers. He divided the AI technology into two categories: customer-related and business operations.

On the customer side, key elements include improvements to app experiences, personalized recommendations, and open finance intelligence. On the business side, AI assists with collections, fraud prevention and greater productivity in the company’s AI engineering.

Vélez says there’s overlap between the two sides, which includes facilitating better credit offers, improving cross-selling efforts — including better “in the moment” offers — and results, and finding “win-win” price points.

“We think there is a significant opportunity to include agentic workflows across most products and services, improving customer experiences across the board,” says Vélez. He also notes that over the last year Nubank devised nuFormer, a proprietary AI model for such tasks as analyzing customer behavior. One result allowed Nubank to adjust credit card limit policies in Brazil, empowering the bank to expand credit for qualifying customers without sacrificing its overall risk attitude.

Maristela Calazans, general manager of global bank account products at Nubank, explains that customer-facing AI efforts focus on making the company’s app work more quickly and more effectively.

“AI can help guide the customer through some challenging journeys and transactions that are still very complicated for them to understand,” says Calazans. She says this is especially helpful with customers new to products that have been available solely to more upscale customers in the past.

Calazans explains that AI also helps with product development. Some of this involves tools that help Nubank handle coding more expeditiously. But AI also helps to understand customers’ needs and guide product development, by sorting through the company’s market and client research in depth. Using AI, features that might have taken three or four months to build in the past now can be delivered in a week or less, she explains.

Getting employees to use the models hasn’t been difficult, but to “start developing those muscles” Nubank has measures like AI-focused hackathons.

Read more:

How a Fintech Bank Applies AI Tools in a Regulated Bank Environment

Calazans says strict rules are in place to make sure outside tools aren’t being used on customer data.

“We can only use those tools allowed and licensed through the bank, so we can guarantee privacy,” says Calazans, adding that emphasis is put on training, “because we are in a very regulated environment.”

Expansion of AI adoption is steered by an internal committee that examines new use cases. This group also looks at new tools that become available. A green light at that level leads to reviews in other parts of the company, by functions such as compliance.

Calazans explains that a key detail in product development is staying within the tolerances of each country’s customer base. In Brazil, for example, consumers tend to be leery of too much automation — “They want to have control,” she says.

“We look at how we can better help them without their losing the sense of being in control and being able to make the last click or the last decision,” says Calazans.

A real-life example: Brazil is home to the pioneering Pix instant payments service, which Brazilians use for many payments, including a lot of smaller ones as they go about their daily lives. However, Calazans says they don’t like opening their banking app while they are out on the street — it doesn’t feel safe.

So, using AI techniques, Nubank developed an interface with the social app WhatsApp so that requests for payment or sharing expenses sent through that app can be forwarded and paid instantly via the consumer’s Nubank account. She says the service is still favored by early adopters, but that interest picks up as more people try it.

Read more: More Banking Apps Offer Predictive Insights, But Many Alerts Arrive Too Late

Parsing Consumers’ Desires as Nubank Expands into the U.S. and Beyond

Calazans says that, in most places, “the jobs to be done are basically the same,” says Calazans. “You need to receive money, you need to pay your bills, you need to transfer money to someone, you need to save, you need to invest.”

But while consumers share many needs, Calazans says customer attitudes can differ among markets in other significant ways. For example, as the bank looks forward to the approval of its U.S. charter, she and her team are pondering the fact that U.S. consumers tend to have very fragmented banking relationships.

She explains that she has been surprised by how many different financial apps the typical U.S. consumer maintains.

“There’s no centralization of Americans’ financial lives,” says Calazans. “They may have their bank account in a traditional bank. They may use a fintech for splitting payments or doing transfers.”

In Brazil, consumers tend to put everything in one place, says Calazans. In the U.S. this is usually described as “primacy,” and for some can be an elusive goal; in Brazil the term is “principality.”

That factor is “super critical” to Nubank in Brazil, according to Calazans. “We look at this as one of our main indicators of how we’re doing.”

Figuring out how to serve a population that may have 10 to 15 financial apps on their phones is new, says Calazans. But Calazans thinks the answer will lie in tracing transactions for which Americans use multiple apps and finding ways to unify them in Nubank’s future offerings: Why is someone making a deposit? It probably means a payment is in the offing, she says.

“We have to figure out how to connect those things for them, to make this much easier by getting them to do everything in the same flow, in the same app,” says Calazans. “We’re trying to understand the mental model of the American consumer.”

Read more: The Classic Checking Account Doesn’t Meet the Needs of Today’s Consumers. Here’s How to Fix It